Sentiment continued to deteriorate on Wednesday on the back of a stronger US CPI print, which caused the dollar to climb higher and led to another slump on Wall Street. Thing didn’t improve at all during the Asian and early European hours, where indices fell further. The FTSE and pound were weighed down further by industrial production and business investment contributed to further a fall in monthly GDP already hurt by a surprise in drop in retail sales we saw a couple of weeks ago. Bitcoin slumped to $26K as the crypto carnage continued for yet another day. Even the Japanese yen found some haven flows, after it had fallen to repeated multi-decade lows in recent trade.

We all know what is the root cause of all this, but don’t forget that sentiment plays a big part. Right now, confidence is shaken among market participants and people are in no mood to take on risk. So, even when we see periods of relative calm, it doesn’t last very long.

UK likely heading for a recession

As far as the UK market is concerned, a lot of the weakness we are seeing is because of the global macro situation, with inflation and rate hikes weighing heavily on sentiment. Domestically, things don’t look very good either.

Following news of a 0.1% negative growth in March and other data suggesting the economy has stagnated, there is a very good chance output will drop in the second quarter. It is worth to point out there is an extra bank holiday scheduled for this June, which should further disrupt economic output already impacted by ongoing consumer spending squeeze as a result of soaring energy costs and inflation.

With growth outlook being far from encouraging, the Bank of England may well end its hiking cycle earlier than expected, which is precisely what the pound traders must be thinking given the sharp falls of later. So far, the BoE has hiked rates 4 times and the market was previously pricing in another 5. But the way things are going, I would be surprised if we get more than 3 hikes of 25 basis each, before hiking is paused.

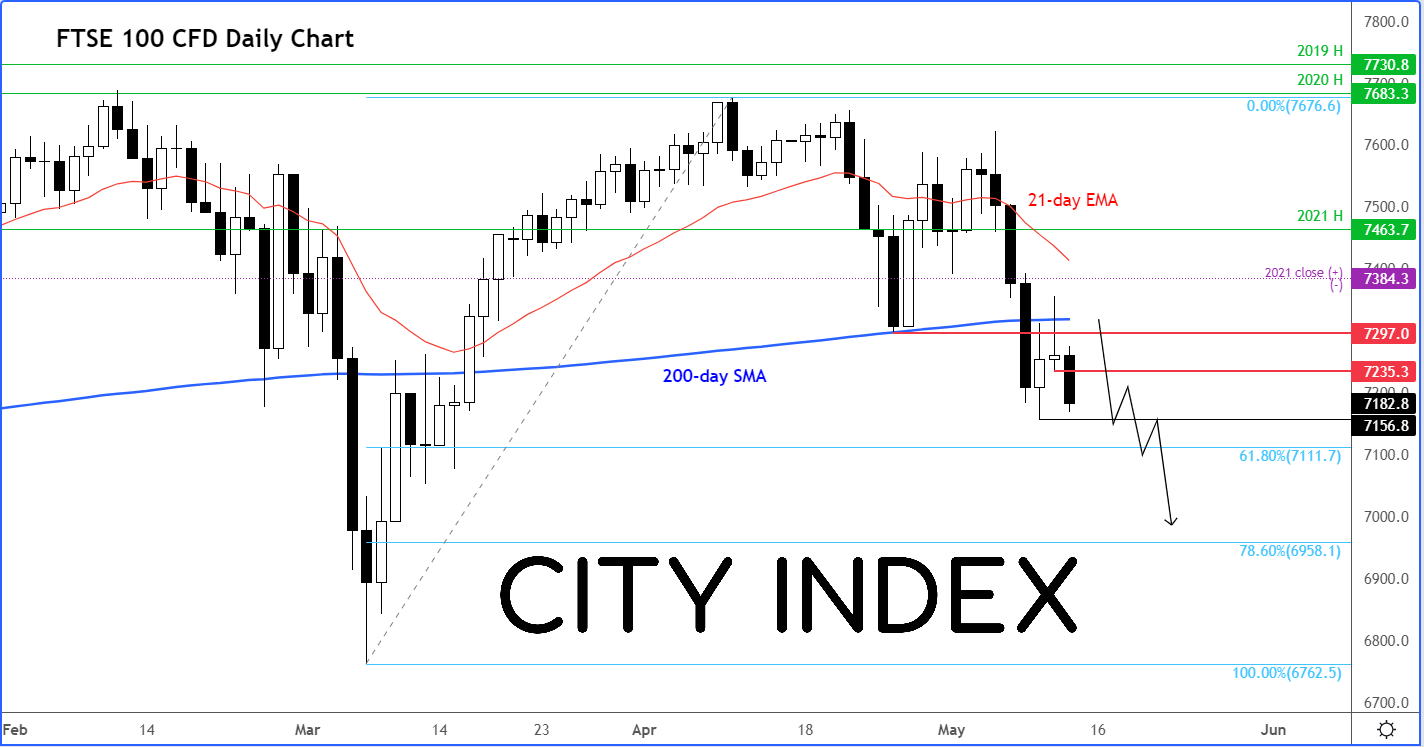

FTSE breaking down

It is worth watching the FTSE closely here, because so far, the UK stocks have held their own relatively well, meaning there’s scope for downside risks given the losses globally. At the time of writing, the FTSE was just over 2.7% lower year-to-date, which contrasts sharply with the falls witnessed on Wall Street and elsewhere.

However, the FTSE failed to hold its breakout above the 200-day moving average this week, which is far from an encouraging sign. The failure means the bulls will probably not try to attempt to buy short-term dips until at least when the index becomes quite oversold or when sentiment towards global equities turn positive again. Either way, this is unlikely to happen in the near-term outlook, meaning, the FTSE is likely headed lower from here.

How to trade with City Index

You can trade with City Index by following these four easy steps:

- Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the company you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Yesterday 08:33 AM

Latest FTSE articles

April 10, 2024 08:46 AM

March 27, 2024 09:37 AM

March 18, 2024 09:19 AM

March 13, 2024 08:54 AM