Tapering is far from Tightening

Are equities getting over the Fed’s “taper” announcement? Three weeks ago, Fed Chairman’s shocked the world with his forthright assessment when he indicated that the […]

Are equities getting over the Fed’s “taper” announcement? Three weeks ago, Fed Chairman’s shocked the world with his forthright assessment when he indicated that the […]

Are equities getting over the Fed’s “taper” announcement? Three weeks ago, Fed Chairman’s shocked the world with his forthright assessment when he indicated that the tapering of asset purchases may begin as early this year and could end altogether by June of next year. U.S. and global markets sustained the initial announcement effect by shedding 3-7% on top of losses, which originally began in late May.

Many Fed watchers expect September as the likeliest date for the start of the tapering, considering a continuation in the macro-economic improvement in the US, notably the job market. As long as non-farm payrolls maintain a monthly rise of +120K to 150K, the unemployment rate remains below 7.5% and jobless claims show no rise above 355K-360K, the Fed could finally pull the trigger, provided it has continued to condition the markets for the tapering via its communication channels (FOMC speakers and August Jackson Hole Conference).

Traders must also bear in mind that the tapering of purchases is a mere “cooling” in the pace of easing, rather than tightening. After all, asset purchases remain a form of easing, or money supply expansion, which has swelled up the Fed balance sheet to a record $3.5 trillion. There is a vast gulf of market movements and expectations between easing, neutral and tightening. We remain well in the midst of policy easing.

Not until the Fed begins the tapering of purchases, can we use the term “normalization”. And once we eventually enter such a period, markets may not look so bad. Historically, markets rallied as the Fed transitioned from interest rate cuts to a neutral policy stance. The principal reason a central bank pauses from easing is the stabilization of economic growth. As the data transitions from stability to expansion, the central bank reduces stimulus, allowing economic and business green shoots transform into full bloom. And thus, it is no surprise that the S&P500 rise during periods of neutral monetary policy following interest rate cuts.

Sep ‘92 to Jan ‘94: S&P500 +15%

Nov ‘98 to May ’99: S&P500 +16%

June ‘03 to May ‘04: S&P500 +18%

If the Fed makes the transition into reducing monetary stimulus, then it implies that any economic stabilization is sufficiently robust to handle the policy shift. That would be especially the case if the Bank of Japan, Bank of England and European Central Bank maintain their easing policy directive.

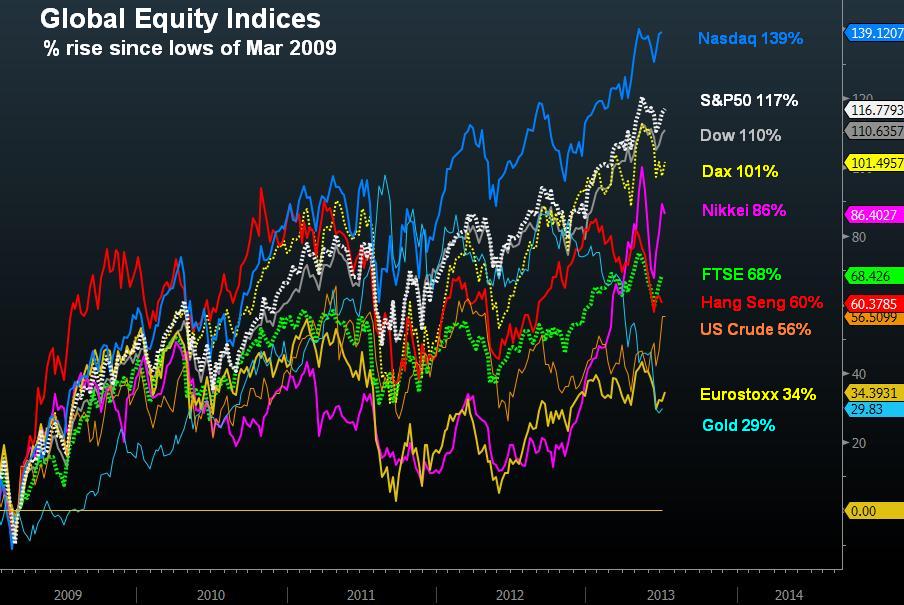

And as US equities show their usual ascent during policy normalization, then global equities could well follow suit due to their habitual convergence with US indices and easier policies in their own central banks. Looking at the chart above, the Dax-30, Nikkei-225 and the FTSE-100 are up 101%, 86% and 68% above their generational lows from March 2009. The FTSE is likely to continue finding support above its 2-year trendline support of 6,050, before making a fresh attempt towards 6,620 towards year-end.