SuperGroup is UK retail fashion victim of the year

SuperGroup’s snazzy ‘street-wear’ for twenty-somethings hasn’t flown off the shelves fast enough recently and its first-half profits tumbled 30%. It said summer ranges received a […]

SuperGroup’s snazzy ‘street-wear’ for twenty-somethings hasn’t flown off the shelves fast enough recently and its first-half profits tumbled 30%. It said summer ranges received a […]

SuperGroup’s snazzy ‘street-wear’ for twenty-somethings hasn’t flown off the shelves fast enough recently and its first-half profits tumbled 30%.

It said summer ranges received a mixed reaction from shoppers, whilst disappointingly, SuperGroup is reiterating that the warm autumn hurt sales of winter items.

Underlying pre-tax profit in the six months to 25th October was £12.5m, a significant collapse from the first half a year ago, when the firm made £17.9m.

Revenues are an encouraging point with an 8.4% rise, though sales at stores open for more than a year fell 4.1%.

What may have saved the shares from the 9.5% drop they saw at the market’s open is the fact the firm is sticking to an outlook for full-year profit to be between £60m and £65m.

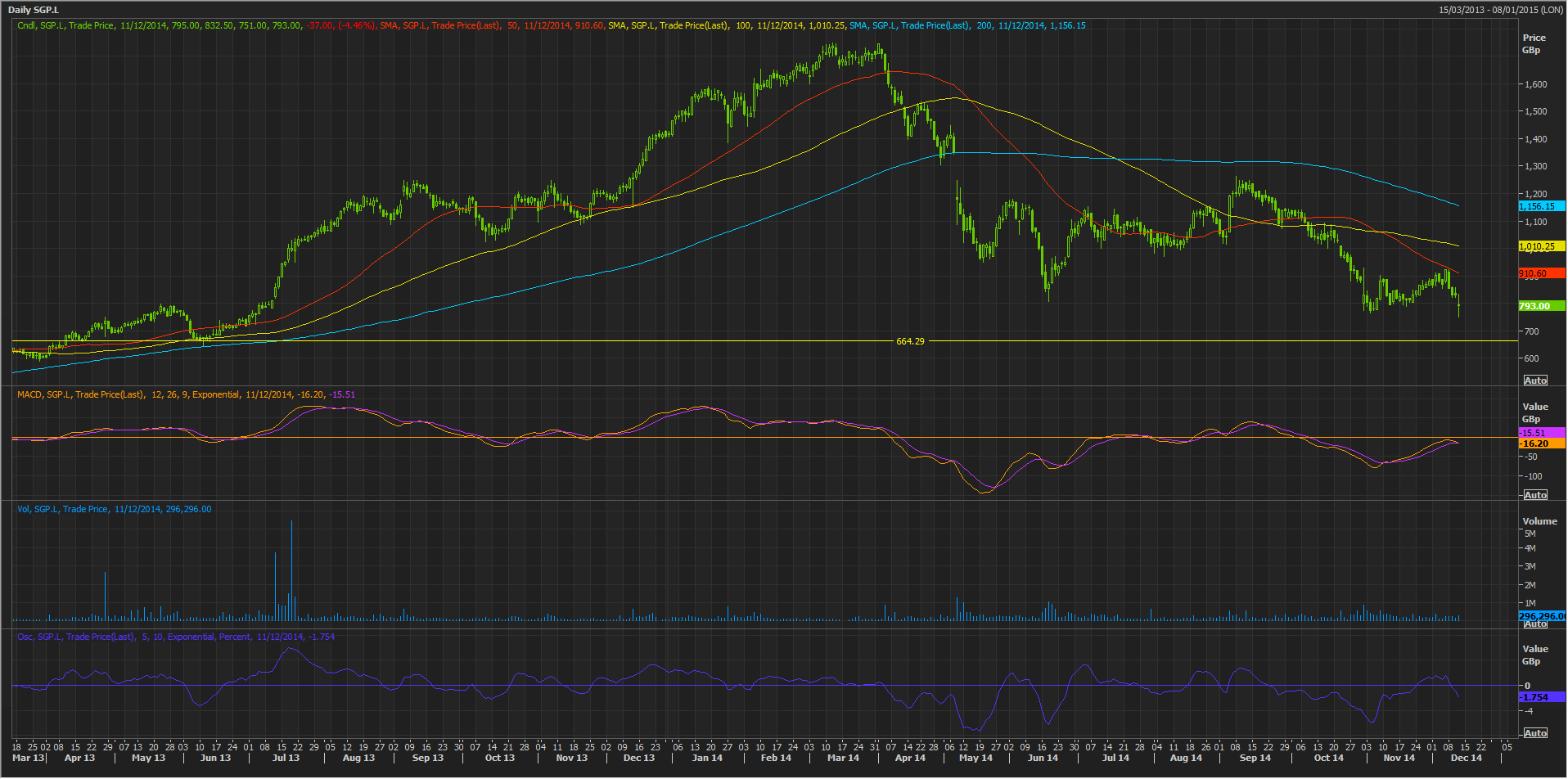

The shares are still more than 50% lower since hitting a three-year high of 1746p in March though, and all things considered, any material near-term recouping would not be justified by current fundamentals in my view.

