The clash of the currency titans Trump and the FX market

It may seem that all is good with the world now that Apple is selling iPhones like hot cakes once again, however, in the background […]

It may seem that all is good with the world now that Apple is selling iPhones like hot cakes once again, however, in the background […]

It may seem that all is good with the world now that Apple is selling iPhones like hot cakes once again, however, in the background the stage is being set for a clash of the currency titans. On Tuesday an economic aide to President Trump, Peter Navarro, said that Germany was exploiting a weak euro to benefit its own economy at the expense of its trading partners. This is an unusual move from Washington, as Presidential aides do not usually talk about currencies, especially when criticising policies of a close ally. Welcome to the new normal under the Trump administration.

Talking down the dollar

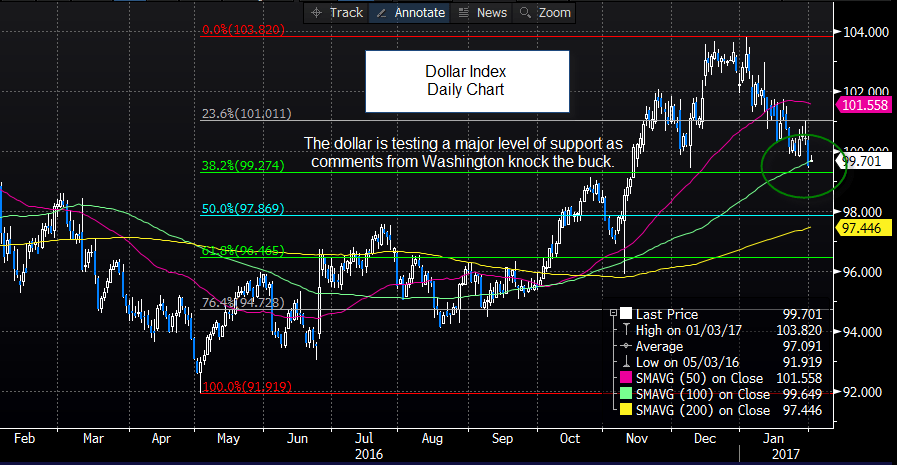

The impact of these comments was immediately felt on Tuesday, and the dollar plunged. EUR/USD reversed course and surged more than 1.5%, and it is still holding onto gains on Wednesday. Team Trump has succeeded in the short0term to weaken the buck, the dollar index fell below the key psychological 100.00 level on Tuesday and is approaching a Fibonacci support level – the 38.2% retracement of the May 2016 low to January 2017 high at 99.27 (see figure 1 below). A break of this level would be a bearish development and would point to further broad-based dollar declines.

President Trump also waded directly into the debate on Tuesday and accused China and Japan of using monetary policy to weaken their currencies one day before the Fed meeting. It is worth noting that six and a half years ago it was the Brazilian finance minister who was decrying a weak dollar and lamenting a global currency war, after the Brazilian real surged to become one of the strongest currencies in the world back in 2010.

So, what can recent history can teach us about politics, FX and currency wars?

Back in September 2010, when the Brazilian finance minister made the comments, the Brazilian real continued to rally, it peaked in July 2011 before embarking on a sustained downtrend that remains in place. This tells us a couple of things: 1, political comments regarding currency valuations tend to have little impact on the large and liquid FX market, 2, it was the detrimental impact of the strong real on Brazil’s economic growth that eventually caused the decline in the currency.

Can Trump weaken the dollar?

While the situation with the Trump team is not an apples for apples comparison with the situation in 2010, it does suggest that verbal intervention by politicians into the currency market does not always go according to plan, and can even backfire. However, Trump is the leader of the world’s largest, and arguably most important economy, what the Trump administration says and does can have a huge impact on global financial markets.

Right now, the dollar index is teetering on an important ledge. If it falls below the Fibonacci support level mentioned above then we could see further declines for the greenback. This may be exacerbated by any further verbal intervention in the FX market from Washington. While the ‘currency wars’ of 2010 barely had an impact on the markets, if the Trump administration continue to meddle in FX then this could be a major theme for 2017.

FX market gets used to new normal for US politics

The Trump administration’s tendency to shoot from the hip could have large ramifications for financial markets. While volatility has remained low so far – there was no noticeable shift in EUR/USD volatility levels after Navarro’s comments – if Trump and co. continue to randomly voice opinions on the level of the dollar, it could trigger a sharper backlash from those in the US’s firing line, and this is when volatility could surge.

Angela Merkel’s measured response to the Trump criticism, saying that Germany can’t influence the level of the euro, dampened concerns about a potential global currency war. However, if this continues, then Trump’s next victim may decide to fight fire with fire, which could spook markets.

The unconventional policy style of the Trump administration is a major departure and is something that investors will have to get used to. Whether or not Trump can get his way and manages to weaken the buck in the longer-term, may also depend on the outcome of Wednesday’s FOMC meeting. Read our preview, to get our take.

Figure 1:

Source: City Index and Bloomberg