The British mid caps earning big dollars

The FTSE 250 index has recouped almost all Brexit vote losses as the pound rises off 30-year lows, though if the pound relapses, some middleweight shares will hold on to gains better than others.

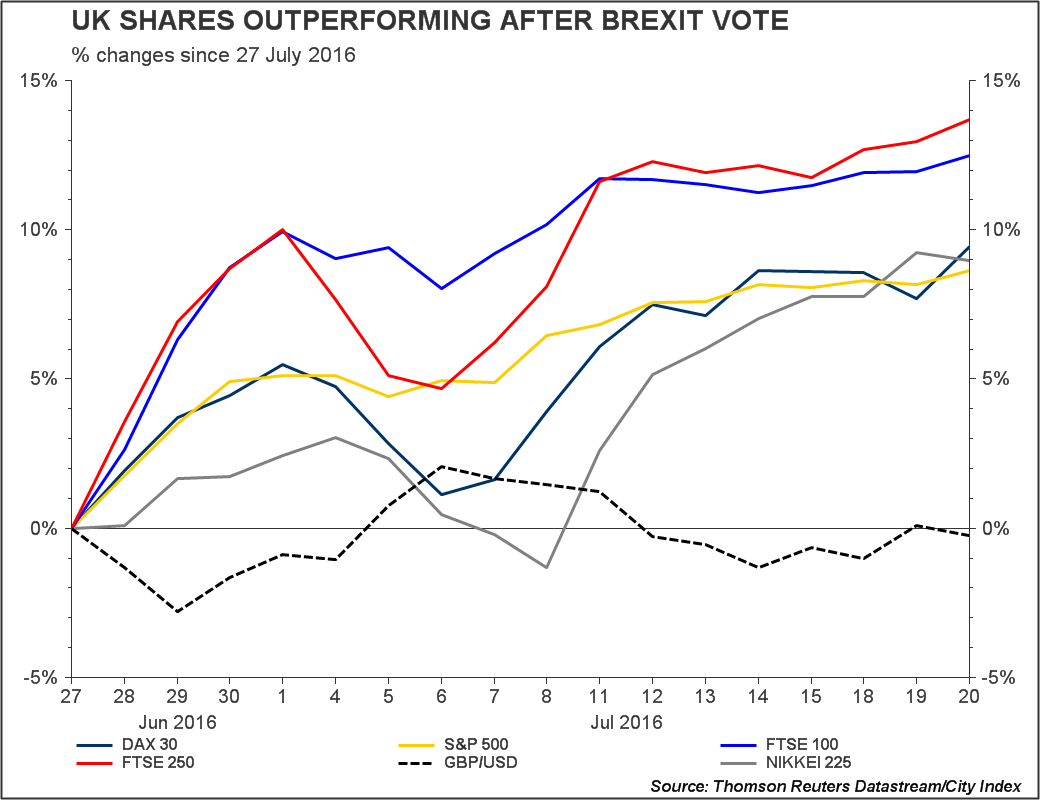

The FTSE 250 index has recouped almost all Brexit vote losses as the pound rises off 30-year lows, though if the pound relapses, some middleweight shares will hold on to gains better than others.

For now, FTSE 250 mid-caps are having their best run since a 14% two-day fall in the wake of the Brexit vote.

Sterling’s bounce is the most obvious reason for the broad rally. Almost 60% of FTSE 250 company sales were in sterling last year vs. 22% of FTSE 100 sales, according to BlackRock.

So, sterling’s 3% rise against the dollar from thirty year lows earlier this month, recharged last week by the Bank of England’s (BoE) decision not to ease, has helped the mid-cap index recoup almost all of its post Brexit loss.

It has even begun to slightly outpace the dollar-fuelled FTSE 100.

Please click image to enlarge

As for the pound, it has strengthened on a string of better-than-expected economic readings, though most were from before the referendum. Resilient US economic data have helped propel the dollar well above early-July lows too, making the pound’s recovery less than streamlined.

The BoE’s next meeting looming just a fortnight away is also cautionary. The Bank said last week it was likely to deliver stimulus, possibly as a “package of measures”.

We think the higher probability of BoE easing will reinstate investors’ recent bias for companies with most costs in sterling and sales largely in foreign currencies. The preference partly explains why the FTSE 100 outperformed all major stock indices in the fortnight following 27th June.

FTSE 250 companies with more regionally diverse sales should outperform too, though there’s a risk they will again be caught up in an indiscriminate sell-off of mid-sized shares like last month’s, if the Bank starts easing.

More positively, sterling’s weak condition is an opportunity to pick up stocks with better chances of outperforming, due to loose ties to sterling.

Not all are large caps.

Smaller miners and oil companies are the most obvious, as all do business in dollars, though risk-averse investors will run for the hills from many of these.

Most that survived commodity price routs are highly indebted and unprofitable and have scrapped dividends.

Ironically the risk-reward balance in Acacia, Centamin, Fresnilo, platinum producer Lonmin, and Petra Diamonds is nowless attractive after surges of 35%-190% in 2016.

Shares which are accelerating but which have not yet to recovered last year’s losses—Anglo, Glencore, Lonmin—may attract the brave.

Either way, these groups will still preserve price gains better than sterling-focused stocks so long as the dollar remains at multi-year highs against the pound.

Remaining SME mining stock opportunities will be found among those that have rallied least, though laggards trail the sector for sound reason. Like exposure to metals with less than sparkling price recoveries, or too-slow debt reduction.

(See copper miner Kaz Minerals whose net debt is 14 times forecast core earnings).

There are even fewer choices among mid-sized oil groups. Excluding the majors leaves only Tullow and Cairn. The rest are in more perilous FTSE SmallCap and AIM waters.

Almost all are running cash deficits and negative operating margins too.

Oil services firms Amec Foster Wheeler and John Wood Group are rare dividend payers. Premier Oil and Tullow are among the more solid explorers. Premier is saving millions of dollars whilst bringing new North Sea fields on stream in sterling.

Tullow is expecting a $500m insurance payout and its large TEN fields project, offshore Ghana, starts production within weeks.

A handful of FTSE 250 shares outside of the energy sector, have significant dollar exposure that’s less easy to spot.

Transport group Stagecoach and Tate & Lyle are the household names among these.

Stagecoach’s US business contributed $552m of sales in its last financial year; Tate’s US arm generated 78% of revenue worth around $2.4bn.

Engineer Meggitt, business publisher UBM and packaging group DS Smith also come out top among FTSE 250 shares, on dividends, cash in the bank, and debt.