Whilst Wall Street traded broadly lower on Monday with both the S&P and the Dow Jones closing in negative territory, the Nasdaq finished higher. This was by no means indicative of the month. In fact August was the best month for US stocks in over 15 years thanks to a shift in Fed policy framework and continued reassurance from the Fed that interest rates will remain lower for longer

Whilst Wall Street traded broadly lower on Monday with both the S&P and the Dow Jones closing in negative territory, the Nasdaq finished higher. This was by no means indicative of the month. In fact August was the best month for US stocks in over 15 years thanks to a shift in Fed policy framework and continued reassurance from the Fed that interest rates will remain lower for longer

Overnight, Asian markets booked gains and Europe is pointing to a stronger start after Chinese data showed that the vast manufacturing sector continued to recover after the coronavirus pandemic.

China manufacturing sector expands at fastest clip in 11 years

The Caixin Chinese manufacturing PMI rose to 53.1 in August, up from 52.8 in July in the fourth straight month of growth. Expectations had been for a slight dip to 52.6. The data revealed that activity in the sector expanded at the fastest pace in almost a decade as new export orders rise for the first time this year. This indicates that after a period of drought caused by the coronavirus lockdown, foreign demand is starting to pick up as economies across the globe reawaken from their lockdown slumber. The employment gauge in the report showed that some companies were starting to increase recruitment to meet production needs, although the gauge remains in negative territory.

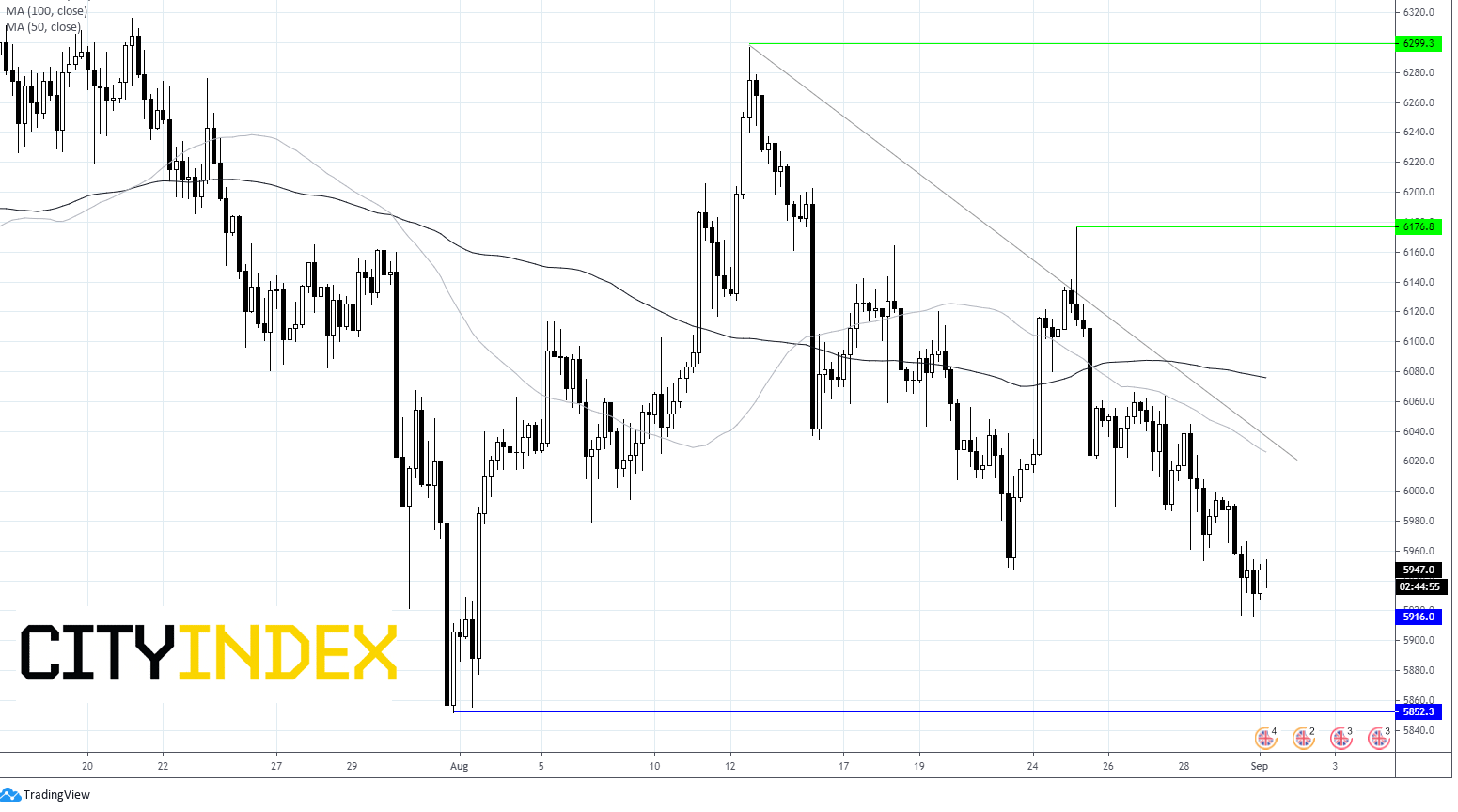

UK miners could see a lift on the back of the upbeat Chinese data, which has boosted metal prices overnight.

The Caixin Chinese manufacturing PMI rose to 53.1 in August, up from 52.8 in July in the fourth straight month of growth. Expectations had been for a slight dip to 52.6. The data revealed that activity in the sector expanded at the fastest pace in almost a decade as new export orders rise for the first time this year. This indicates that after a period of drought caused by the coronavirus lockdown, foreign demand is starting to pick up as economies across the globe reawaken from their lockdown slumber. The employment gauge in the report showed that some companies were starting to increase recruitment to meet production needs, although the gauge remains in negative territory.

UK miners could see a lift on the back of the upbeat Chinese data, which has boosted metal prices overnight.

Manufacturing PMI’s to show continued recovery (except Germany)

Manufacturing PMI’s for UK, Europe and US are due to be released. Manufacturing sectors across the board have broadly performed better than service sectors through and after lockdown, simply because they were not as affected. The UK’s manufacturing sector is expected to remain steady in expansionary territory at 55.3. The Eurozone is also expected to confirm 51.7. However, weakness is expected from Germany which could see the initial reading downwardly revised to just 50 down from 53.

This week is a busy week for US data, culminating in the non-farm payroll on Friday. Prior to that US ISM manufacturing is expected to continue reflecting moderate growth. Even so this is not expected to be sufficient to halt the US Dollar’s decline. Whilst the PMI is expected be 54.5, weakness in employment could add further pressure to the greenback.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest FTSE 100 articles

March 11, 2024 04:30 PM

March 5, 2024 12:00 PM

February 12, 2024 10:30 AM

January 15, 2024 12:30 PM