The Serco effect

Call it the Serco effect. A heavy burden was lifted from the firm on Friday, yet the shares dropped like a stone. Serco shares traded […]

Call it the Serco effect. A heavy burden was lifted from the firm on Friday, yet the shares dropped like a stone. Serco shares traded […]

Call it the Serco effect.

A heavy burden was lifted from the firm on Friday, yet the shares dropped like a stone.

Serco shares traded as much as 12.5% lower to 145p.

In one of the better pieces of news for the firm this year, the City of London Police abandoned its investigation into a contract between Serco, one of the world’s largest outsourcing firms, and the UK prison service.

Square Mile detectives announced on Friday afternoon they had concluded their probe of the firm’s Prisoner Escort and Custody Services (PECS) contract, and would not be continuing with their investigation.

In August 2013 City Police were asked to investigate if Serco staff had been misleadingly recording prisoners as ready for court when they were not.

Serco noted on Friday the investigation concluded there was no evidence of any corporate-wide conspiracy or intention to falsify figures.

Still, Serco already agreed to forego all past and future profit for the contract which still has three years and eight months to run.

And the government watchdog report into government contracting concluded last week that too often “the ethical standards of contractors had been found wanting”.

The cross-party Commons Public Accounts Committee also noted “Competition for Government business should bring with it a constant pressure to innovate and improve. But for competition to be meaningful, there must be real consequences for contractors who fail to deliver and the realistic prospect that other companies can step in.”

Aside from this signal from Parliament of increased rigour in ensuring competitive contract awards, Serco still of course retains a formidable list of issues.

To be fair, it hasn’t been all doom and gloom for the firm. Serco has signed a £1bn contract to continue running Australia’s onshore immigration detention services, the company said on Wednesday.

And it also emerged the firm continued to undertake separate business with the UK government despite it remaining under investigation by the Serious Fraud Office.

That may not be enough to encourage long-term buyers of its stock though.

The reputational impact of events of the last several months, combined with the severe slimming down pledged by Serco’s relatively new CEO Rupert Soames, all point to signs that the firm has itself concluded it lacks the level of intellectual capital required to operate as the huge and attenuated conglomerate it was in the past.

It has 122,000 staff in 20 countries many of whom are servicing low-margin contracts.

All of the above mean Serco is not ready yet for the long-term investors its share register would require to bring some stability to the stock.

