Stocks are pointing to a mixed start as investors weigh up moves by President Trump taking aim at Chinese tech, impressive Chinese and German trade data and with nerves showing ahead of the non-farm payroll report after a week is disappointing labour market data.

Trump’s executive order giving US firm 45 day to stop dealings with ByDance’s TikTok and Tencent’s WeChat is the latest move by the White House in an increasingly broad campaign against China dragging on sentiment

Earlier on Thursday Trump also advised that Chinese firms listed on US stock exchanges delisted unless they can provide US regulators with access to their accounts.

These moves are unlikely to be taken lying down by China and could potentially see China blocking US big Tech such as Apple or Microsoft. Whilst tech was always an undercurrent in the US - Sino trade war, this latest move points to the potential start of a more explicit tech war?

Timing is everything and doesn’t bode well for the next US – Chinese meeting over progress in the Phase one trade deal next week.

Chinese exports surge

The attacks by Trump and flaring up of US – Sino tensions have overshadowed the surge in Chinese exports. Trade data from China showed that exports soared 7.2% compared to a year earlier. This is significantly ahead of 0.2% increase forecast and points to the Chinese economic recovery gaining momentum.

The attacks by Trump and flaring up of US – Sino tensions have overshadowed the surge in Chinese exports. Trade data from China showed that exports soared 7.2% compared to a year earlier. This is significantly ahead of 0.2% increase forecast and points to the Chinese economic recovery gaining momentum.

German exports jump 14.9%

Upbeat data from Germany is going someway to off set the Trump inspired downbeat mood. German exports rose in June for a second straight month and rose by a convincing 14.9% in June, whilst imports increased 7%. The data adds to mounting evidence that the economic recovery in Germany is on a solid footing and comes following factory orders data yesterday which smashed expectations.

Upbeat data from Germany is going someway to off set the Trump inspired downbeat mood. German exports rose in June for a second straight month and rose by a convincing 14.9% in June, whilst imports increased 7%. The data adds to mounting evidence that the economic recovery in Germany is on a solid footing and comes following factory orders data yesterday which smashed expectations.

Still no US rescue package in sight

Developments on Capitol Hill will be in focus as the Democrats and Republicans have so far failed to agree on a new stimulus package for America to support it through the coronavirus crisis. The two sides remain far apart on what size the package should be. The summer recess is due to start today.

Developments on Capitol Hill will be in focus as the Democrats and Republicans have so far failed to agree on a new stimulus package for America to support it through the coronavirus crisis. The two sides remain far apart on what size the package should be. The summer recess is due to start today.

US NFP in focus

Attention will now turn towards US non-farm payroll data. Expectations are for 1.5 million new jobs to have been created in the US in July. This is down significantly from last month’s 4.8 million. Lead indicators this week from the ADP Payroll report and the employment subcomponent of the ISM non manufacturing report have been disappointing and point to the recovery in the labour market stalling, hampered by a resurgence in coronavirus cases since mid-June.

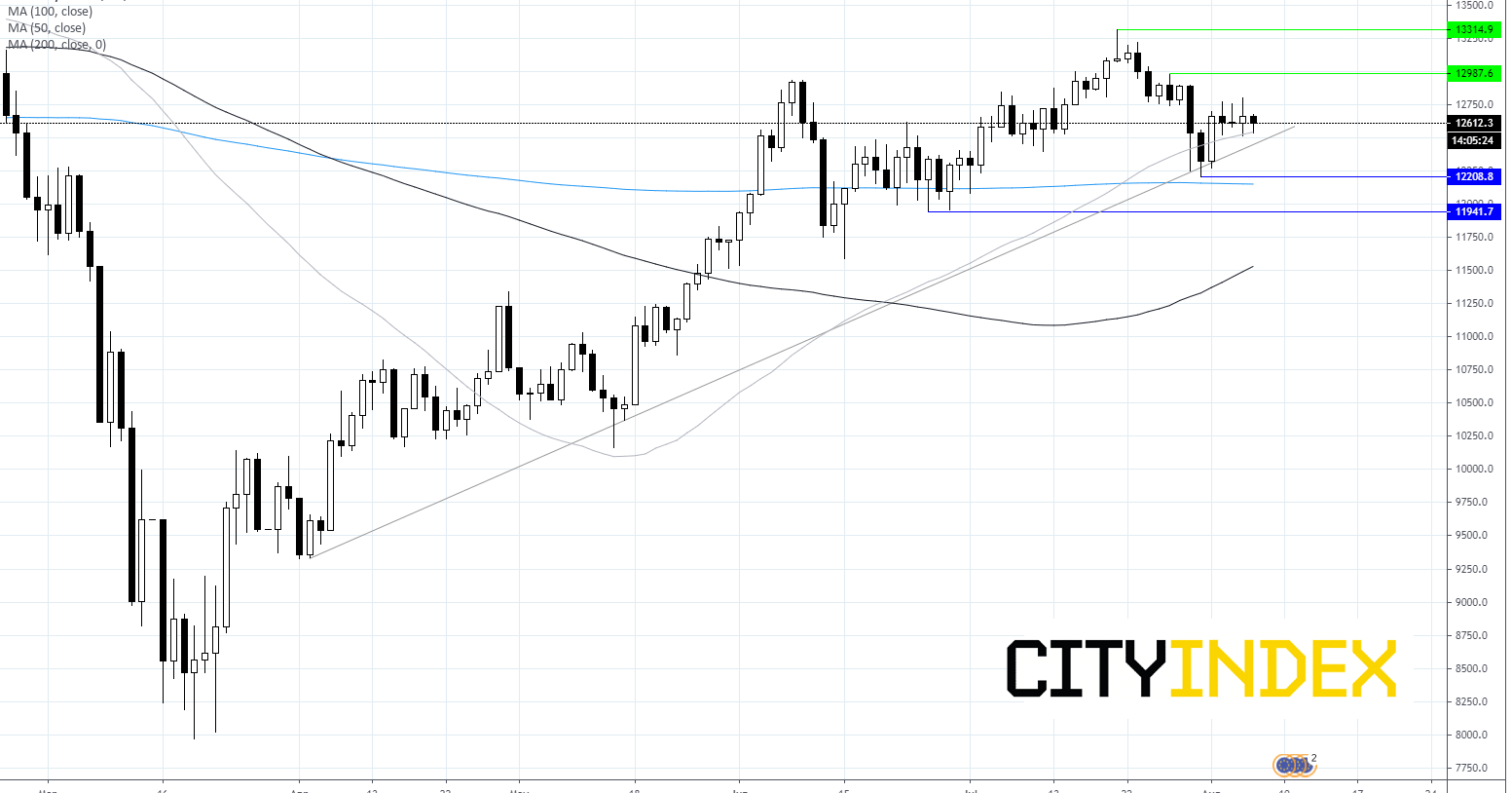

Dax chart

Latest market news

Today 07:55 AM

Today 04:47 AM

Yesterday 11:23 PM

Yesterday 10:19 PM

Latest Dax articles

Today 07:55 AM

Today 04:47 AM

Yesterday 04:54 PM