There is a lot to like as the European session gets underway, Fed & Trump stimulus, Brexit optimism, UK unemployment remaining at multi decade lows and an expected record breaking rebound in US retail sales. Needless today the positives are outweighing second wave fears sending stocks sharply higher.

The formal start of the Fed’s corporate bond buying programme boosted global sentiment. The Fed announced that it will start purchasing corporate bonds today. This is one of several emergency facilities launched amid the coronavirus pandemic.

Trump’s stimulus talk

Adding to the seemingly addictive stimulus high, the Trump administration is weighing up a $1 trillion infrastructure spend to spur on the economy in the wake of the coronavirus crisis. The plan is expected to include more traditional infrastructure work, such as roads and bridges, but is also expected to set aside money for wireless 5G and rural broadbands.

There is nothing like a fresh round of stimulus to boost risk sentiment in the markets. Fears of a second wave have been calmed by the fact that the Fed has your back and that Trump is prepared to increase spending significantly to inject life back into the economy.

Adding to the seemingly addictive stimulus high, the Trump administration is weighing up a $1 trillion infrastructure spend to spur on the economy in the wake of the coronavirus crisis. The plan is expected to include more traditional infrastructure work, such as roads and bridges, but is also expected to set aside money for wireless 5G and rural broadbands.

There is nothing like a fresh round of stimulus to boost risk sentiment in the markets. Fears of a second wave have been calmed by the fact that the Fed has your back and that Trump is prepared to increase spending significantly to inject life back into the economy.

