Stocks US indices at key levels ahead of Q2 earnings season

The US stock markets have opened lower today, tracking the sharp losses overnight in Asia Pacific. Investor sentiment has been hurt by a number of […]

The US stock markets have opened lower today, tracking the sharp losses overnight in Asia Pacific. Investor sentiment has been hurt by a number of […]

The US stock markets have opened lower today, tracking the sharp losses overnight in Asia Pacific. Investor sentiment has been hurt by a number of factors. These include the commodity market sell-off, the Chinese stock market rout and the renewed strength in the dollar, which is obviously not good for US exports and company earnings. And let’s not forget Greece, of course!

The latest news from Athens is that the Greek government will submit “credible reform” proposals to its international creditors on Thursday, according to PM Alexis Tsipras. The bank holidays have been extended to at least until Thursday and the €60 daily limit on ATM withdrawals is kept in place. Overnight in China, the Shanghai Composite managed to claw back some of its earlier losses but it still closed down almost 6% despite the introduction of several measures aimed at halting the rout. Oil and metal prices are more stable following their recent sell-off, but remain vulnerable as worries about the health of the Chinese economy grow.

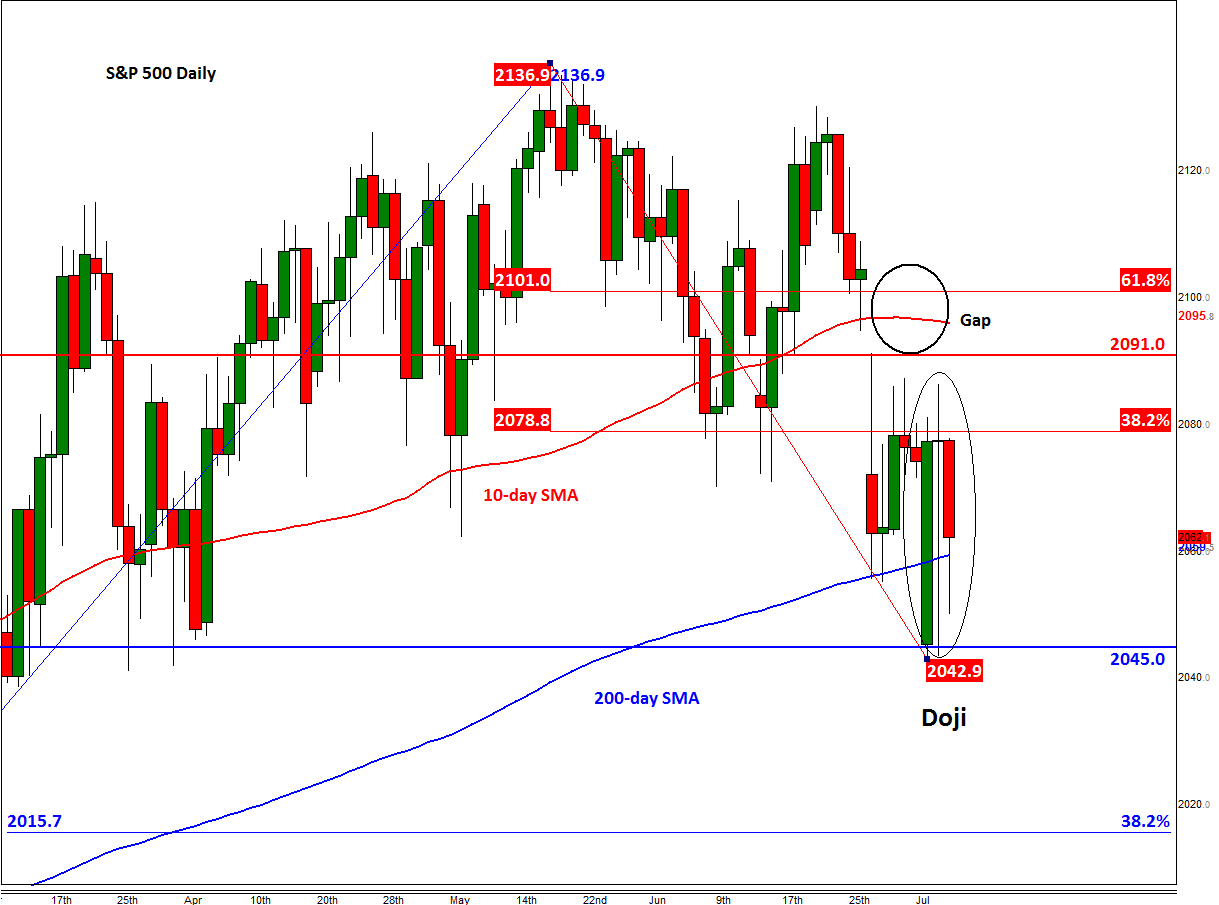

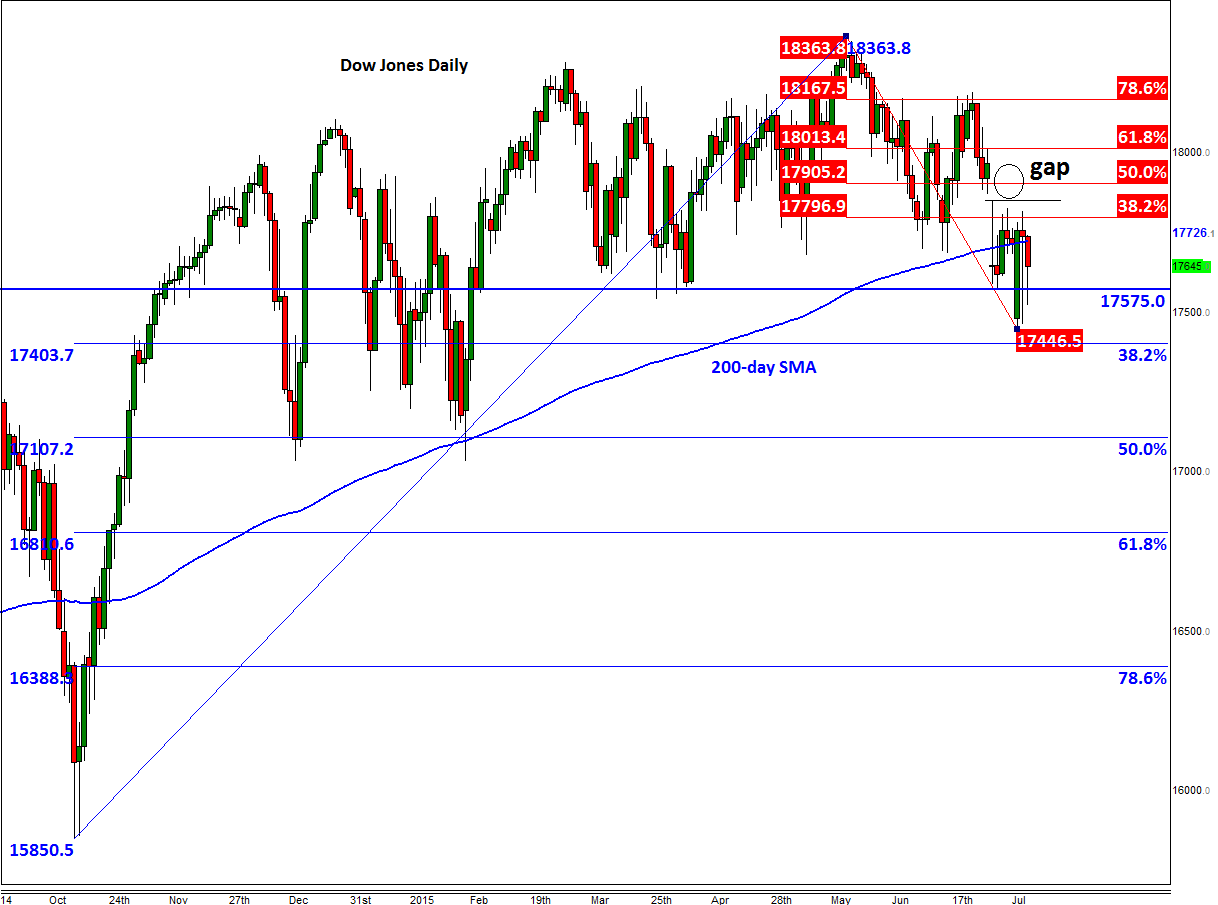

