Yesterday, 25 Jun “sell-off” seen in U.S. stocks have saw losses within the range of -1.00% to -1.5% among the key U.S. benchmark stock indices, the 3rd day of consecutive decline with the higher beta tech heavy Nasdaq 100 being hit the hardest.

Primary triggers have been negative news flow from “Fed Speak” and G20 as reported yesterday;

- Fed official Bullard was quoted in a media report that he favoured a 25 bps cut on the Fed funds rate to act as “an insurance” to buffer slower economic growth rather than a 50 bps reduction. This news flow triggered a negative feedback loop into the markets as the Fed funds futures have priced in a 42% probability of a 50 bps cut a day ago on 24 Jun based on CME Fed Watch tool.

- U.S. administration has stated that plans have been made to suspend the next round of tariffs on an additional US$300 billion of China imports ahead of G20 summit. Also, U.S. will not accept any further conditions on tariffs as part of reopening trade negations with China and no detailed trade deal is expected from the Trump-Xi G20 meeting as quoted by media from a senior U.S. administration official.

Media reports have attributed the sell-off seen in U.S stocks from the probable “less rosy” outcome from Trump-Xi G20 meeting where a trade deal will not be struck between U.S. and China. Interestingly, a week ago where media had interviewed the investing and political analysts’ community and most of them have a bias that a trade deal will not materialise after the G20 summit.

Thus, yesterday’s G20 related news have already been priced into the markets. In fact, the U.S. administration’s latest plan to delay additional tariffs on China imports has shown a “toned down hawkish stance” and the willingness to restart trade negotiation talks with China is rather a positive catalyst. Click here for a recap on our G20 preview.

Therefore, the 3-days of consecutive decline seen in stocks may have been overdone and since now the media has spin “a less rosy” outcome from Trump-Xi meeting and if any encouraging trade related remarks from U.S. administration after the meeting can easily trigger a positive feedback loop back into stocks and risk assets.

Now, lets us review the technical structure on the Hang Seng Index, a key China related play that can be impacted from G20 news flows.

