Stocks surge but are we climbing a wall of worry

The stock market volatility has been a dominant theme this week. After that vicious sell-off on Monday, the markets have bounced back strongly thanks in […]

The stock market volatility has been a dominant theme this week. After that vicious sell-off on Monday, the markets have bounced back strongly thanks in […]

The stock market volatility has been a dominant theme this week. After that vicious sell-off on Monday, the markets have bounced back strongly thanks in part to the PBOC’s decision to further loosen monetary policy. Concerns over the health of the US economy have also eased somewhat following the release of mostly better than expected data this week. The latest readings on consumer confidence, durable goods orders and now GDP have all topped expectations. But housing market data has disappointed, with sales of new and pending homes missing the mark. Also helping the stock market rally has been the sharp rebound in oil prices, which has helped to underpin energy stocks today. While further short-term gains could be seen, I remain sceptical about this latest rally and question its sustainability. After all, it is not unusual to see wild swings in the markets when major trends change course. Growth concerns about China are still there and the Fed may still increase interest rates later this year. There will also be plenty of buyers who may still hold large losing positions. This group of market participants may choose to exit their positions when they have the opportunity to do so. Thus, the sellers could return once the dust settles, possibly as early as Friday or the start of next week.

DAX: is the German index rallying into a resistance area?

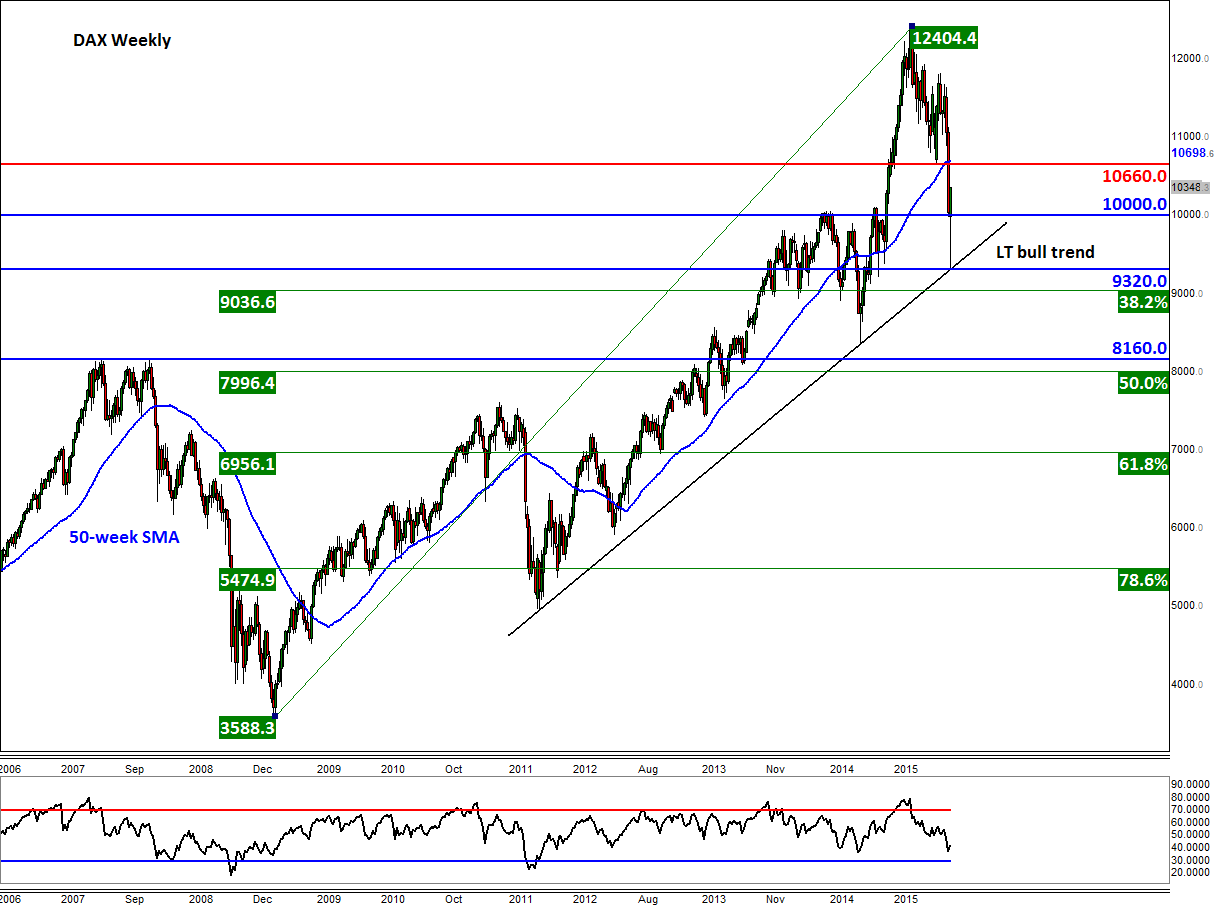