The Dow and the S&P 500 have now pulled back around 4% each from the record levels in May, so the sell-off on Wall Street has been nowhere as pronounced as China. Not yet anyway. Here, investors are probably waiting to see the results of some company earnings before deciding on what to do with their long equity holdings. The second quarter earnings season will unofficially kick off as aluminium giant Alcoa reports its numbers after the closing bell tonight. Ahead of that we will have the minutes from the Federal Reserve’s June policy meeting at 14:00 ET. Not a long time ago, the Fed was expected to start raising interest rates in June. Then expectations were pushed out slightly for a September hike and then to December. But now the calls are growing to hold off until early 2016, most prominently from the IMF. We may have a better idea in terms of the timing for the lift off once the minutes are released today. Any further delay in raising interest rates should be good news for stocks and bad for the dollar.

As well as China’s Shanghai Composite and Germany’s DAX, some of the key US indices such as the Dow and the S&P 500 are also testing their respective 200-day moving averages. This particular moving average is closely-watched and it is thought that some money managers and hedge funds have specific rules that prevent them from buying markets which are trading below these averages. Thus, should the indices break decisively below their 200-day averages, we could see further withdrawal of long positions form this group of market participants which could exacerbate the sell-off. But if the 200-day average supports hold firm, a potential rally could be on the way, particularly as there are also a few market gaps that have yet to be “filled.” The S&P created a long-legged doji candle on its daily chart on Tuesday which points to indecision. Tuesday’s ranges should therefore be watched closely as a break could lead to a sharp move in that direction.