Fed adds fresh rates uncertainty to edgy markets ahead of summit

Global shares have broken out of a week-long holding pattern as nerves ahead of the G20 summit are exacerbated by reassessed chances of a rate cut. There are now hints that policymakers may be walking back prospects of near-term easing after chair Jerome Powell gave no indications of timing in a speech on Tuesday. This compounds an increasingly sober mood as the on 28th and 29th June summit looms. With a decision on whether Washington will slap another $300bn in tariffs on Chinese goods at stake, the event could make or break the stock market’s comeback from end-May lows.

With the S&P 500’s volatility indicator, the VIX, grinding more than 40% below early-June peaks by last week, relative market calm had replaced the initial flight from risk seen after U.S. President Donald Trump accused China of ‘breaking’ the trade the deal. But after complacency got the better of investors earlier in the year, there’s little appetite to see assumptions upended again. On Tuesday the volatility gauge revived well ahead of Fed news after Washington officials played down what could be achieved when Trump meets China’s President Xi Jinping.

To be sure, Washington’s tone hasn’t hardened much. U.S. Commerce Secretary Wilbur Ross noted last week that the G20 was too broad for detailed progress. Markets have been prepared for weeks for a best-case scenario that would merely see further tariffs suspended. Contained expectations ought to mean that any disappointment will also be limited.

In itself, the fact that there are concrete plans for a meeting at all has reduced the risk of further escalation. Donald Trump’s repeated boast of a warm relationship with Xi should also level off dangers that their dispute will deepen in Osaka. Trump has twice agreed to postpone tariff hikes: with the European Union’s Jean-Claude Juncker last July and with Xi in December.

On the downside, Mexico’s agreement to further clamp downs on illegal border crossings after tariff threats may embolden Trump. Furthermore, the likelihood of monetary easing may convince the President that the U.S. will soon have an economic cushion. Given his evident desire for rate cuts, he may even see a chance of killing two birds with one stone.

Here are the latest key developments and points to watch in the run up to the G20 meeting:

- U.S. Trade Representative Robert Lighthizer and Treasury Secretary Steven Mnuchin spoke with China’s Vice Premier Liu He on Monday

- Details are scarce about the discussions, but China’s Commerce Ministry said the two sides agreed to keep talking

- The trio will reportedly meet ahead of the summit to prepare an agenda

- Trump has recently shifted emphasis from the U.S.’s $420bn trade deficit with China to broader calls for China to address intellectual property concerns, subsidies, and more

- There appears to be zero chance that the two sides will agree to more than a pause in tariffs hikes, but the outside chance of de-escalation represents stock markets’ biggest upside risk

Chart thoughts

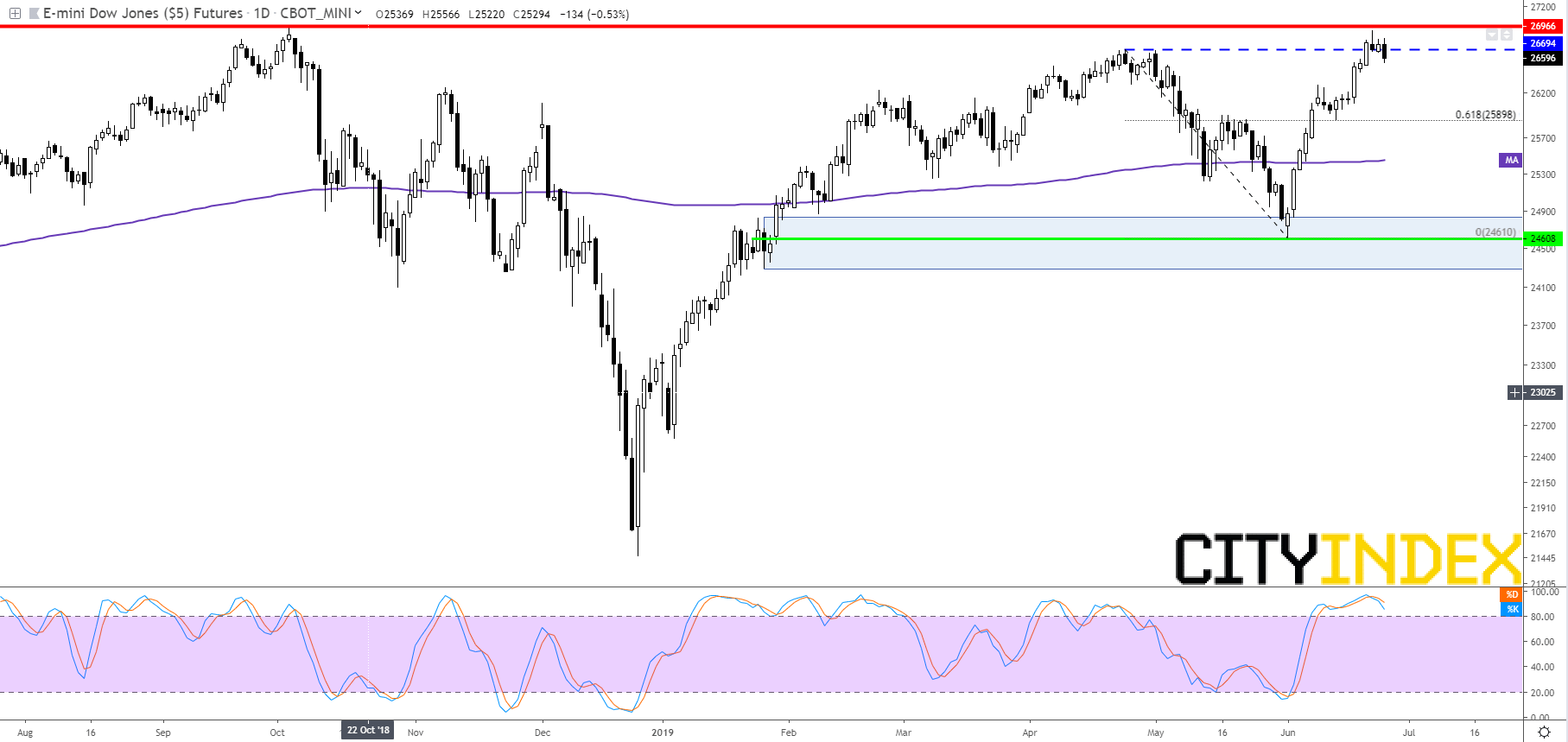

Perhaps one of the biggest prizes, from a chart perspective, would be the possibility that trade-sensitive Dow industrials finally take the index to fresh peaks. The Dow continues to lag Nasdaq indices and the S&P 500, which marked new records in recent weeks. True, the DJIA missed a return to October’s top by just a fraction of a percentage. Nevertheless, the symbolic failure was enough to force prices back through key support. A close by Dow futures above 26694, a pivot formed in April and May, could prevent a deeper consolidation. Failing that, another visit to 61.8% of the 24th April to 31st May slide would be on the cards. That natural support held two weeks ago. Nor does pricing favour a sustained breach of the 200-day moving average. (Though if seen, expect 3rd June’s low to be magnetic). For now, the Dow’s problems are more on the upside than on the downside. Like trade resolution, a break higher may remain out of reach for a while yet.

Dow Jones E-Mini Future (CBOT) - [20.15 BST, 25-06-2019]

Source: Tradingview/City Index

Latest market news

Yesterday 03:30 PM

Yesterday 01:23 PM

Yesterday 11:00 AM

Yesterday 08:15 AM

Latest Interest rates articles

March 7, 2024 03:34 PM

February 9, 2024 04:37 PM

December 13, 2023 08:10 PM

November 27, 2023 08:19 PM