The fallout from the Fed minutes

So, the minutes were considered dovish, which is no surprise since the meeting at the end of July allowed an element of doubt to be […]

So, the minutes were considered dovish, which is no surprise since the meeting at the end of July allowed an element of doubt to be […]

So, the minutes were considered dovish, which is no surprise since the meeting at the end of July allowed an element of doubt to be thrown in about the prospect of a rate rise next month. The build up to the first rate hike from the US is starting to get tortuous, the market wants clear direction from the Fed, but the Fed is resisting it. Our view is that the decision will come down to the wire, with the market lurching at key employment, wage and inflation data between now and then.

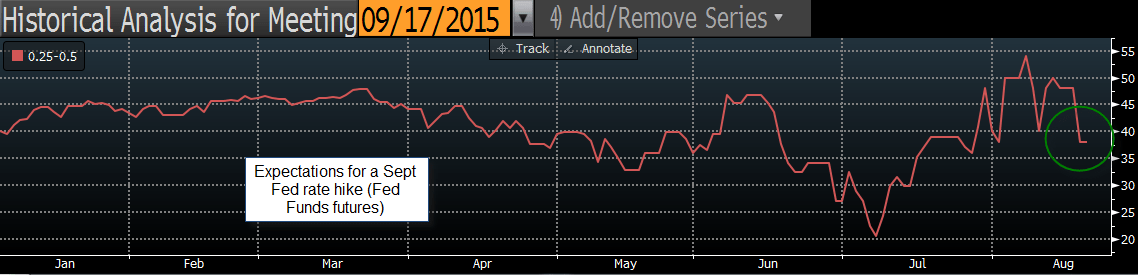

The actual damage done from these minutes is a shift in Fed Funds futures. The Fed Funds futures market is now pricing in a mere 38% chance of a rate hike next month, compared with more than 80% of economists polled by Bloomberg looking for a rate hike. The market is a bit more optimistic of a rate hike in December, with a 66% chance of a move. However, recent events including a sell-off in stock markets and the Chinese currency devaluation has made the market less sure of a rate rise in 2015, and more likely to put their money on a rate rise in Q1, where there is an 83% chance of a rise according to Fed Fund futures.

This is significantly lower than expectations earlier in August, as you can see in the chart below, when the Fed Funds futures was pricing in a 55% chance of a rate rise on the 17th September FOMC meeting.

From a market perspective, this caution on the prospect of a rate hike next month may trigger some interesting market developments in the next couple of weeks:

Figure 1:

Source: Gain Capital