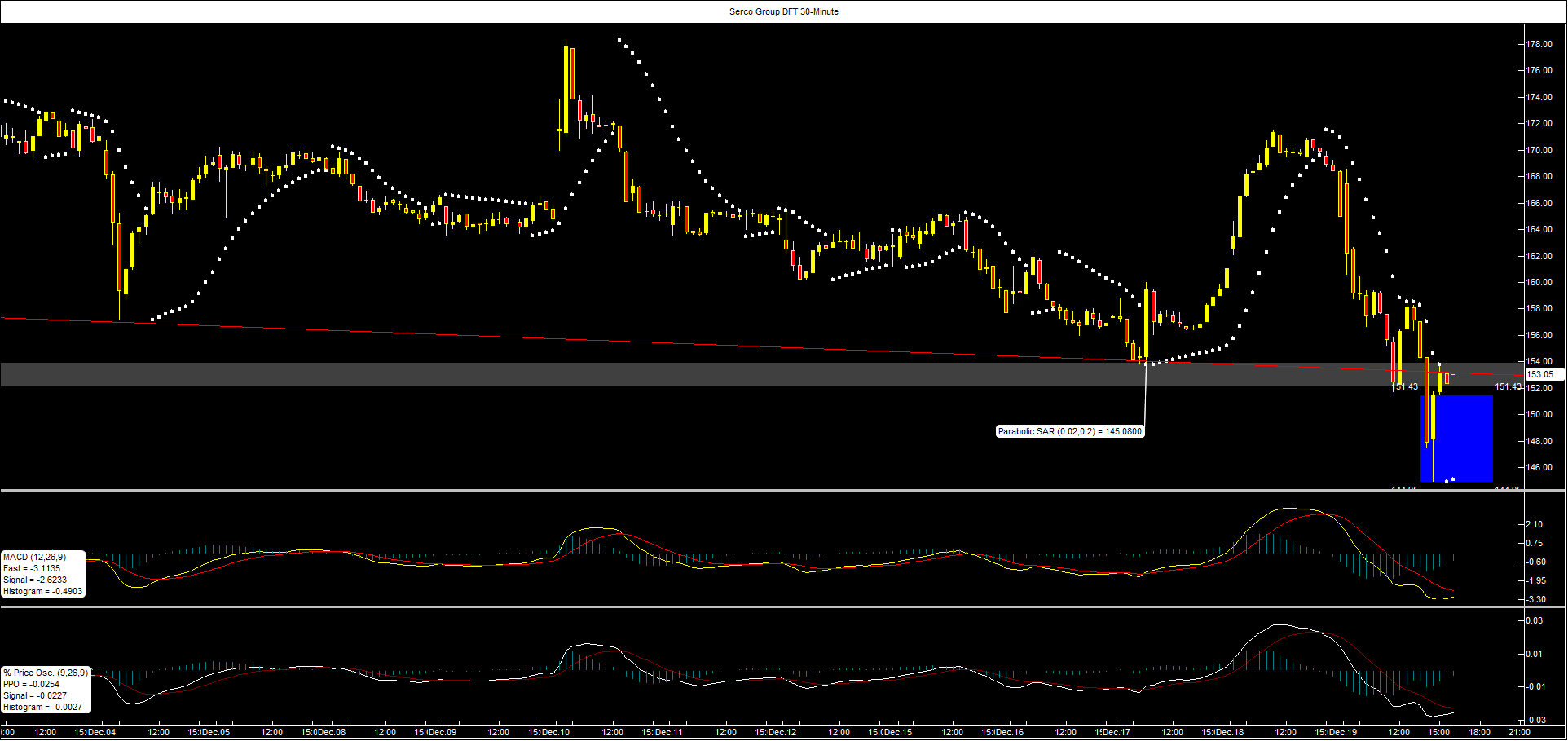

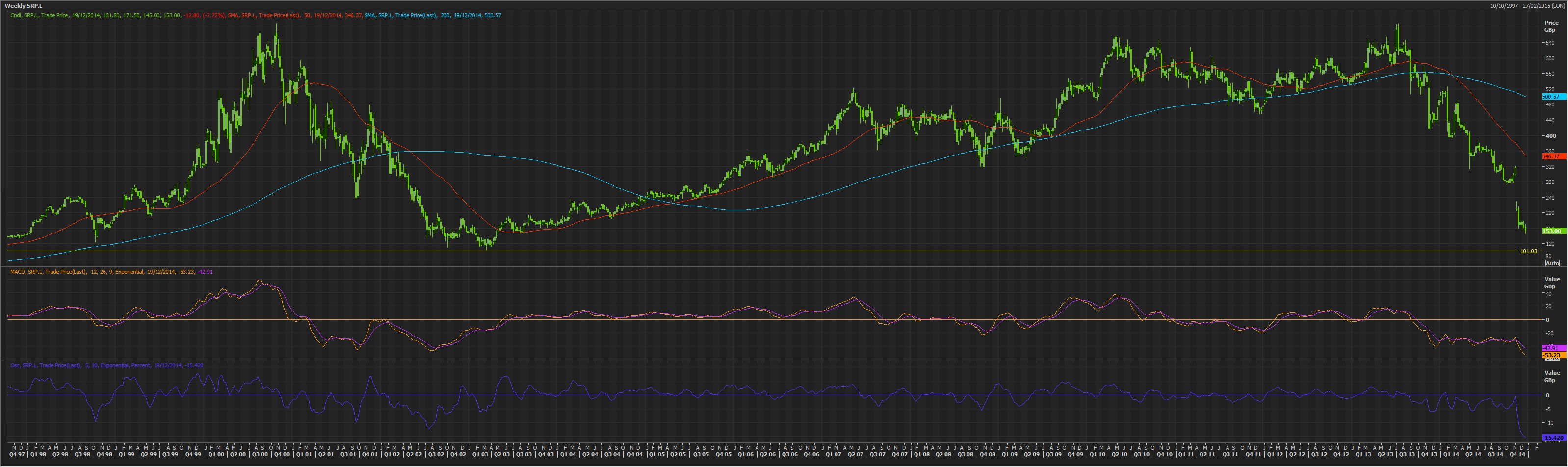

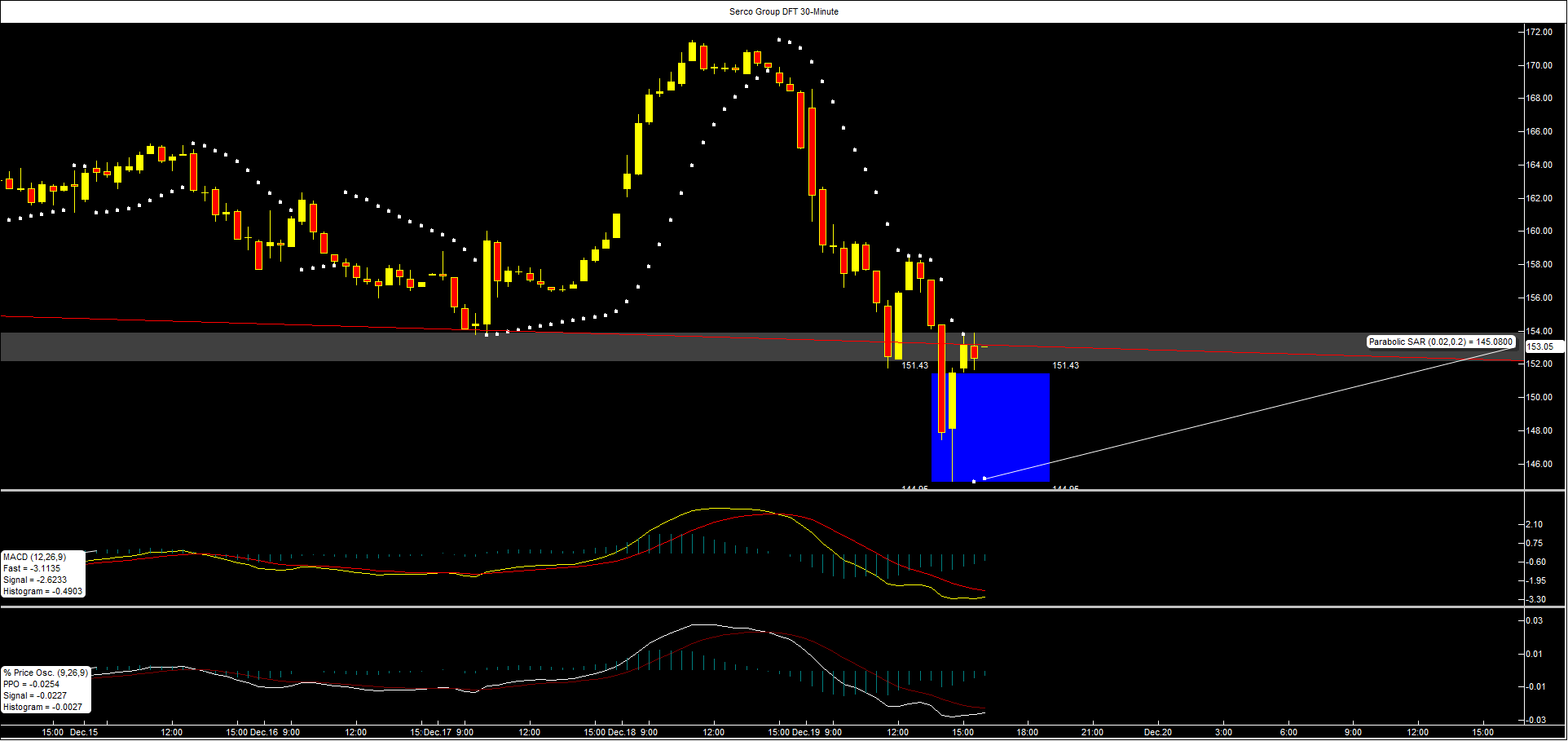

One medium-term glimmer of hope (albeit temporary) for the stock: downside momentum is overstretched on a weekly basis.

Traders of City Index’s Daily Funded Trade already started to lighten up on shorts or add, after the title reached near to lows corresponding to those of the underlying stock.

At the same time, the half-hourly trading in the DFT has not ventured far above a downtrend visible from late November (the trend currently leads to around 151).

The particular leg of the DFT’s fall (also reflected in the underlying stock) from late November coincided with the firm writing off £ 1.5bn, news of its rights issue and the resignation of its chairman.