Asian Futures:

- Australia's ASX 200 futures are down -20 points (-0.27%), the cash market is currently estimated to open at 7,361.10

- Japan's Nikkei 225 futures are up 160 points (0.55%), the cash market is currently estimated to open at 29,185.46

- Hong Kong's Hang Seng futures are up 99 points (0.39%), the cash market is currently estimated to open at 25,508.75

UK and Europe:

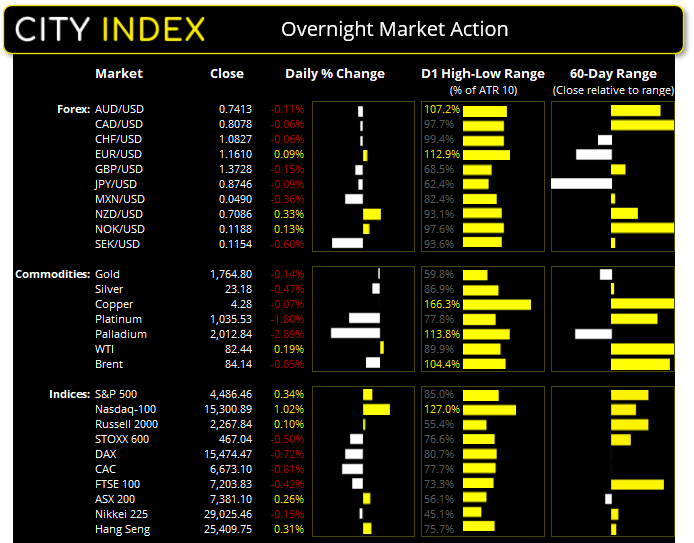

- UK's FTSE 100 index fell -30.2 points (-0.42%) to close at 7,203.83

- Europe's Euro STOXX 50 index fell -31.51 points (-0.75%) to close at 4,151.40

- Germany's DAX index fell -112.89 points (-0.72%) to close at 15,474.47

- France's CAC 40 index fell -54.42 points (-0.81%) to close at 6,673.10

Monday US Close:

- The Dow Jones Industrial fell -36.15 points (-0.1%) to close at 35,258.61

- The S&P 500 index rose 15.09 points (0.34%) to close at 4,486.46

- The Nasdaq 100 index rose 153.967 points (1.02%) to close at 15,300.89

Indices: Chip shortages weigh on output

Manufacturing production fell -0.7% in September due to the global shortage of semiconductors. Industrial production fell -1.3% in September its worst month in 5 and rose 4.6% y/y, down from 5.66% which was revised lower from 5.95%. The Dow Jones fell -0.1% by the close, weighed down by Walt Disney (DIS), Amgen (AMGN) and Travelers (TRV).

Tech stocks were the stronger performers with the Nasdaq 100 rising 1% and printing a bullish engulfing candle on the daily chart. This places gap support around 15,064 and the next key level for bulls to conquer is the 15,365 high.

ASX 200 Market Internals:

ASX 200: 7381.1 (0.26%), 18 October 2021

- Materials (1.04%) was the strongest sector and Information Technology (-1.24%) was the weakest

- 6 out of the 11 sectors closed higher

- 4 out of the 11 sectors outperformed the index

- 91 (45.50%) stocks advanced, 102 (51.00%) stocks declined

- 65.5% of stocks closed above their 200-day average

- 49.5% of stocks closed above their 50-day average

- 58% of stocks closed above their 20-day average

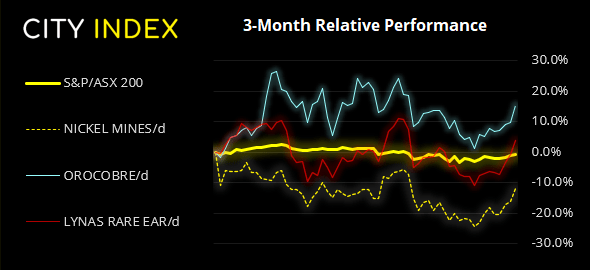

Outperformers:

- + 5.1%-Nickel Mines Ltd(NIC.AX)

- + 4.9%-Orocobre Ltd(ORE.AX)

- + 4.8%-Lynas Rare Earths Ltd(LYC.AX)

Underperformers:

- -4.6%-Kogan.com Ltd(KGN.AX)

- -3.8%-EML Payments Ltd(EML.AX)

- -3.7%-Domino's Pizza Enterprises Ltd(DMP.AX)

