Supermarket shares near front of inflation queue

For UK food prices, it’s turning out to be feast or famine.

For UK food prices, it’s turning out to be feast or famine.

For just over two years, real food price deflation sapped the strength of high street grocers adding to pressures from changing consumer habits and a price war triggered by Aldi and Lidl.

Then came the Brexit vote. By last December, the rare phenomenon of British food prices falling below historical norms— the ONS said this last occurred in the ‘60s—was virtually over.

It definitely is now. The plunge in the pound has the forced the cost of staples like butter, fish, tea and skincare higher by levels which shoppers are beginning to notice. The latest grocery price survey by researcher Kantar Worldpanel shows prices up 2.3% on the year in 12 weeks to 26th March.

There’s no mistaking the trend: prices were up just 1.4% in Kantar’s Christmas-February data.

The speed at which prices hardened and subsequently accelerated underlines that whilst all consumer-facing industries are bracing for a new era of inflation, challenges will be particularly acute for supermarkets.

Their direct link to trends around consumption of necessities suggests their shares will react faster to any sign of economic tightening. The first pinch isn’t being felt by grocers themselves though.

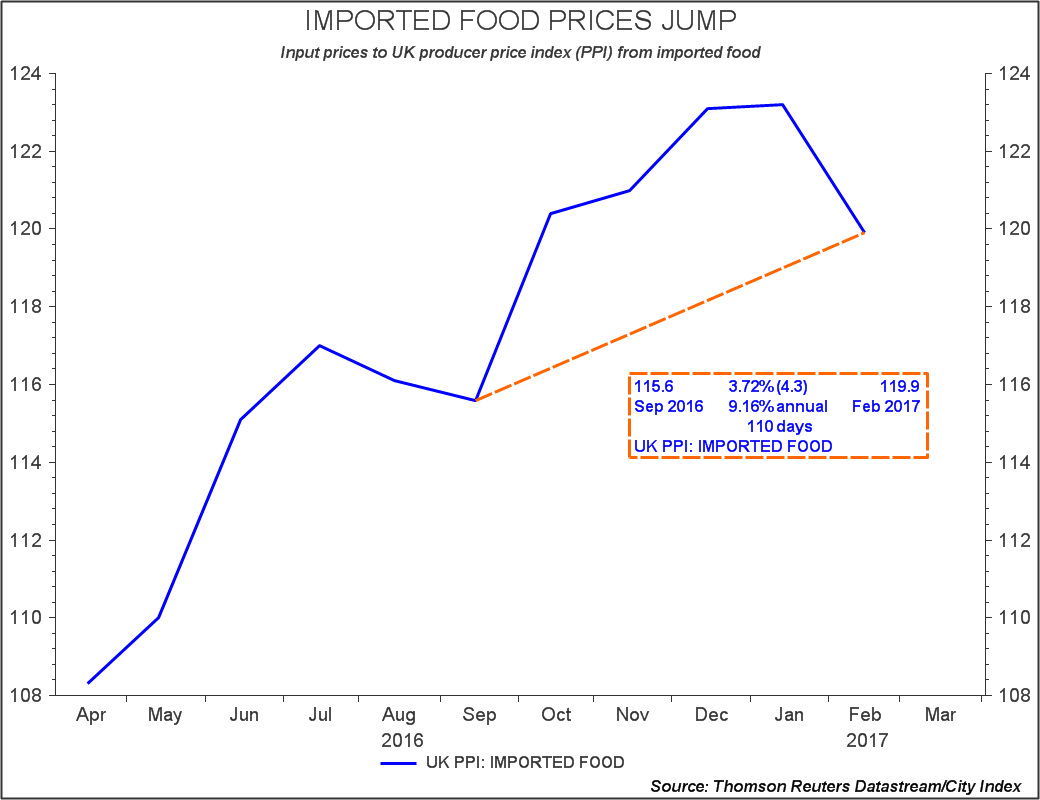

Despite easing off at the start of the year, prices paid by food producers (input prices) are still more than 9% higher than they were in September, presenting a steep hike in costs.

Rising suppliers’ costs are the first inflationary pressures in the chain. The question is when and to what extent such hikes will or can be passed on to grocers, and in turn to shoppers.

Anecdotal evidence continues to point to the bargaining power of the biggest British retailers—supermarket operators—largely winning out, keeping checkout price rises relatively contained, for now.

However this week’s data shows long-term agreements and selective price rises have not masked an increase in prices overall. And pain (or at least frustration) is already beginning to show among large suppliers (e.g. Unilever—see ‘Marmitegate’) and small ones (e.g. Premier Foods).

It’s only a matter of time before supermarkets, most of which only recently since saw a mild recovery in underlying sales, are once again between a rock and a hard place.