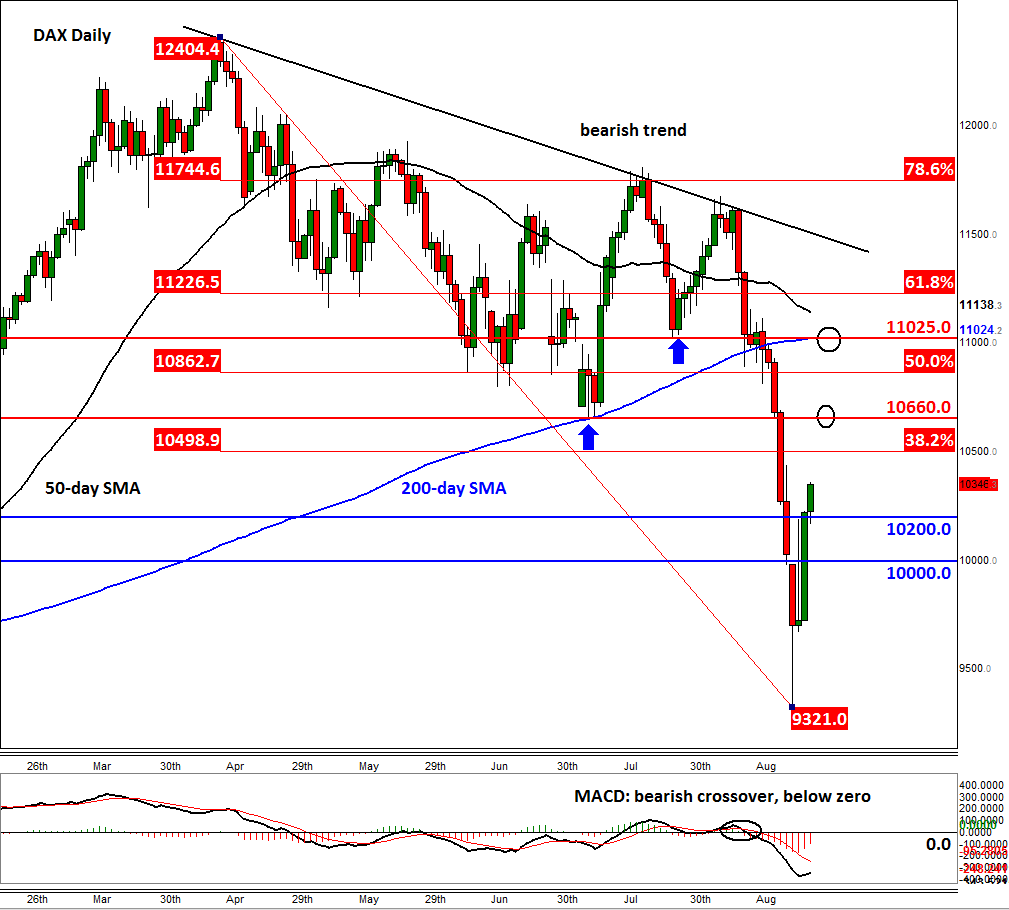

As we highlighted the possibility on Monday, the German DAX index dropped all the way to its long-term bullish trend line around 9320 later that day. This trend line has obviously held as support, causing the index to bounce back very strongly. So far this week, it has gained a cool 1,000 points from there – not a bad return! But more gains could now be on the way, at least in the short term anyway. As can be seen from the updated charts, below, there is not much overhead resistance now until 10660, a level which corresponds with the July low. If that level breaks then the rally may continue until the next resistance at 11025 which also corresponds with the 200-day moving average. Traders should also keep a close eye on the Fibonacci retracement levels of the sell-off from the all-time peak of 12405. The 38.2% retracement level is at just below 10500 while the more significant 50 and 61.8 per cent retracement levels are at 10860 and 11225, respectively.

Given the recent turmoil and the growing investor pessimism, it could be that the markets may have already formed a top. It is not unusual for the markets to stage these sorts of moves when a top is formed. So, we remain sceptical about this rally and recommend that traders should proceed with an open mind and avoid making any strong conclusions based on what they might have seen over the past few sessions. It is likely that once this kick-back rally euphoria fades that the sellers may return and re-establish their positions at better levels. When and where, that is anyone’s guess. But conservative speculators may want to wait until a clear reversal pattern is formed, ideally around a key resistance level – such as those we identified above – before making a trade.