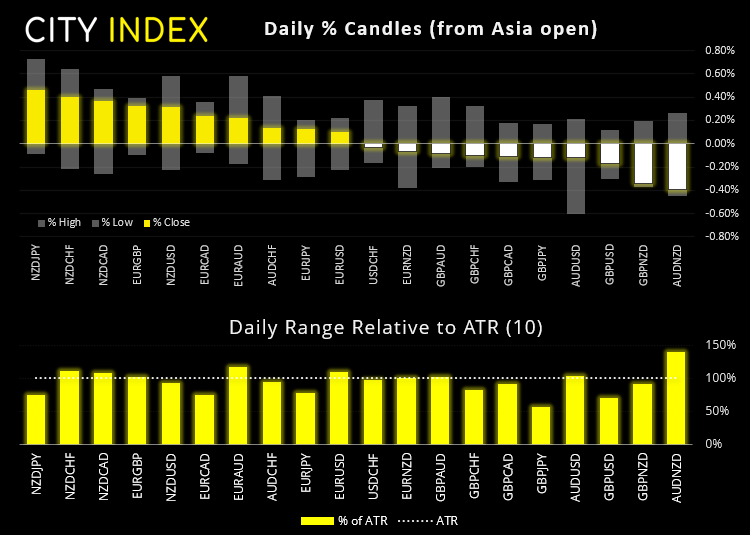

Forex: NZD maintains top spot on the leader board

NZD retained its place at the top of the leader board throughout all three sessions yesterday, after hot inflation all but confirmed another rate hike from RBNZ this year. JPY weakened for a 3rd consecutive session although volatility subsided as momentum waned.

AUD/USD closed the day with a wide legged Doji, after Friday’s bearish pinbar found resistance at the 200-day eMA and monthly R1 pivot. At the very least it suggests a pause in trend is now underway, although some metrics suggest it is time for the Aussie to retrace.

USD/CAD closed slightly higher during another choppy session although prices remain confined within a tight bearish channel on the four-hour chart. Our bias is for a move to 1.2300 once its current consolidation period is complete.

EUR/NZD fell to its lowest level since February, although is on track to close with a wide-legged Doji (volatile indecision candle) which suggests the downside move may need to pause for breath before its trend continues lower.

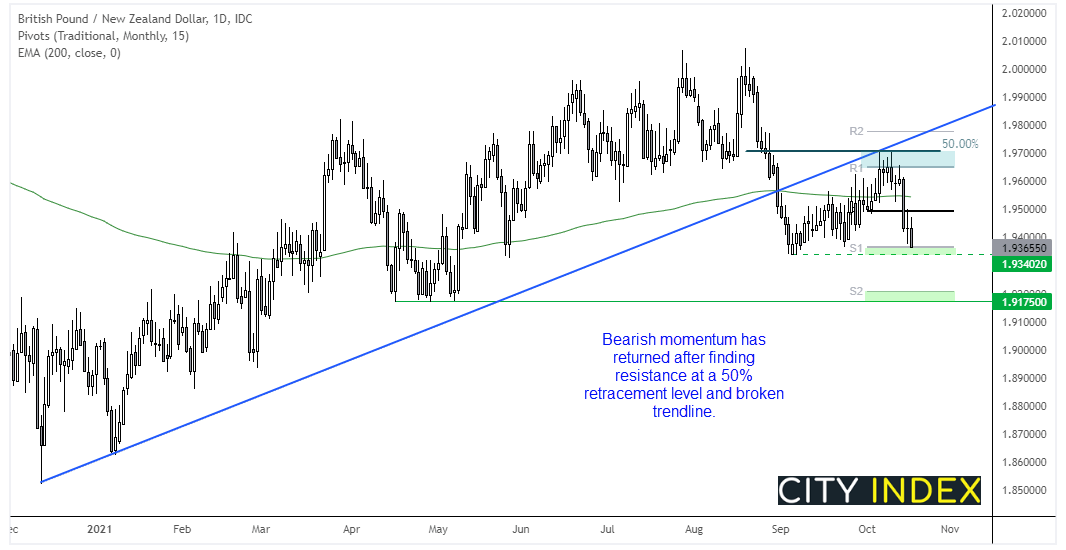

GBP/NZD was on our ‘shortlist’ in September after it broke trend support. Yet its tendency of grinding marginally higher meant it dropped by the wayside. Still, bearish momentum has clearly returned after it seemingly topped out where the 50% retracement level met the broken trendline.

Prices are probing the monthly S1 support level ahead of a potential break beneath the 1.9340 low. A break beneath of which brings the monthly S2 and 1.9175 lows into focus. Hopefully a break lower can materialise without it breaking above the monthly pivot point.

There is very little in the way of economic data today. However, RBA release their monetary policy minutes at 11:30 AEDT, although we doubt it will be a market mover with RBA continuing to be one of the more dovish central banks out there. BOE Governor Andrew Bailer speaks at, then FOMC members Daly, Bowman, Bostic and Waller speak in the early hours between 02:00 and 06:00 tomorrow.

Commodities: Bearish hammer on WTI

WTI printed a bearish hammer on above-average volume, having found resistance at the 83.0 handle. We suspect we could now be headed for a choppy period, although that is not to say it will trigger an outright correction. Therefore, traders may want to drop to lower timeframes and not look for oversized moves without an apparent catalyst driving its direction.

The breakout from the inverted head and shoulders pattern on silver’s daily chart is currently lacking any follow-through. It is holding above the $23 neckline (just) so bulls need to get their skates on to keep this pattern alive. A break beneath $23 invalidates the bias, and a break above Monday’s high is required to keep it alive.

Up Next (Times in AEDT)

How to trade with City Index

You can trade easily trade with City Index by using these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the company you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Today 10:37 AM

Today 08:25 AM

Latest Trade Ideas articles

Today 10:37 AM

Today 08:25 AM