Tesco shares set to pause on flat 8216 aspirations 8217

One grim ‘advantage’ big UK supermarkets have with investors: expectations are low and will remain so, perhaps for years. With the ‘Big 4’ grocers battered […]

One grim ‘advantage’ big UK supermarkets have with investors: expectations are low and will remain so, perhaps for years. With the ‘Big 4’ grocers battered […]

One grim ‘advantage’ big UK supermarkets have with investors: expectations are low and will remain so, perhaps for years.

With the ‘Big 4’ grocers battered by losses, write-downs and more, as they struggled to meet the challenge of ‘hard discounters’, their sales languished between anaemic single-digit growth or inexorable retreat.

Against this backdrop, Sainsbury’s quarterly store sales slippage of 1.1% was welcomed by shareholders as a relative achievement last week, sending the stock as much as 17% higher.

Investors haven’t cheered Tesco’s results on Wednesday so emphatically, even though its CEO Dave Lewis proclaimed they showed “sustained improvement across a broad range of key indicators.”

The shares traded as much as 3.8% lower earlier, albeit they’d risen 17% from late-September lows up till Tuesday’s close.

From a cursory reading, Tesco, just like Sainsbury’s, managed to beat many low City expectations.

(Note, ‘like-for-like’ (LFL) sales exclude fuel)

Tesco’s results arguably ticked ahead of the pack too; Sainsbury’s, Asda’s and Morrisons’ quarterly sales dipped between 1.1% and 2.4%.

The price though has been continued price cuts at their biggest rival, in one form or another.

Unlike at Sainsbury’s, most particularly, which said last week it trimmed promotions, there’s little sign of discounts slowing at Tesco, after it boasted of “500 additional reductions on key product lines”.

Efficiency metrics have moved in the right direction under the technocratic Lewis, with an average three days’ less worth of stock in the first half than a year before.

But profitability suffered, tanking deeper than most market expectations by 55% to £354m from £779m.

That’s using Tesco’s newly favoured earnings measure: unadjusted operating profit, AKA Earnings before Interest and Taxation (EBIT).

Underscoring the sense that Tesco investors are now those who are satisfied with slimmer operations and only a distant hope of material profit rises, Lewis also backed “aspiration” for flat annual profit.

“We’re on track to meet that aspiration notwithstanding that there are some challenges still in the second half of the year,” he told reporters.

The target is £950m, which removes the better-than-expected £4.2bn Tesco fetched from the successful (if long-winded) disposal of Homeplus in South Korea.

Operating profit last year was £1.2bn, excluding one-offs.

Additionally, the balance sheet should now be much less of a concern. (Again, see Homeplus).

That in turn has reduced the urgency of any residual disposal programme.

It has also emboldened Lewis—as we long expected it would—to announce that the other high-profile business on the block, ‘Clubcard’, will now not be sold after all.

Clubcard was one of the first digital customer data, relationship and retention businesses in the world (with the less catchy official name Dunnhumby).

It now looks rather more strategic—especially with cash crunch risk averted—in view of the high-tech retail citadel Lewis is undoubtedly fashioning.

Amazon/Google-like benefits from Clubcard will naturally be some way off though.

And that leaves just a studier, steadier ship in the retail storm, with less ballast, but with the ‘pirate’ threats from Aldi et al intact.

ASDA, Sainsbury’s and Morrisons can be expected to vie for marginal second and third place in terms of market share for the foreseeable future too.

For Sainsbury’s at least, its moderately stronger exposure to London and the South East may be an edge Tesco needs to worry about in the medium term.

But none of these names have given themselves a great deal of room to manoeuvre in yet.

Or margin for error.

For Tesco in particular, a fair final verdict on its half year is that investors may not have a great deal to complain about, on a relative basis, of course.

Traders may see things differently.

