Stocks surge as disappointing US data reduces rate hike probability

This week’s disappointing jobs report and manufacturing data from the US, the world’s largest economy, has dampened expectations for a rate rise in 2016, though […]

This week’s disappointing jobs report and manufacturing data from the US, the world’s largest economy, has dampened expectations for a rate rise in 2016, though […]

This week’s disappointing jobs report and manufacturing data from the US, the world’s largest economy, has dampened expectations for a rate rise in 2016, though it has not been entirely eliminated from the equation. Unfortunately it just means that uncertainty about the next rate rise will remain in place for far longer than one would have liked. For traders though, that is a worry for another day. Clearly, some have used this as an opportunity to reload their short dollar positions that they were forced to close on the back of Fed’s optimism at the Jackson Hole symposium. So far it has also been good news for some buck-denominated commodities like gold, silver and oil, but more so for stocks. Indeed, the UK’s FTSE 100 has been a star performer in Europe today, up nearly 2%, due to the sheer number of commodity stocks that it contains. But in the US, the reaction has been a little muted, though the indices here have also extended their gains from Thursday.

Look ahead to next week

Looking forward to next week, the Labor Day holiday means the US and Canadian markets will be closed on Monday and no data will be published from North America then. But a speech by the Bank of Japan Governor Haruhiko Kuroda and the UK services PMI should give traders outside North America plenty to think about. The economic recovery in the UK post the Brexit vote has caught many people by surprise and a strong PMI reading for the largest sector of the economy will no doubt further boost investors’ confidence about UK assets. On Tuesday, the Reserve Bank of Australia will decide whether to cut rates further or stay on hold at 1.50% as it has previously indicated. If there are any dovish comments on the policy statement then this should provide some support for the Australian stock markets. But the key data on Tuesday will be form the US, the ISM services PMI. After we saw a very disappointing manufacturing PMI, this particular PMI should have more of an impact on the dollar and stocks as the US is a services-led economy – as long as it shows a significant deviation from the expected reading. Also relevant for the stock markets will be the latest trade figures from China, due out on Thursday. Concerns over the world’s second largest economy have faded in recent months amid the slight improvement in data there. If confirmed by the latest import and export figures, this should help to boost the appetite for risk further. Perhaps a key event for European markets in particular will be the European Central Bank rate decision on Thursday, although the central bank is widely expected to remain on hold at this meeting. Nevertheless, comments from the ECB President Mario Draghi at the press conference on the future path of monetary policy could lead to volatile moves in the FX and stock markets.

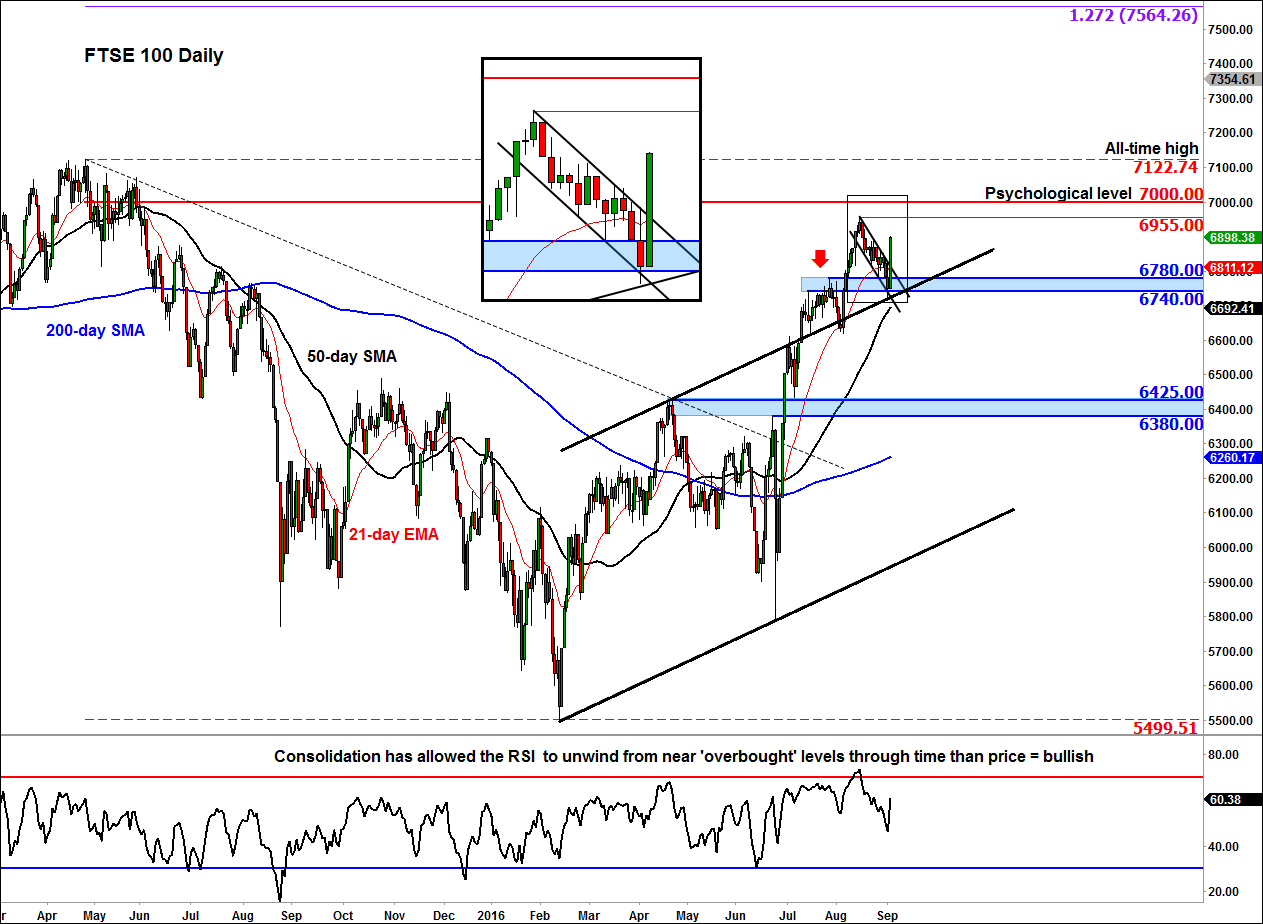

Technical outlook: FTSE ends corrective trend

After edging lower for nearly three weeks, the FTSE surged higher on Friday. The consolidation from around mid-August had allowed the RSI momentum indicator to unwind from ‘overbought’ levels of 70 mainly through time rather than price action. Now that the index appears to have ended its consolidation phase, and with the RSI being away from its extreme levels, we could see some further momentum buying pressure in early next week. Some of the bullish objectives to watch include 6955, the high from August, followed by the psychological level of 7000 and then the previous all-time high at 7122. So, the path of least resistance is to the upside. As things stand, only a break below the key 6740-6780 support range would invalidate our bullish technical view.