Tesco sellers may be eyeing 157p

Tesco Plc. shares crept off the lows they slumped to this morning, closing nearer to 7% lower on the previous session compared to the better […]

Tesco Plc. shares crept off the lows they slumped to this morning, closing nearer to 7% lower on the previous session compared to the better […]

Tesco Plc. shares crept off the lows they slumped to this morning, closing nearer to 7% lower on the previous session compared to the better part of 9% lower earlier in the day.

Following a second profit warning in two months from the UK’s largest retailer together with a 75% cut of the dividend and investment spending, the starting date of the turnaround specialist appointed as chief executive to replace the departing Philip Clarke was brought forward by a month.

Tesco now sees for 2014/15 trading profit in the range of £2.4bn-2.5bn compared with £2.7bn to £2.8bn analysts had been expecting before, a 25% fall against last year, the third such decline in a row.

As was seen on Wednesday this week, Tesco’s sales decline has worsened, amid the weakest overall market growth in a decade. Tesco’s fell 4% in the 12 weeks to 17th August whilst its market share has fallen to 28.8% compared to 30.7% early in 2011.

The major causes of Tesco’s decline are well known to investors, so in a nutshell: competition from discounters (like Lidl and Aldi) as well as the ‘premium’ end (Marks & Spencer) a costly failed gamble by historic management in large ‘hypermarket’ style stores, just before shopping habits changed to include more online purchases and at local stores. Not to mention the less than successful overseas ventures.

Obviously the hope is the interim dividend (and implied cut to the final dividend) and capital expenditure cuts, estimated to bring savings of up £1.3bn, will be ploughed into investments in ‘margin’. Meaning cheaper retail prices for you and I (at the expense of rivals such as Sainsbury’s and others, whose share prices today were already anticipating the pricing pain Tesco might be capable of inflicting).

Statements by the company today suggested other cost-savings were being considered, with attention appearing to focus on Tesco’s status as Britain’s largest private sector employer with headcount of 500,000.

Also there appears to be potential for a review of the sprawling property portfolio hand-in-hand with the introduction of new store formats to respond to changing retail shopping habits with an offering to go head-to-head with discount brands, one for the mid-market and a one for the high end.

If any of these tactics have an air of familiarity about them to you, your recognition is correct: many similar strategies were executed by a similarly beleaguered Sainsbury’s in the middle of the last decade, when its then CEO Justin King halved the dividend and margins for the sake of price cuts.

Few would doubt Tesco is doing the right thing, if not at the right time—earlier would have been preferable.

We may learn on 1st October how much confidence current management has in the ability of the strategic moves to deliver the desired effect, when the new CEO David Lewis may present some initial thoughts with the super market chain’s interim trading results, with profit currently expected to come in at $1.1bn.

In fact, whether Lewis chooses to do a complete verbal washout and present an overly pessimistic scenario (for Tesco to potentially outperform by a laudable small margin) of if he decides to express more optimism, is almost immaterial for the medium term.

Tesco is not a ‘distressed’ name by any means, even if it faces further ugly times before a recovery estimated by retail analysts to be at least two years into the future.

Debt to equity by the close of the session today stands at a healthy 76.2% for the last 12 months compared to a reasonable 46.4% for Sainsbury and Wm. Morrison’s good showing of 64.6%.

(Compare the UK supermarkets with France’s Carrefour SA which is on 119.1%, or its rival, Casino Guichard Perachon SA on an intriguing 155.8%!)

Tesco’s interest coverage is (especially now, after the dividend cut) a similarly robust 9.2 times compared to a European peer median of 4.7 times.

I prefer to focus on the fact that whilst we ‘the consumers’ are likely to benefit from Tesco’s widely expected cost cuts, the real pain will be felt in more remote ways.

Not all of us will be ‘retail investors’ seeking what had been Tesco’s solid yield of 6% before the dividend cut. But most of us will have pensions managed by funds which are all but obliged to hold stocks like Tesco.

Larger shareholders will now have to take evasive action either by reducing holdings, or resort to the darker arts of financial market protection.

Interestingly, there has been a spike in selling of near-term puts related to Tesco shares today. (An investor would choose to sell a put option if her outlook on the underlying security was that it was going to rise.)

Even so, compared to the enormous volume of 8.11bn free floating shares, it’s possible to over-estimate the significance of what looks to be a large open interest in Tesco Dec 6 240p puts expiring on 16th December. These are going for 30.75p.

Perhaps though, the increase in put selling may be indicative of a very cheap means of hedging a much more pronounced short strategy in the underlying stock or, more likely, some derivative.

