The budget 2014 what investors can expect

On Wednesday 19th March in the House of Commons, at approximately 12.30pm, the Chancellor of the Exchequer, George Osborne, will deliver his latest budget. He […]

On Wednesday 19th March in the House of Commons, at approximately 12.30pm, the Chancellor of the Exchequer, George Osborne, will deliver his latest budget. He […]

On Wednesday 19th March in the House of Commons, at approximately 12.30pm, the Chancellor of the Exchequer, George Osborne, will deliver his latest budget.

He does so in the midst of a UK economic revival that has surprised many – where inflation has finally fallen in line with the Bank of England’s 2% target, popularity for Scottish independence is rising and where many investors, home owners and individuals are now bracing themselves for the reality of an interest rate hike within the next 12 months.

Investors will be watching the budget news with great interest as to how the Chancellor expects to maintain the UK’s growth trajectory.

Theme of ‘the job is not yet done’

Each budget speech has a theme; ‘paying the cost for reckless spending’, ‘green shoots appearing’, etc – the theme this year will likely be, “the recovery is gaining momentum but the job is not yet done.”

Osborne will continue to drive home the mantra that he and the government are the most fiscally responsible to drive the economy forward – and with the knowledge that the most important budget speech is not this one but March 2015 (see below).

This budget speech is not the time to pledge that we can now enjoy the fruits of five hard years of austerity labour. That comes in 2015. 2014 remains a year of hard work, but one in which the hard work is visibly starting to pay off.

With a general election some 14 months away, this budget is likely to be coloured with the beginnings of the government’s economic manifesto.

The Conservative party has essentially three more budget speeches before the UK general election; this one, the autumn statement later this year (November or December) and the 2015/16 budget (likely in March 2015).

Given the fact the latter two reside uncomfortably close to the election, it may be easy to convince that those two speeches will be tainted by election pledges and populist decisions used to garner support for the Conservatives, convince swing constituencies and protect constituencies where the Tory party holds a majority or where the Liberal Democrats can sway the Labour vote.

In that sense, perhaps this will be the final budget speech that may still commit to policies that drive long-term UK growth.

Nevertheless, do not underestimate the ability of Osborne to ‘place’ specific policies now in order to set up a more populist pledge come May next year.

For example, one of the speculated pledges that could arrive on Wednesday surrounds the income tax threshold, which could be raised to £10,500 from 2016.

That specific move will not only boost the Tory’s sway with low income voters but also give the Liberal Democrats a boost given their motivation at the previous election to raise the threshold above £10,000.

Why is this important? The Conservatives will be hoping to give the Liberal Democrats enough support momentum to diversify the Labour support at next years’ election. Of course, this move won’t do it alone, but it will certainly help given the declining popularity of the Lib Dems over the last few years.

One of the greatest dangers to the Conservative party’s ability to be re-elected next year is the expected timing of the first interest rate hike by the Bank of England.

In the last quarterly inflation report, the BoE confirmed market expectations by effectively timing the first rate hike in 12 months’ time, which would fall a month or two short of the general election.

That means Osborne has to try to defend against this expected increase in interest rates or risk facing an electorate whose mortgage bills and debt has just increased right as they hit the polls.

He must do so either through tax relief or pro-growth pledges, both of which create a cushion for individuals who still feel the bite of austerity.

There is little movement the chancellor can make on taxes right now, when austerity remains in flight.

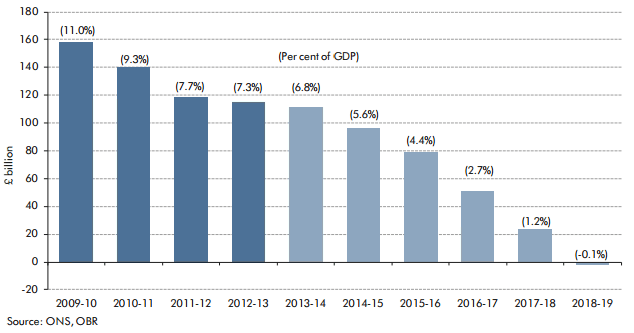

For example, according to the institute of fiscal studies, only 36% of departmental savings have actually been achieved and the budget is not yet balanced – a key pledge of this coalition government – with the deficit as a percentage of GDP, excluding the Royal Mail and asset purchases facility, standing at 6.8% and expected to fall to 0 in 2018/19.

And what’s more, why would this government move on taxes right now (apart from raising the threshold)? The prime time to do so is next year, apart from the obvious connotation that such a decision is being dictated by the election.

First and foremost, expect upward revisions (at least in the very near term) to UK growth by the Office of Budget and Responsibility (OBR).

In the autumn statement, the OBR upgraded GDP projections for 2014 from 1.8% to 2.4%. Given the Bank of England expects growth to come in at 3.4% (seen as somewhat optimistic), the market is expecting GDP for this year to be reforecast at 2.7% or 2.8%. Expect revisions to 2015, 2016 GDP also.

The key will be whether Osborne can announce any pro-growth policies that materially boost GDP over a much longer period of time.

The UK still struggles with output productivity and exports, relying too heavily on consumer spending.

It is in this sense that Osborne needs to show some more teeth, particularly as one way to boost exports is to maintain a weak currency, and the pound has gained in strength on expectations of higher interest rates.

Therefore, we might expect Osborne to extend the £250,000 annual capital allowance beyond its current 2015 expiry to help business investment.

We could also see other reliefs on pro-business and investment measures that are linked to jobs creation and wage growth. Net real earnings remain a constant challenge; so much so that the BoE is taking a greater look at earnings growth within the context of the recovery and timing of rate hikes.

We should also expect revisions to public sector net borrowing figures to be revised, and this will take a strong interest of ratings agencies as well as investors in gilts and sterling. The worst case scenario for the government now would be to announce borrowing will be net 0 a year later to 2019/20 – so we need to watch this carefully.

We already know that the government is investing £200m into creating a new garden city in Ebbsfleet, supporting the building of some 15,000 new homes.

We also know Osborne is extending the new home’s segment of the controversial Help to Buy scheme past 2016 to 2020, which he says will also create 120,000 new homes.

However, there is a chance – albeit a small one – that we could see the £250,000 threshold for stamp duty raised to £300,000 on the basis that UK house prices have been growing strongly over the last few years and the average UK house price, according to the Office of National Statistics, reached £250,000 in December last year.

As has proved common over the past four years, the details of the budget speech are well leaked and there tends to be a lack of surprises.

The BoE’s forward guidance has also tended to leave the budget speech somewhat behind the economic curve, rather than in front of it – making those details even less important. As such, it has become rare that the big markets enjoy big swings on the back of a UK budget speech.

Nevertheless, given the speech’s proximity to both the first expected rate cut in the UK and the general election in May 2015, traders of sterling, UK gilts, retail stocks and oil and gas stocks (particularly those with exposure to north seas oil refinery) need to watch the speech carefully.

The pound typically suffers some volatility depending on the severity of both GDP and borrowing forecasts, and this speech could dictate a somewhat more sensitive edge.

Anything that could put the first interest rate hike at threat could see the pound weaken against the US dollar and Euro. Should borrowing be forecasted to fall at a slower pace, this could also see the pound suffer even more volatility.

And of course, when politics is involved, there will always be a surprise or two so traders need to keep their wits about them ahead of the speech on Wednesday.