The BOE shifts the goal posts makes it harder to raise interest rates

The market has interpreted the first Inflation Report of the year as dovish in tone, UK yields have fallen alongside the pound, which is nearly […]

The market has interpreted the first Inflation Report of the year as dovish in tone, UK yields have fallen alongside the pound, which is nearly […]

The market has interpreted the first Inflation Report of the year as dovish in tone, UK yields have fallen alongside the pound, which is nearly 1% lower since the Report was released. In contrast the FTSE 100 is rising. So, what made this Report so dovish.

We think two things have made the market reassess the BOE’s willingness to hike rates in the foreseeable future: 1, it did not increase its inflation forecast, and now expects inflation to peak at 2.8% in 2018. 2, the Bank lowered the equilibrium rate of unemployment to 4-4.75%, from 5%. Thus, the UK unemployment rate, currently at 4.8%, could fall substantially before the BOE would consider this an inflation risk. These two developments are worth watching closely.

Inflation forecast suggests that rate hike could be years away

As mentioned, the BOE kept its inflation forecast broadly unchanged, and prices are meant to peak at 2.8% next year. CPI peaked above 5% in 2011 and they still didn’t raise interest rates, thus, with inflation forecasts at this level, history suggests that the BOE won’t hike rates for a long time yet, and definitely not on the back of currency-fuelled CPI pressures.

Bank moves the goal post on unemployment rate

The Bank of England announced that it has lowered its equilibrium rate for unemployment to 4-4.75%, down from 5%. This could have major implications for monetary policy going forward. As stated in the Inflation Report: the “MPC now judges that the unemployment rate can probably fall a little further before wage pressures build significantly to keep the inflation rate at the 2% target over the medium term.”

Right now the UK’s unemployment rate stands at 4.8%, which means that it could fall substantially further before it leads to stronger wage growth and thus threatens the BOE’s inflation target. The Bank expects wage growth to pick up only gradually. It noted that wages and productivity growth tend to move together over time. Since the BOE expects productivity growth to remain weak, it thus expects wage pressures to be kept in check, even if pay moves higher temporarily due to January bonus payments.

Wages the key metric going forward

This Report was all about inflation, and the BOE’s technical diagnosis of the UK economy suggests that inflation pressures won’t require any remedial interest rate increases in the foreseeable future. One thing that could spur the BOE to hike interest rates would be a significant pick-up in wage growth, the IR states that ‘if pay growth picks up by more than anticipated, monetary policy may need to be tightened to a greater degree than the gently rising path implied by market yields’.

This small chunk of the 45 page report tells us something very important: watch wage growth like a hawk going forward. If pay packets continue to rise strongly then a rate rise will be on the cards. However, pay packets may not surge substantially until the labour market experiences a squeeze, which may not be until we leave the EU in 2 years’ time, or if immigration controls are tightened during the negotiation phase once the government triggers Article 50 next month.

BOE and Trump on same page regarding unemployment rate

Donald Trump stated during his election campaign that the unemployment rate was a “phoney” way of determining economic strength, even though the Federal Reserve hiked interest rates last December because the US economy was considered to be near full employment. Trump’s economic team have suggested that a new measure should be used, the U-5 rate, which includes discouraged workers, or workers who have left the workforce altogether, and part time employees who want full time work.

This is more radical than what the BOE did today: Carney and co. still intend to view the unemployment rate, whereas the Trump team wants to change the employment metric altogether. The Fed did note in its statement on Wednesday that there is still room for improvement when it comes to the jobs market, and Yellen and co. do look at alternative measures when deciding policy. However, outright ditching the unemployment rate and choosing another measure could lead to confusion over the expected trajectory of monetary policy in the US, which may trigger excess volatility in financial markets. So watch out for any unemployment themed tweets from Donald Trump, especially during Friday’s NFP release.

The BOE’s move to lower the equilibrium unemployment rate, shares the same goal of the Trump team, but is a less radical, more easily digested move that essentially reduces the chance of a rate hike until the unemployment rate falls even further.

Thus, changes in monetary policy could be delayed both in the UK and the US if the unemployment goal posts are moved, and the prospect of three interest rate hikes from the Federal Reserve this year may start to look a bit rich.

The impact on the pound:

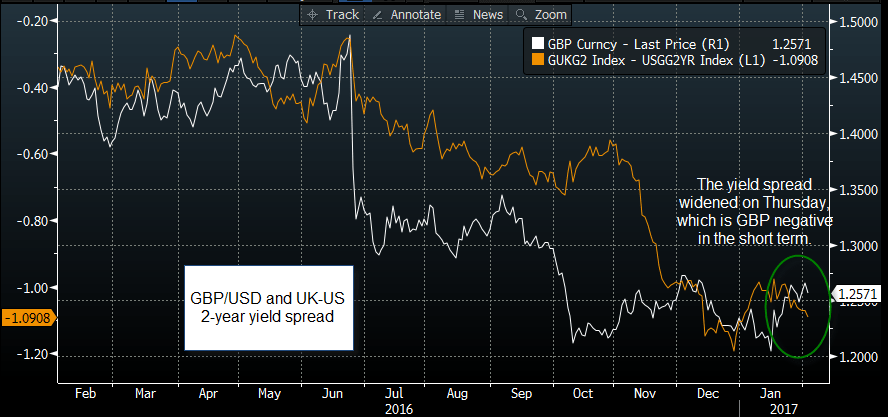

The BOE Inflation Report has significantly weakened the pound on Thursday, and it is nearly 1% lower this afternoon. The break below 1.2580 was a significant bearish development that opens the way to 1.2470 – the 100-day sma – which could act as short-term support. Added to that, the UK-US short term yield spread has also moved lower, which further erodes support for the pound (see chart below.)

Overall, the market has viewed this Inflation Report as dovish for the two reasons that we outlined above. The BOE is on hold, and we don’t expect the Bank to raise rates for some time to come.

Figure 1:

Source: City Index and Bloomberg