Tesco shares hinge on CEO after record loss

Updated 1254 BST Tesco’s final results for 2014 were a fitting way for the company to cap its most challenging year for decades. In a move […]

Updated 1254 BST Tesco’s final results for 2014 were a fitting way for the company to cap its most challenging year for decades. In a move […]

Updated 1254 BST

Tesco’s final results for 2014 were a fitting way for the company to cap its most challenging year for decades.

In a move long anticipated by investors, the firm has written down the value of its stores by £4.7bn, pushing its bottom line into the red by £6.38bn, its worst-ever annual loss.

The statutory pre-tax loss was moderately deeper than even the most pessimistic forecasts by City analysts.

However, it’s worth remembering there is a large element of intent and flexibility in specific corporate crisis situations of the kind Tesco has been in.

I see fair evidence that Tesco’s freshened management team under CEO Dave Lewis, who joined from Unilever in October, sought to bundle several further impairments and write-offs into 2014 finals beyond the property write down, in order to clear the decks for their turnaround plan proper.

From that perspective, the impact from today’s grave disclosure may not be profoundly negative for the stock.

In fact the shares traded 2% higher about an hour into Wednesday’s session, probably helped by a number of measured positive comments peppered within this morning’s report

Later, the early fillip to sentiment was tempered by inevitable reality checks voiced by Tesco’s chief executive, on top of the still considerable challenges evident in its final 2014 report.

“To rebuild our profit this year even back to the level of what we achieved last year isn’t without its challenges,” Lewis told reporters, underscoring his comment in the results statement that Tesco was “not expecting any let up in months ahead”.

The upshot of these challenges could well mean that trading profit could be even lower than the £1.4bn of this year, Lewis suggested.

“Our aspiration is to maintain the profit level at what it was last year but you should understand that if we feel we have to make further investments to keep the momentum of the business going … we would,” Lewis said.

These cautions from the CEO back a strong impression left from the morning’s news that management would be more comfortable if consensus forecasts for the current year were somewhat lower.

However, in view of better-than-expected UK operating momentum –the EBIT loss was £32m when some market forecasts projected a loss of as much as £200m—even factoring in the further retail profit decline CEO Lewis warned of this morning, Tesco’s chances of ending 2015 with a profit seem better than those for 2014.

It might also be worth noting that since the £570m inventory related charges announced today were predicated on ‘forward-looking provisioning methodology’, there may scope for beneficial releases later in the year.

Beyond the above, earnings visibility remains one of Tesco’s significant problems.

From the market side, I don’t regard price-to-earnings ratios for Tesco as helpful yet, following last year’s catastrophic loss of market value.

Current consensus points to 22 times FY 2015 forecasts.

That could be accurate, or a mirage.

Having said that, Tesco shares currently price less than 17 times earnings forecast for the year ending in February 2017.

Even on the most sceptical assessment of management capability, that multiple represents an excessively pessimistic average growth rate, in my view.

Tesco is not currently a dividend play and it pales alongside many proven retail growth plays.

But if, as I suspect the investment case has, in effect, become largely a bet on the talents of Tesco’s new management team, favourable sentiment towards Dave Lewis & Co. is yet not fully reflected in Tesco’s shares.

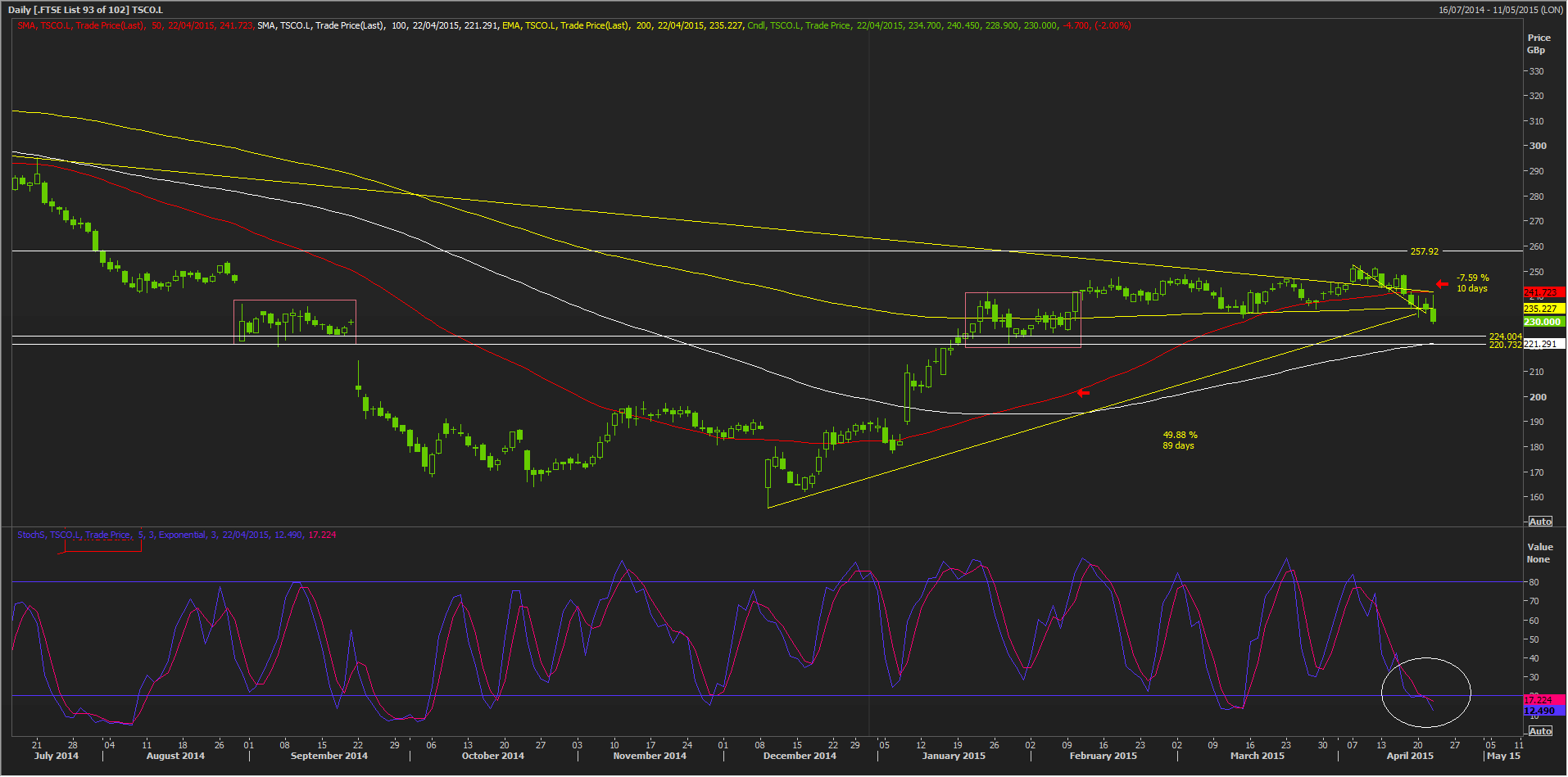

This underlying scepticism may have a price, judging by the stock’s daily chart.

It looks to be no lower than 220p-224p; at least the stock hasn’t traded below that band since January.

On top of that, the stock has now been sold ‘hard’ on a daily basis, according to the ‘slow’ stochastic indicator sub-chart,

There is no formal ‘buy’ signal yet, but there will be in the near-medium term.