The pound tells us that May could deliver bad news on Tuesday

When Theresa May lays out her vision for Brexit on Tuesday, she will be giving the speech of her career. Expectations are growing that she […]

When Theresa May lays out her vision for Brexit on Tuesday, she will be giving the speech of her career. Expectations are growing that she […]

When Theresa May lays out her vision for Brexit on Tuesday, she will be giving the speech of her career. Expectations are growing that she will give “Hard Brexit” a new sense of reality.

At this stage her speech could leave more questions rather than answers. For example, if she announces that we will leave the single market and the customs union, as expected, then what will she replace it with? If she says that our most important industries will be protected, then what “special” deals will she set up with Brussels to ensure that our financial sector doesn’t move to Frankfurt, or that foreign business owners don’t shift overseas?

Even publically stating that she sees us leaving the single market could trigger questions regarding her legitimacy to do so, especially ahead of a court ruling that could force the government to hold a Parliamentary vote on the minutia of their Brexit plans.

More woe for GBP

Combined with a market that is positioned towards further downside in the pound – CFTC positioning data is showing another build up of short positions in GBP/USD, and overnight volatility in GBP/USD is at its highest level since August – it is hard to see how Mrs May is going to do anything other than weaken the pound tomorrow.

Politics to remain pound’s kryptonite

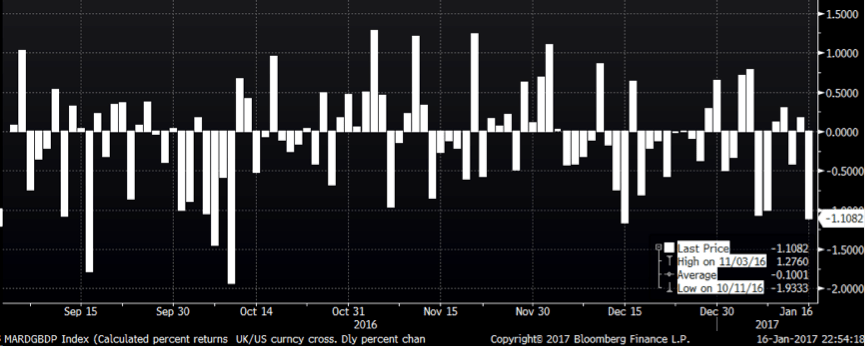

Theresa May’s aides reportedly said that her speech could trigger a “material drop in the pound”. The chart below shows the daily percentage moves of GBPUSD since October. It is a good visual guide to how volatile the pound has become, predominantly on the negative side. Back in October, we were regularly getting daily moves to the downside of 2%, post the Tory Party Conference. Declines have not been as large since, but considering Tuesday’s speech is being touted as the most important since May became Prime Minister, then we could see much larger declines in GBP, and another rise in volatility in the coming days. Thus, politics are likely to remain the pound’s Kryptonite for some time yet.

Figure 1: GBPUSD daily percentage moves

Source: City Index and Bloomberg

So how low are we talking for GBP/USD? If volatility does increase, and downside moves get larger then we could quickly smash through 1.1841, the low from October’s flash crash, and head towards 1.10 before May actually pulls the trigger on Article 50.

Buy the rumour, weakly sell the fact?

There is a risk that the market could sell the rumour and buy the fact, however, figure 1 also shows that rallies in the pound in recent weeks have been weak, while selloffs have been harsh and prolonged. Thus, she would have to give one hell of a speech to turn around sentiment to sterling in this environment, and due to this, we think that we have not yet seen the end of the pound’s downtrend.

Of course, as we mentioned earlier today, May’s speech is not the only thing that could weigh on the pound. Inflation also matters, read more on this here: https://www.cityindex.co.uk/news-and-analysis/one-chart-that-explains-the-pound-s-decline/

Could political fear hit the FTSE 100?

The tonic to the weaker pound has been the rise in the FTSE 100 in recent months; however, even this could be at risk as we approach the triggering of Article 50 in 3 months’ time. Although the FTSE 100 made a fresh record high on Monday, bulls may want to watch out, as there are signs that political risks might be starting to bite. Financials were one of the worst performers in the FTSE 100 on Monday, and RBS fell nearly 3% after Goldman Sachs downgraded the bank due to rising political volatility in the UK. This suggests that banks, which have helped to lead this rally, could at risk from a sell off in the coming weeks.