Tesco shares need undramatic end to 2015

For a retailer whose key sales have continued to decline, almost consecutively, for about two years, Tesco’s shares have put in a respectable rise […]

For a retailer whose key sales have continued to decline, almost consecutively, for about two years, Tesco’s shares have put in a respectable rise […]

For a retailer whose key sales have continued to decline, almost consecutively, for about two years, Tesco’s shares have put in a respectable rise so far in 2016.

True, though more than 30% higher, they’re lagging Morrisons’ a little.

But the UK’s fourth-largest grocery chain by market share has had a more dramatic 12 months.

Morrisons’ shares are rebounding furiously to recover after it reported its worst profits in eight years; was booted from the FTSE 100 and then re-admitted to the top UK index; all in the space of a year.

By contrast, supermarket No.1 has had a relatively sedate 2015/16.

That was perhaps inevitable, after the group hit the skids in an annus horribilis of much drama in 2015, when it reported one the biggest losses in British corporate history.

That year will continue to haunt Tesco though, providing an inescapable prism through which 2015/16 will be judged, not least because investors can be expected to react coolly if the group only has the relatively low-hanging fruit of not performing as badly as in 2014 to offer.

After disposals of key assets like South Korean giant Homeplus, the US part of its Clubcard operator Dunnhumby, broadband and streaming outfits and the Giraffe restaurant chain, what has Tesco achieved since?

We expect a relatively low-key but emphatic pitch from Tesco to investors in its final earnings that will be released on Wednesday 12th April.

The group will probably again point to a recovery which it has already indicated is underway, whilst making clear the comeback remains in its early stages.

So far, markets have responded well to similar iterations of this implicit message from the CEO’s management team and of course ‘Drastic Dave’ Lewis himself.

(He is known for slashed product ranges, and sadly, massive job cuts, which may not be over yet, if reports in The Guardian in February of a potential 40,000 more, prove correct.)

At some point, Mr Drastic will reach ‘Peak Cuts’.

Investor ire at that point if market share and revenue growth still stubbornly refuse to rise could be considerable. After all, his strategy is basically price cuts to boost demand.

But we’re not there yet.

Independent and official retail data for the last few quarters, whilst still mired in negative territory, arguably show Tesco’s thoroughly revamped customer service plan, steps to get suppliers back on side, and yes, price cuts, though hand-in-hand with better availability, are having the desired effect.

A March reading by retail researcher Kantar Worldpanel had Tesco sales down 0.8% over a 12-week stretch, but that was better than the 1.6% slide from the month before. And the group’s sales improved for a fourth straight month in 12 weeks ending on 27th March Kantar said last week, this time with a fall of just 0.2%.

It’s worth bearing in mind that the ‘Big 4’ are in fact fighting back against the German retailers (Aldi, Lidl) across the board, so investors should be wary of applauding just Tesco too loudly.

For additional perspective, consider that Lidl remained Britain’s fastest growing supermarket with sales up 17.7%. Aldi’s rose 14.4%, giving it a record-high market share of 6%.

The pair and their imitators plus other ongoing pressures could yet snuff out signs of forthcoming ‘green shoots’ for Tesco and its largest rivals.

These are of course, not standing still. Sainsbury’s is the case in point, growing sales at a faster rate than Morrisons, Tesco and Asda, for the ninth survey period in a row. Its share price has underperformed despite that achievement largely because of its planned purchase of Home Retail Group.

For now though, if Tesco can at least match Dave Lewis’ ‘hope’ that the group would make operating profits of around £940m (steady on the year) before ‘one offs’ (there’s still scope for quite a few) it would be a strong first step towards maintaining market favour, despite the mention of ‘dividends’ being unlikely for some time.

That would make Q4 the group’s first positive one for over three years.

Don’t upset the apple cart Tesco.

It would be a doubly inopportune time to do so, given wider troubles ahead.

Our view is that consumer-facing sectors, large-cap and small, offer among the weakest defence against market uncertainty pre-EU Referendum.