It’s the short side where we expect the majority of interest to lie, late into the year.

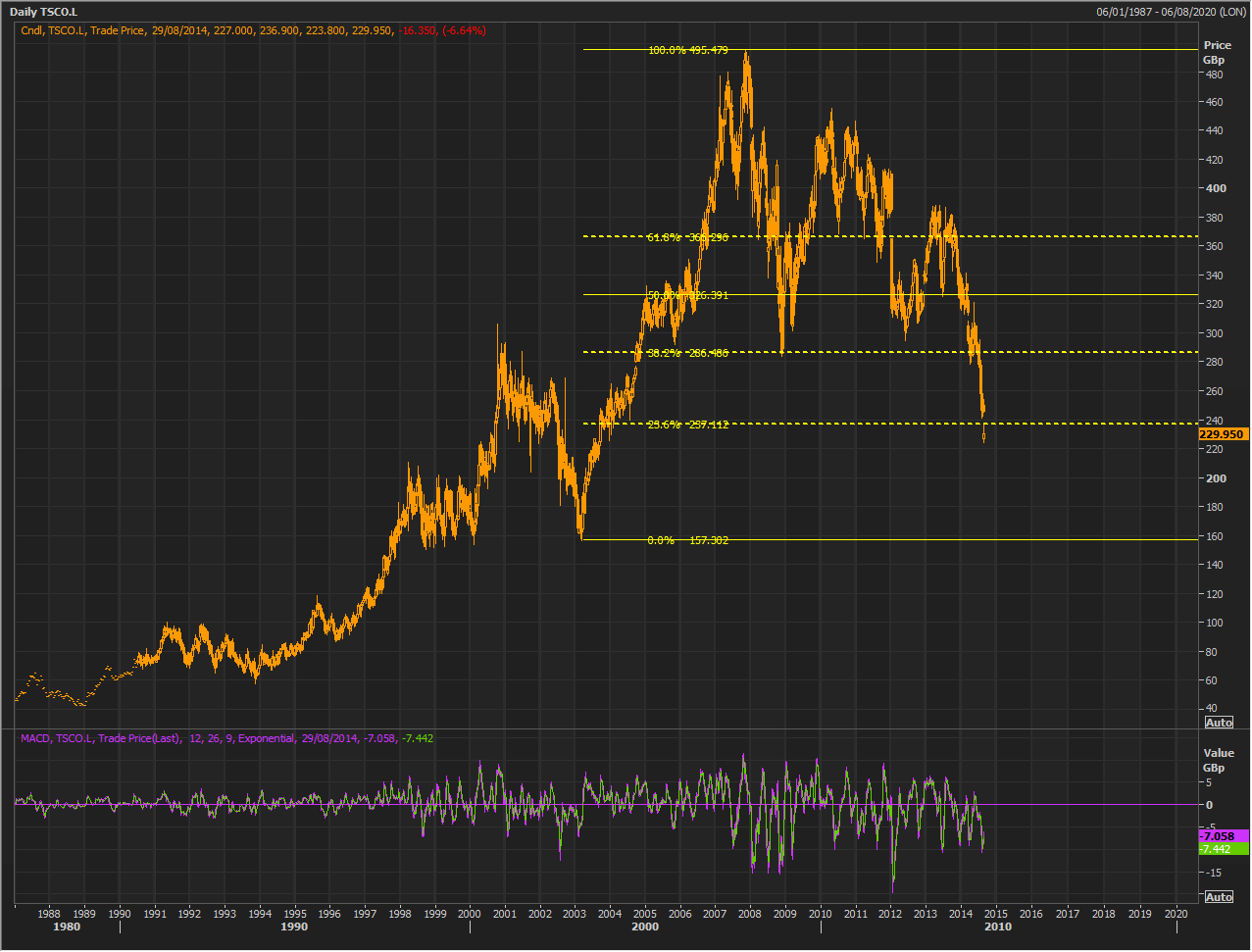

Tesco shares were last at current levels in the early 2000s, recovering from what looks like a stock-specific rout starting in October 2010.

I therefore map Fibonacci retracements from the start of the rise in 2003 up to the peak around 495.50p at the end of March 2007.

This reveals today’s gap as being close to a relatively porous 23.6% as the MACD prepares to cross below the signal line, potentially denoting a time to sell, especially below the zero line which is suggestive of greater momentum to the downside.

Conservative sellers would be likely to go for prices beyond 220p but perhaps not much lower than 200p at most, in the medium term.

More aggressively, the potential for a revisit to the 2003 bottom slightly below 160p could also be a temptation for some.