The chart to watch ahead of BOE Inflation Report

The pound is likely to be very sensitive to the outcome of today’s Inflation Report released at 1200 GMT, and the accompanying press conference by […]

The pound is likely to be very sensitive to the outcome of today’s Inflation Report released at 1200 GMT, and the accompanying press conference by […]

The pound is likely to be very sensitive to the outcome of today’s Inflation Report released at 1200 GMT, and the accompanying press conference by Mark Carney at 1230 GMT. GBP/USD has had a volatile session so far, it rallied earlier, before falling back sharply in the past hour; however, it remains nearly 2% higher since the start of the week.

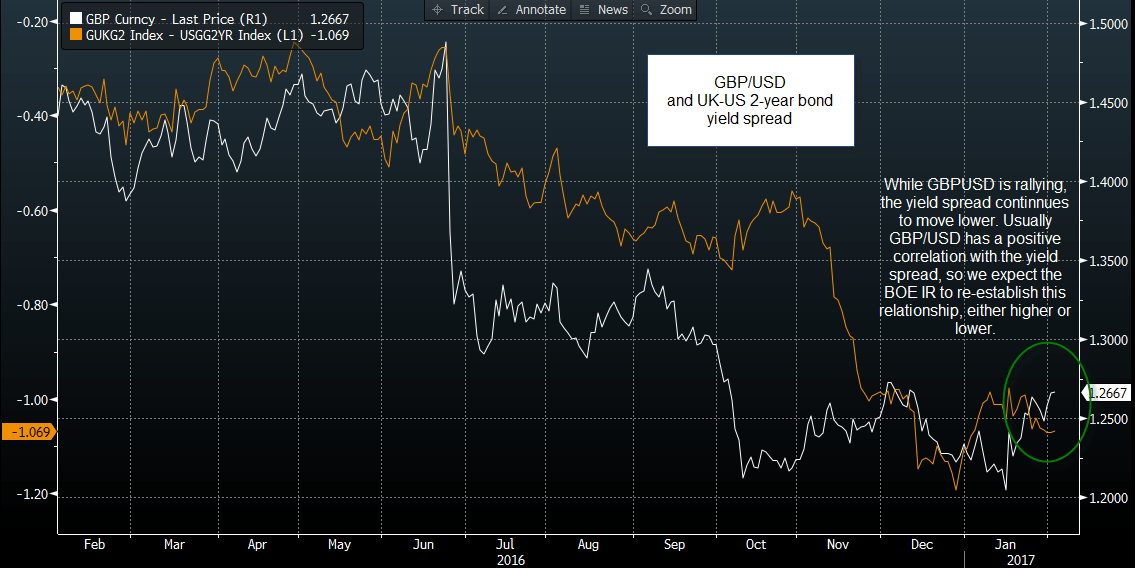

Due to the sensitivity of the pound to today’s IR, it is worth keeping an eye on GBP/USD and the spread between UK and US 2-year yields to get a sense about the market’s reaction to the report.

As you can see in the chart below, GBP/USD is rallying, but the UK-US 2-year yield spread, which is sensitive to shifts in market perception about near term central bank policy, has turned lower once more, suggesting that UK yields have not kept pace with the rally in sterling.

So, is sterling a lead indicator? If BOE sounds more hawkish than expected and revises up its GDP and CPI forecasts substantially, then the rally in sterling could continue, and we would expect the yield spread to turn higher.

However, a surprise dovish tone from the BOE could trigger a sharp fall in GBP/USD, especially since the recent rally is not supported by the yield spread. Key levels to watch on the downside for GBP/USD include: 1.2450-70 – the 100-day sma, while a hawkish BOE could trigger a move back to 1.30.

Overall, while GBP/USD is rallying, the yield spread continues to move lower. Usually GBP/USD has a positive relationship with its short-term yield spread, so we expect the BOE Inflation Report to re-establish this relationship, either higher or lower, later today.

Figure 1:

Source: City Index and Bloomberg