Stocks set for volatile Monday as Greek vote looms

The stock market open on Monday could be a messy one and very difficult to predict given the uncertain outcome of Sunday’s Greek vote, with […]

The stock market open on Monday could be a messy one and very difficult to predict given the uncertain outcome of Sunday’s Greek vote, with […]

The stock market open on Monday could be a messy one and very difficult to predict given the uncertain outcome of Sunday’s Greek vote, with the latest polls contradicting each other and showing strong support for both camps. As far as the equity market is concerned, the best outcome would probably be if the Greeks voted “yes” to the proposals offered by Greece’s creditors. Although this may see Alexis Tsipras step down as Prime Minister, it would most likely safeguard Greece’s membership in the euro zone, removing some near-term uncertainty hanging over the markets. In contrast, a “no” vote would increase the risks of a “Grexit” which could weigh heavily on risk appetite early next week.

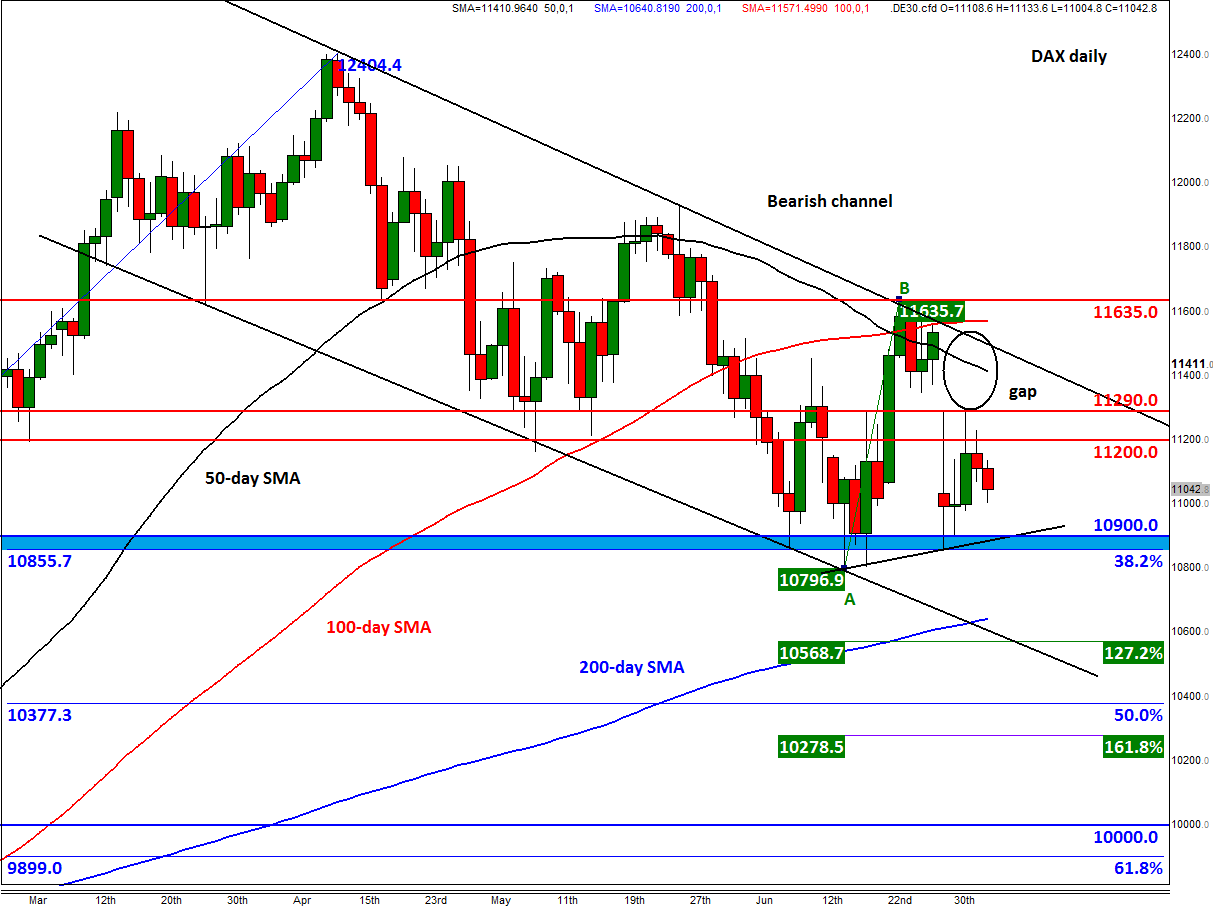

Traders will be watching the major European indices, such as Germany’s DAX, with keen interest as the drama unfolds in Greece. From a purely technical point of view, the DAX has failed to entirely ‘fill’ its weekend gap, as it twice ran into strong selling pressure this week around 11290. It is likely that there will be a cluster of stop buy orders sitting some distance above this key level, which may get triggered early next week. If that happens, it could lead to a sharp rally – possibly all the way to last Friday’s close and the resistance trend of the bearish channel around 11530, and potentially beyond. If the DAX goes on to break out of the bearish channel then the June high of 11635 would be the first logical resistance level that would need to be tackled. Once cleared, the path of least resistance would be unambiguously to the upside.

Meanwhile if the outcome of the Greece referendum (or otherwise) causes a rise in risk aversion next week then the index may continue drifting lower inside its bearish channel. In this scenario, a closing break below the 10855-10900 support range, which held firm throughout June, would be a particularly bearish outcome. The lower end of this range corresponds with the 38.2% Fibonacci retracement level of the upswing from the October low. There is also a chance that the index could gap below this area – the bulls need to be wary of this possibility as it could prove very costly, as some must have found out earlier this week. Below 10855-10900, the next potential support could be the June low at just below 10800. Thereafter is the 200-day moving average at 10640 followed by the 127.2% Fibonacci extension level of the intra-month upswing in June, at 10570. The support trend of the bearish channel also comes into play here, making it a key level.