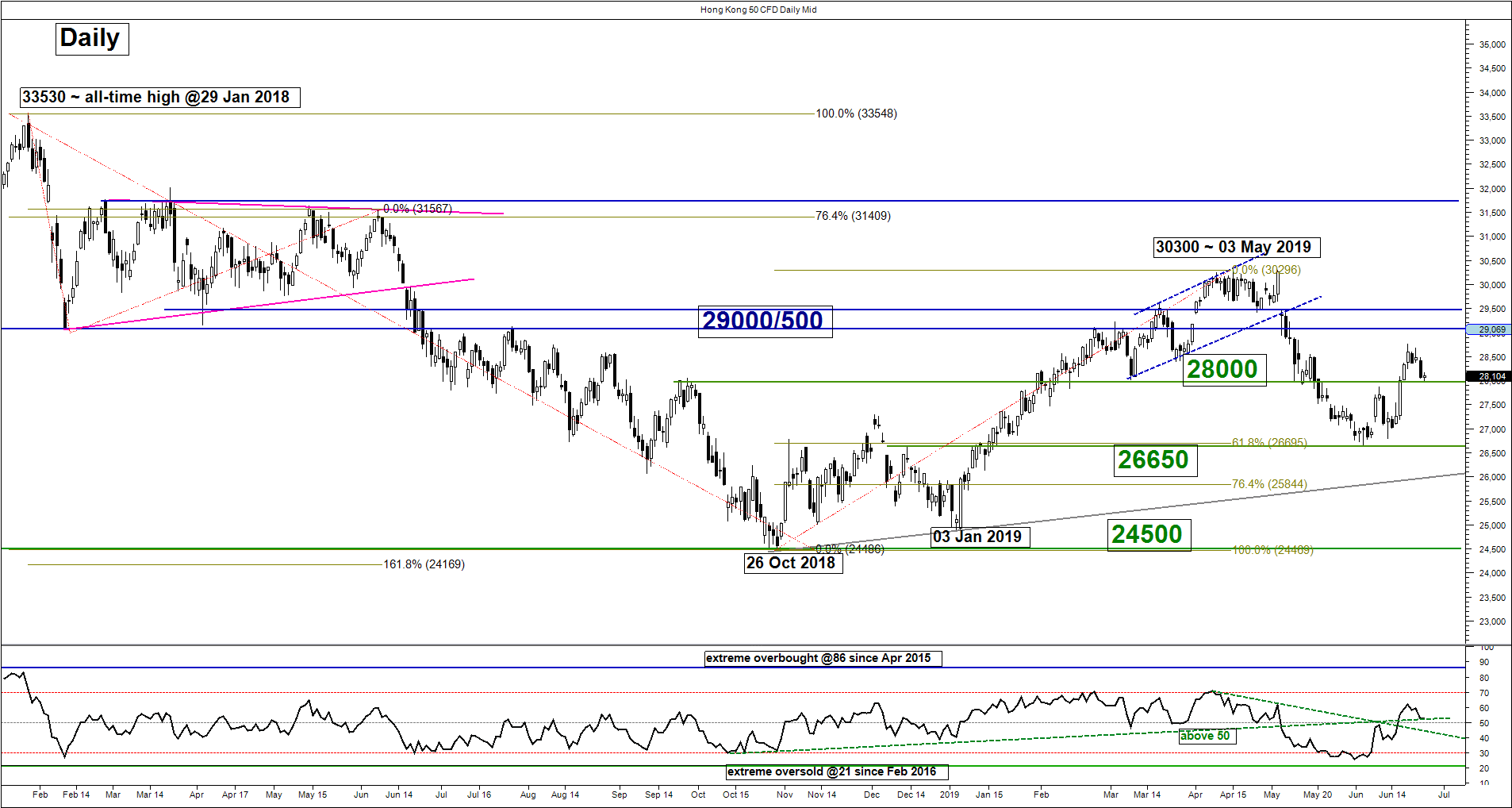

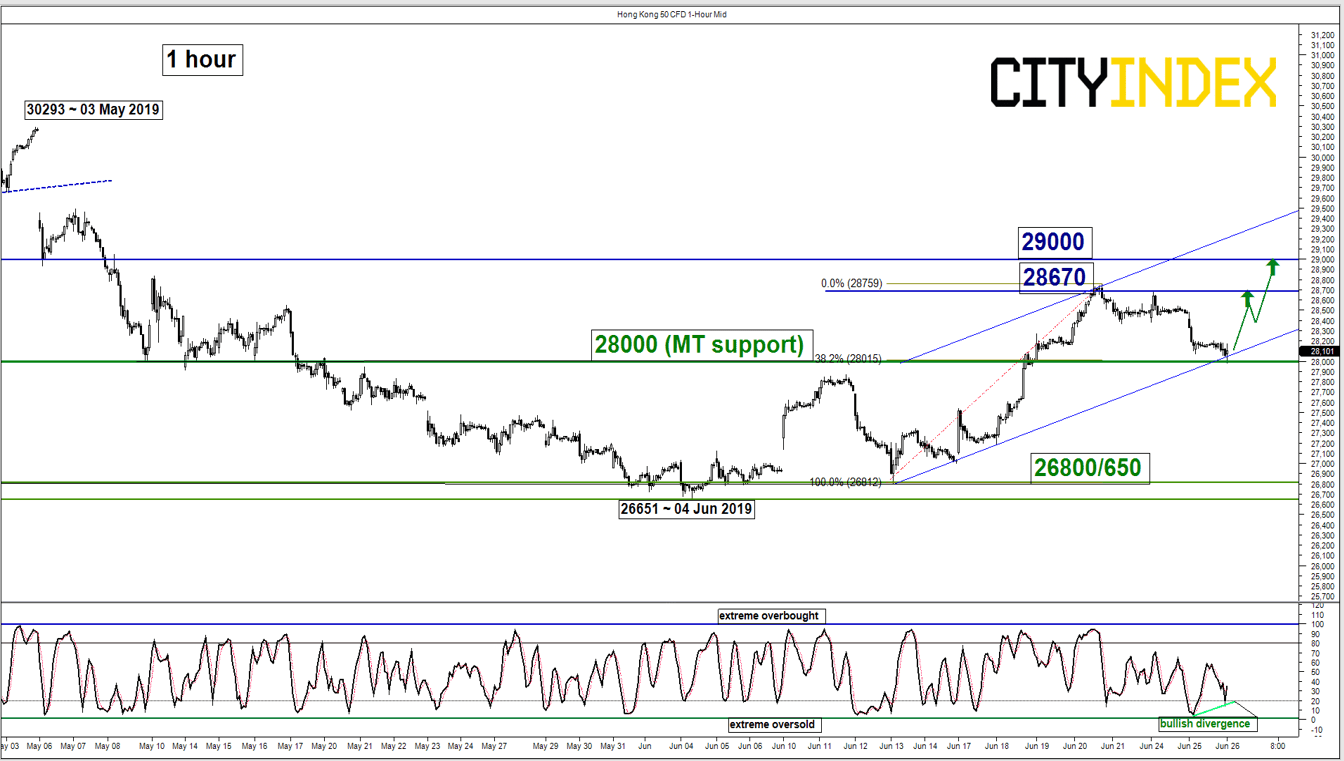

Short-term technical outlook on Hang Seng Index/Hong Kong 50 (Wed 26 Jun)

click to enlarge charts

Key technical elements

- Since its high of 28756 printed on 20 Jun 2019, the Hong Kong 50 Index (proxy for Hang Seng Index futures) has declined by -2.7% to print a current intraday low of 27982 as at today, 26 Jun Asian session.

- Interestingly, the decline has led to a test on the predefined key medium-term pivotal at 28000 (click here for a recap on our weekly technical outlook report) with positive elements.

- The daily RSI oscillator is now resting on a significant corresponding support at the 50 level with a bullish divergence signal seen in the shorter-term hourly Stochastic oscillator at its extreme oversold level. These observations suggest that the recent downside momentum has started to ease.

- The 28000 key medium-term pivotal support also now confluences with the lower boundary of the minor ascending channel in place since 13 Jun 2019 low.

Key Levels (1 to 3 days)

Pivot (key support): 28000 (medium-term pivot)

Resistances: 28670 & 29000

Next support: 26800/650

Conclusion

If the 28000 key medium-term pivotal support holds, the Index is likely to see a potential recovery to retest the recent 20 Jun minor swing high area of 28670 before targeting the next resistance at 29000.

On the other hand, a daily close below 28000 invalidates the recovery scenario for a further decline towards the next support at 26800/650 (the aftermath of the recent local HK street protests over the China extradition bill).

Charts are from City Index Advantage TraderPro

Latest market news

Today 08:18 AM

Yesterday 10:40 PM

Latest China articles

March 26, 2024 04:11 AM

March 13, 2024 04:47 AM

March 6, 2024 05:47 AM

February 22, 2024 01:21 AM