Unfortunately, blaming a fall in demand for winter clothing (one of SuperGroups’s biggest categories is winter jackets) on the unseasonably warm weather, is playing less and less well with the investment community, and we note firms like Next Plc. and Marks & Spencer have latterly shied away from attributing their sagging clothing sales to the British autumn.

The fact that SuperGroup hasn’t followed suit puts it at risk of increased negative attention within the sector by default.

But perhaps more darkly, SuperGroup has revised its full-year margin guidance from a rise of 25 basis points, to now an expectation of no margin gains.

SuperGroup explains this by saying it will be clearing over-stocked items left over from the first half.

For me, this spotlights SuperGroup’s fashion supply chain and space management systems as having an even greater need of the kind of modernisation programs that its peers like Inditex, Hennes & Mauritz, M&S, Hugo Boss and others have embarked on.

This basically means they now aim to buy goods more often and closer to home, rather than relying on seasonal collections sourced months in advance.

Chains adopting this approach tend to deal directly with factories to cut down delivery times and ensure a steady supply of new garments.

There is a cost for the relatively smaller-scale retailers that can’t offer manufacturers the huge volumes of their global competitors.

This can be a further factor putting operators like SuperGroup at a disadvantage, as newer supply chain methodologies gain traction, something that seems to us as pretty much inevitable.

Add in the admission I mentioned above, that margins would soften, and the inevitable conclusion is that there should be no material comeback as yet, by the shares from current 17-month lows.

In fact, support might arguably, be stronger closer to 660p.

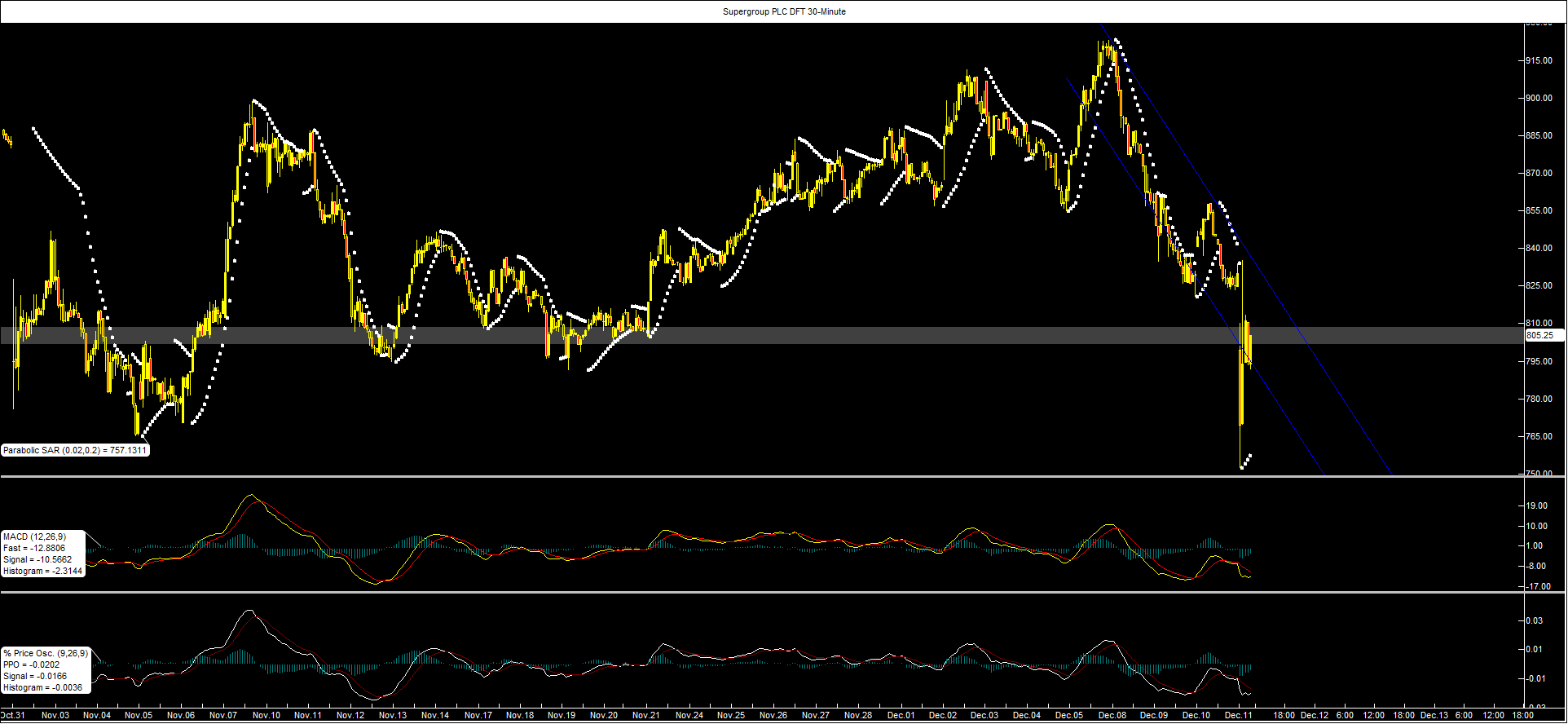

City Index’s SuperGroup Daily Funded Trade seems to be reflecting current vulnerabilities in the shares well.

Clients seem well aware that re-basing the title at levels closer to the equivalent of 660p support would require a confirmed breach of the current channel.

So long as momentum is not overstretched, renewed tests lower are likely.