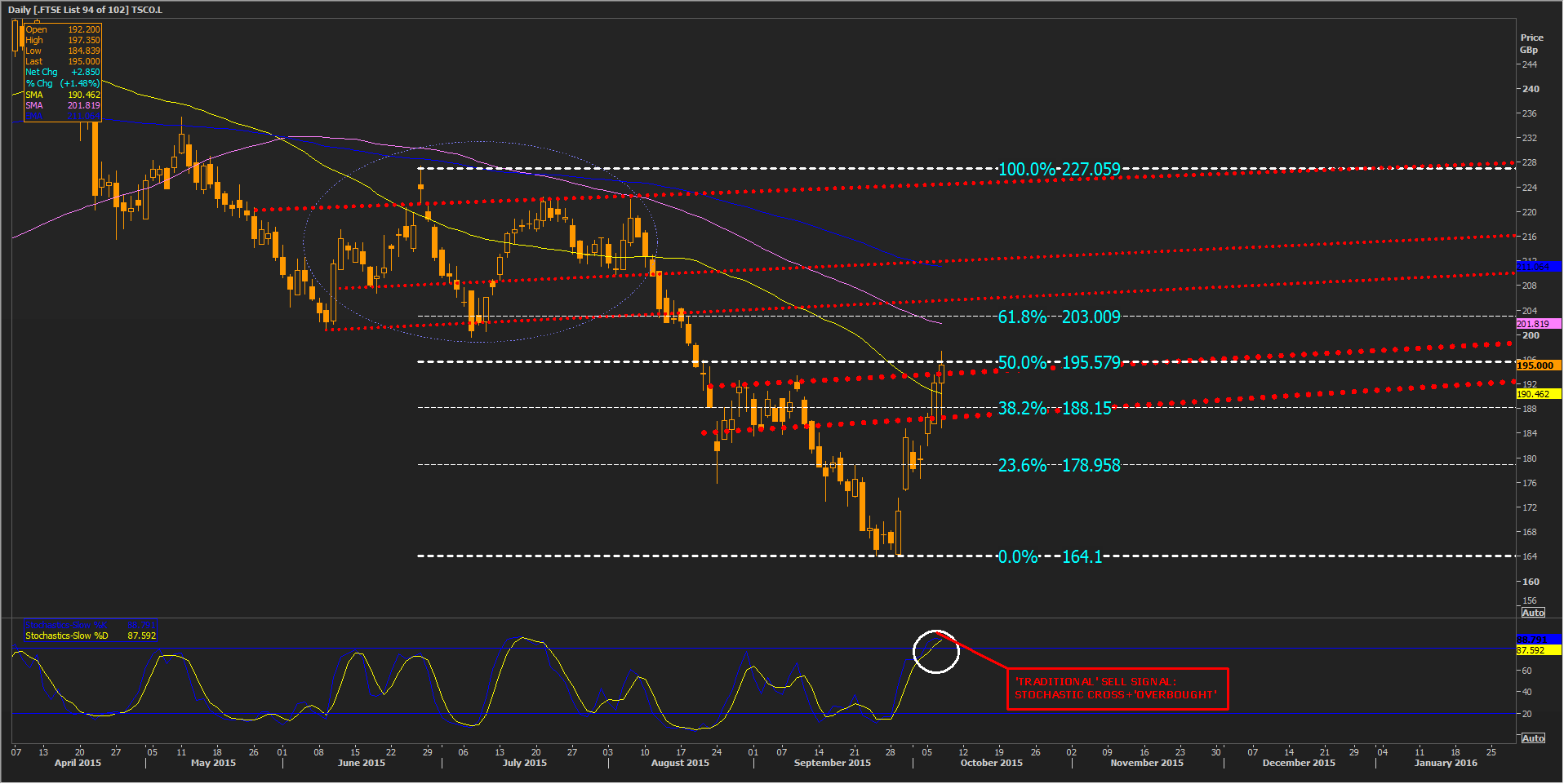

With Wednesday’s afternoon gain of 1.5%, the stock has now retraced about 50% of the decline from June highs (227p) to September lows (165p).

It’s still within the potential influence of a band of resistance formed by the consolidation in late August-September (184p-192p).

Beyond the above band, the stock could probably also use a faster run-up to take the resistance inherent from the inverse head & shoulders pattern between 8th June and say, 13th August.

The 100-day moving average hovers overhead at 203p, whilst a sentiment weather vane, the Slow Stochastic, crosses in the ‘overbought’ zone as this article goes on line.

Please click image to enlarge