Ted Baker a fashion contender on first half results

Ted Baker Plc. the British mid-tier fashion retailer has reported excellent first-half results including a 33.8% jump in pre-tax profit to £15.6m and revenues up […]

Ted Baker Plc. the British mid-tier fashion retailer has reported excellent first-half results including a 33.8% jump in pre-tax profit to £15.6m and revenues up […]

Ted Baker Plc. the British mid-tier fashion retailer has reported excellent first-half results including a 33.8% jump in pre-tax profit to £15.6m and revenues up 17.4% at £182.2m.

Before one-off items, profit for the 28 weeks ending on 8th August was up 24.2% at £14.4m.

Ted Baker also announced an 18.9% rise in its interim dividend to 11.3p per share.

“We have successfully opened new space in our international markets, with further planned for the second half of the year in line with our strategy,” said Ted Baker’s CEO Ray Kelvin.

The FTSE 250-listed firm is being increasingly perceived as a contender within a distinct segment of the high-street fashion sector catering to consumers who may be prepared to pay slightly more for clothes than prices in the ‘value’ segment (e.g., Primark) but not quite as much as the ‘luxury’ end (e.g. Burberry).

Its UK high-street fashion peers include names like All Saints, Zara (owned by Spain-based Inditex SA) SuperGroup Plc., GAP Inc., with perhaps its pre-eminent rival being the larger and slightly longer-established Next Plc.

The emergence of this group, which has long been dominated by Next Plc., obviously provides investors in the space with increased choice, though only a handful in the sector are listed.

Ted Baker may also be winning enhanced attention after rival Next said earlier this week it might have to lower its full-year profit guidance range from £775m-to-£815m, citing an unseasonably warm September.

Next also said unseasonably cold weather in August had been a benefit.

Investors seem suspicious of Next’s explanation for the period of poor trading and have sold the stock more than 5% lower over the last 5 sessions.

As for Ted Baker’s performance during the period, its CEO Ray Kelvin told news agency Reuters this morning: “Business has been good, we’ve got good quality products, obviously we probably would have done even better in the last few weeks had we had a colder snap, but we’re in a good position”.

Any perception Ted Baker might proving to be a more stable and perhaps faster-growing ‘pure’ high-street fashion play than Next, could obviously call for a re-think of its place amongst its peers.

Generally speaking, the firm has a record of growth in good times and resilience when trading is tough (it last issued a profit warning in 2001).

Another point of comparison ought to be the proportion of growth coming from online purchases.

Ted Baker doesn’t appear to break out online retail figures, but Next’s online Directory business has put in a strong performance over the last few years with UK and overseas growth of 16.2% in the half year ending in July 2014.

For its first-half, Ted Baker continued a trend of reporting firm overseas retail sales. These make up 30%-40% of its revenues.

Online or offline, the strong international showing makes it a good competitor of such online-focused fashion retailers as ASOS Plc.

Whilst Ted Baker can barely be thought of as a growth stock with a trailing dividend yield of 1.8%, its 20.3 rating on a price/earnings basis might be the most credible of its close peers, especially if Next Plc. is confirmed to be on shaky ground by the end of the year.

Much larger rival Inditex trades on a current PE of 24.3. Next is on 15.2

Ted Baker said a new store in Las Vegas as well as concessions elsewhere in the United States and in Europe had opened in the half, with plans to open new stores in Miami, Toronto and London’s Heathrow airport by the year end.

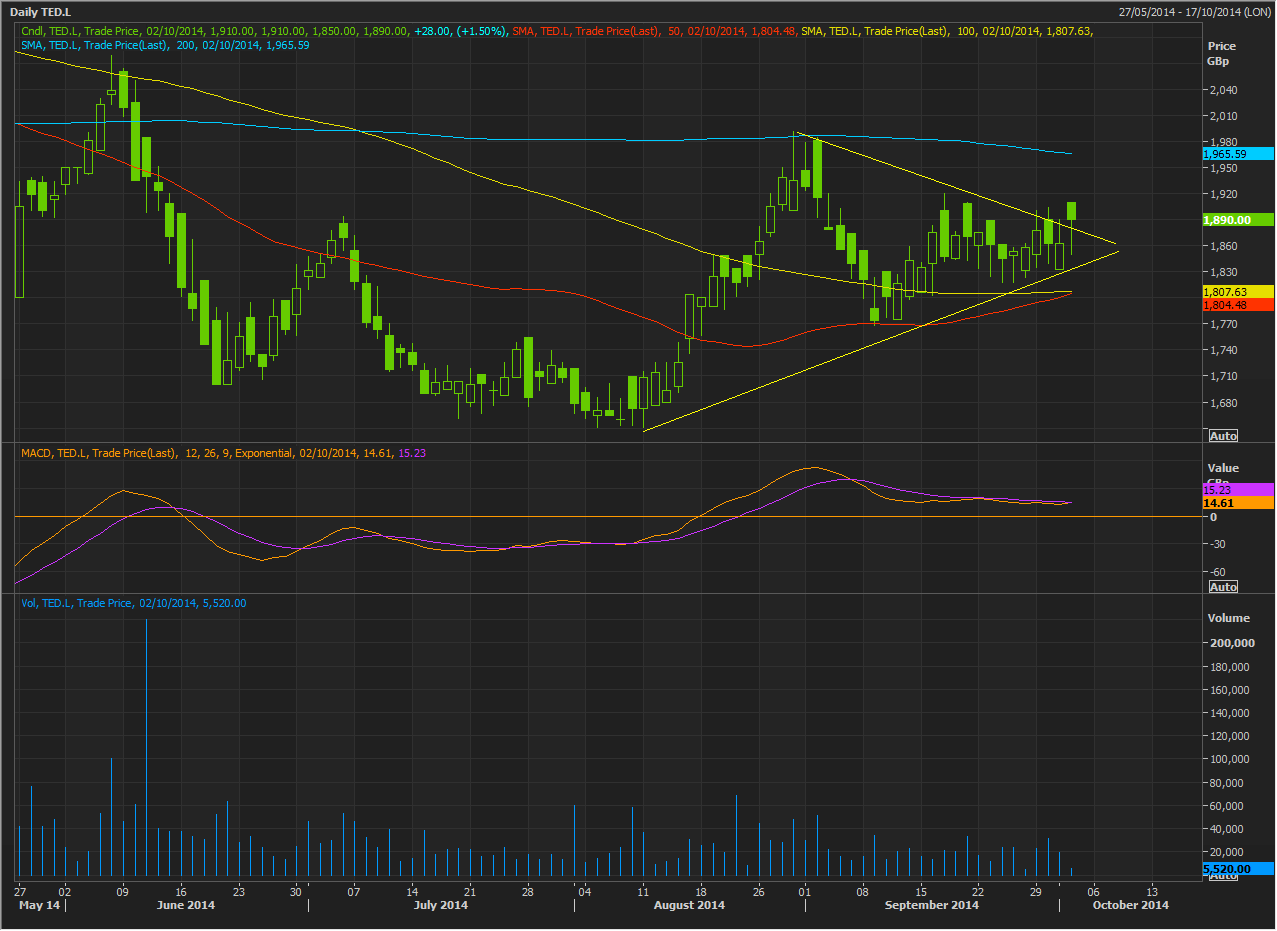

The chart for the stock reflects a number of years of steady progress by Ted Baker, with a pause earlier in the summer, though the shares look to be rising in orderly fashion off a base of 1672p set in August.

They need to close above today’s low of 1850p for continued upside progress in the near term.

They need to also preferably close above a line descending from a peak marked late in August.

The closest point of the line from the market price is around 1880p.