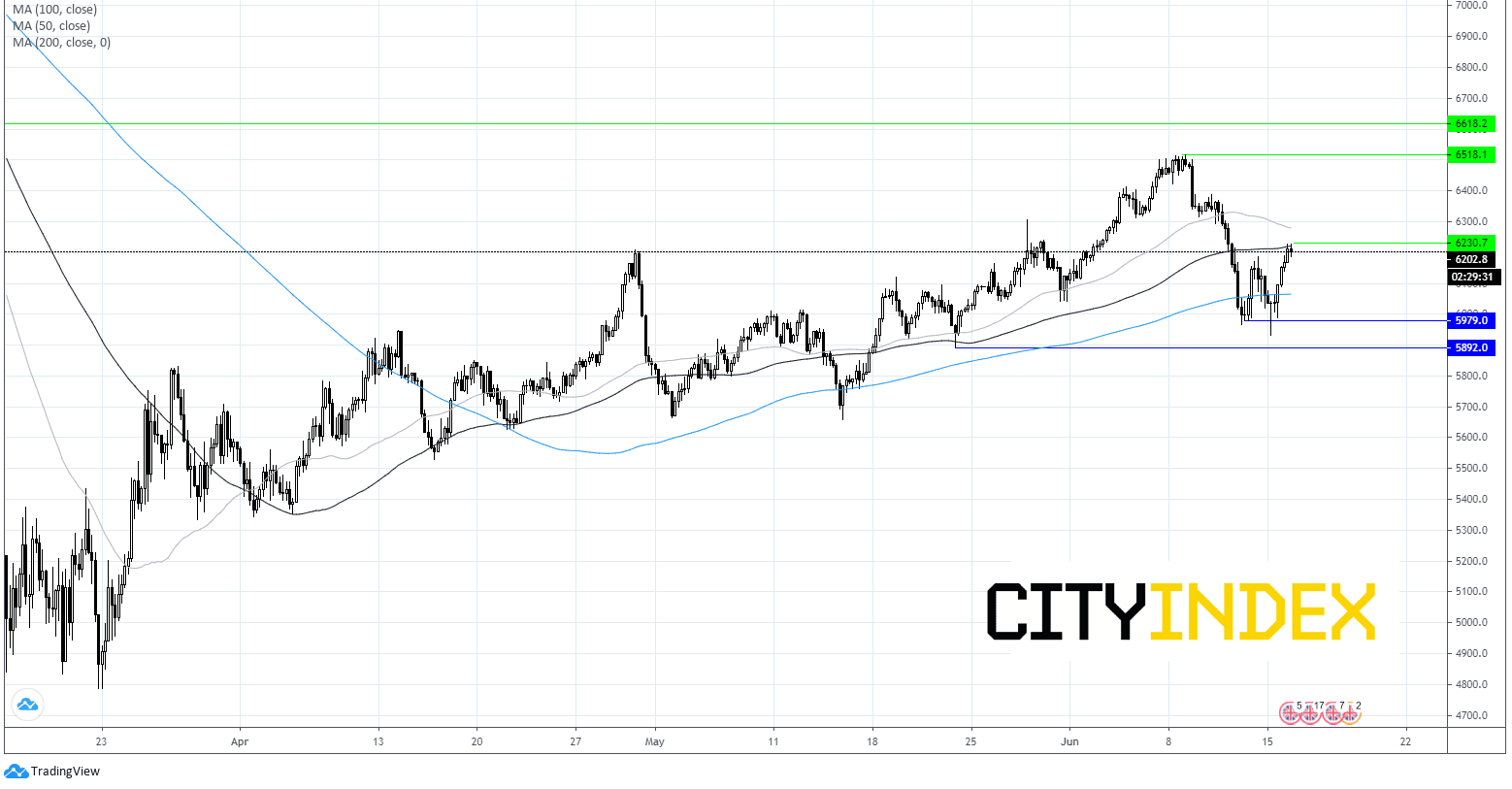

Asian stocks rallied overnight, European futures are pointing to a sharply stronger open, erasing losses from the previous session. Meanwhile safe havens such as the US Dollar is trading firmly on the back foot, whilst traditional gold is extending losses from the previous session. Oil is holding onto 4% gains from Monday’s rebound.

Brexit optimism

Good news isn’t just confined to the US. Political momentum appears to have been injected into Brexit negotiations following high level talks between Boris Johnson and EU presidents. Boris saying that he sees no reason why a deal can’t be reached in July has boosted optimism that a deal is coming. The renewed optimism in both London and Brussels comes after recent talks stalled.

Good news isn’t just confined to the US. Political momentum appears to have been injected into Brexit negotiations following high level talks between Boris Johnson and EU presidents. Boris saying that he sees no reason why a deal can’t be reached in July has boosted optimism that a deal is coming. The renewed optimism in both London and Brussels comes after recent talks stalled.

UK unemployment beats, claimant count soars

The Pound barely acknowledged a mixed bag of labour market data, holding onto gains achieved overnight versus both the US Dollar and the Euro. The UK unemployment rate remained at multi decade lows of 3.9%, defying expectations of an increase to 4.7%. However, evidence of the covid-19 impact to the labour market was revealed through a sharp increase in the claimant count, which jumped by 528,900 well 50% higher than the 370,000 forecast.

The Pound barely acknowledged a mixed bag of labour market data, holding onto gains achieved overnight versus both the US Dollar and the Euro. The UK unemployment rate remained at multi decade lows of 3.9%, defying expectations of an increase to 4.7%. However, evidence of the covid-19 impact to the labour market was revealed through a sharp increase in the claimant count, which jumped by 528,900 well 50% higher than the 370,000 forecast.

Whilst the government’s furlough scheme offers an unprecedented amount of support to the UK labour market, we can expect to see this start to unravel in the coming months as the scheme is gradually withdrawn.

US retail sales to rebound

Looking ahead the focus will shift to US retail. US retail sales are expected to post a record jump in May as states across the US started to reopen and 2.5 million Americans returned to work. An increase of 8% in sales is expected, however, this will only represent about a quarter of the historic drops experienced in March and April.

Even so hints of a turnaround and signs of the green shoots of recovery could see risk sentiment bound higher, lifting stocks whilst weighing on the safe haven US Dollar.

Latest market news

Yesterday 01:23 PM

Yesterday 06:01 AM

April 18, 2024 11:27 PM

April 18, 2024 04:46 PM

Latest Coronavirus articles

January 5, 2023 08:14 PM

December 6, 2022 05:03 PM

September 1, 2022 04:28 PM

August 1, 2022 08:40 AM