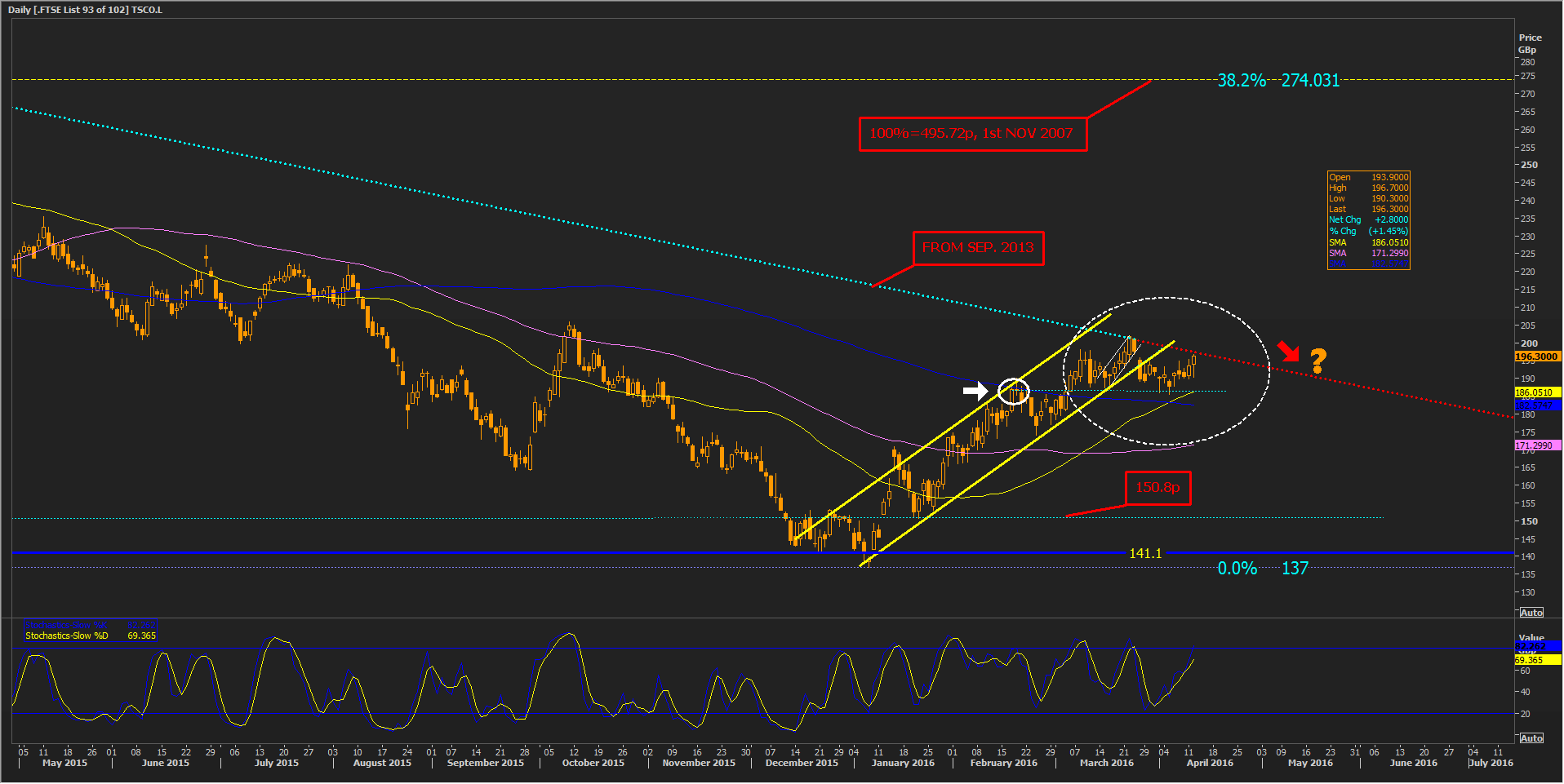

This factor may be in play just as much as any Tesco-specific shareholder misgivings in the near-term, if the stock’s recent firm performance (up 43% from over 18-year lows in December) should stall, as charts suggest it might.

TSCO has yet to break above the declining line from about 30 months ago, and has recently collided with it in disorderly fashion, though has confirmed suspected support stemming from a strong close near the day’s highs on 17th February (white circle).

Less helpfully, the line, around 186p, is triangulating with the overhead trend and pointing to later this month or early in May as a decision point, though support is roughly backed by the powerful 200-day moving average (MA).

Whilst the latter looks to be tipping lower, a potential ‘golden cross’ from the yellow 50-day MA will help maintain more optimistic sentiment.

Further attempts to break higher in the near term look likely.

It is clear that trade above the downtrend would provide the best prospects in the medium term for continued gains.

Below, if the medium-term average doesn’t hold (see lilac 100-day MA), support may be offered at 150p-ish, though that level may be deceptive given that a greater number of settlements were below it when it was resistance in December than above it when it was support in January.

Regardless of direction, the technical picture suggests that rather like Tesco itself, further pronounced share price drama in the near-term-to-medium appears unlikely.

Please click image to enlarge