The mood in the market remains depressed on Wednesday as coronavirus concerns coupled with geopolitical tensions drag on risk sentiment. Equities across the board are out of favour whilst safe haven gold is consolidating just shy of $1800 after jumping 1% so far this week and hitting $1797, its highest level since 2012.

New daily US coronavirus cases dipped slightly at the start of the week. However, Tuesday’s figures have shown its premature to say that numbers are falling. COVID-19 concerns were further fueled by warnings from several Federal Reserve officials that rising coronavirus numbers in the US could jeopardize the economic recovery. The timing here of the rising numbers in the sunbelt is extremely important given that some stimulus programmes are due to expire soon.

US considers sanctions on Hong Kong & HSBC

Geopolitical tensions are also back in focus amid reports that the White House is toying with the idea of striking against the Hong Kong Dollar peg in retaliation for China’s national security law. Whilst the Hong Kong Dollar has shrugged off the reports, HSBC is under pressure as the Trump administration also considers sanctions against banks in the city.

Geopolitical tensions are also back in focus amid reports that the White House is toying with the idea of striking against the Hong Kong Dollar peg in retaliation for China’s national security law. Whilst the Hong Kong Dollar has shrugged off the reports, HSBC is under pressure as the Trump administration also considers sanctions against banks in the city.

HSBC is caught in a political tug of war between the US and China. Asia is the biggest regional contributor to HSBC income highlighting the importance of the region to the business. However, sanctions from the US would be extremely damaging. The share price in London is still down 40% year to date, reflecting the troubles at the bank, compared to Barclays, for example which trades -26% lower year to date.

Rishi Sunak’s Summer Statement in focus

The Chancellor Rishi Sunak is set to take centre stage as he delivers his Summer statement, outlining the economic stimulus package which he will implement to steer the UK economy through the coronavirus crisis. The focus is set to be on jobs, both the protection and creation of jobs as he attempts to pull the UK economy out of the deepest economic downturn in 300 years.

In addition to jobs focus on business costs would be beneficial with immediate effect. More business rate relief, the pre-announced stamp duty holiday and targeted VAT cuts, particularly for the leisure and hospitality sectors would be well received. These measures could see house builders and leisure and hospitality stocks rally, whilst business rate cuts could see battered retail sector rise.

Should Rishi Sunak underwhelm, stocks, particularly on the FTSE250 could come under pressure among with the Pound.

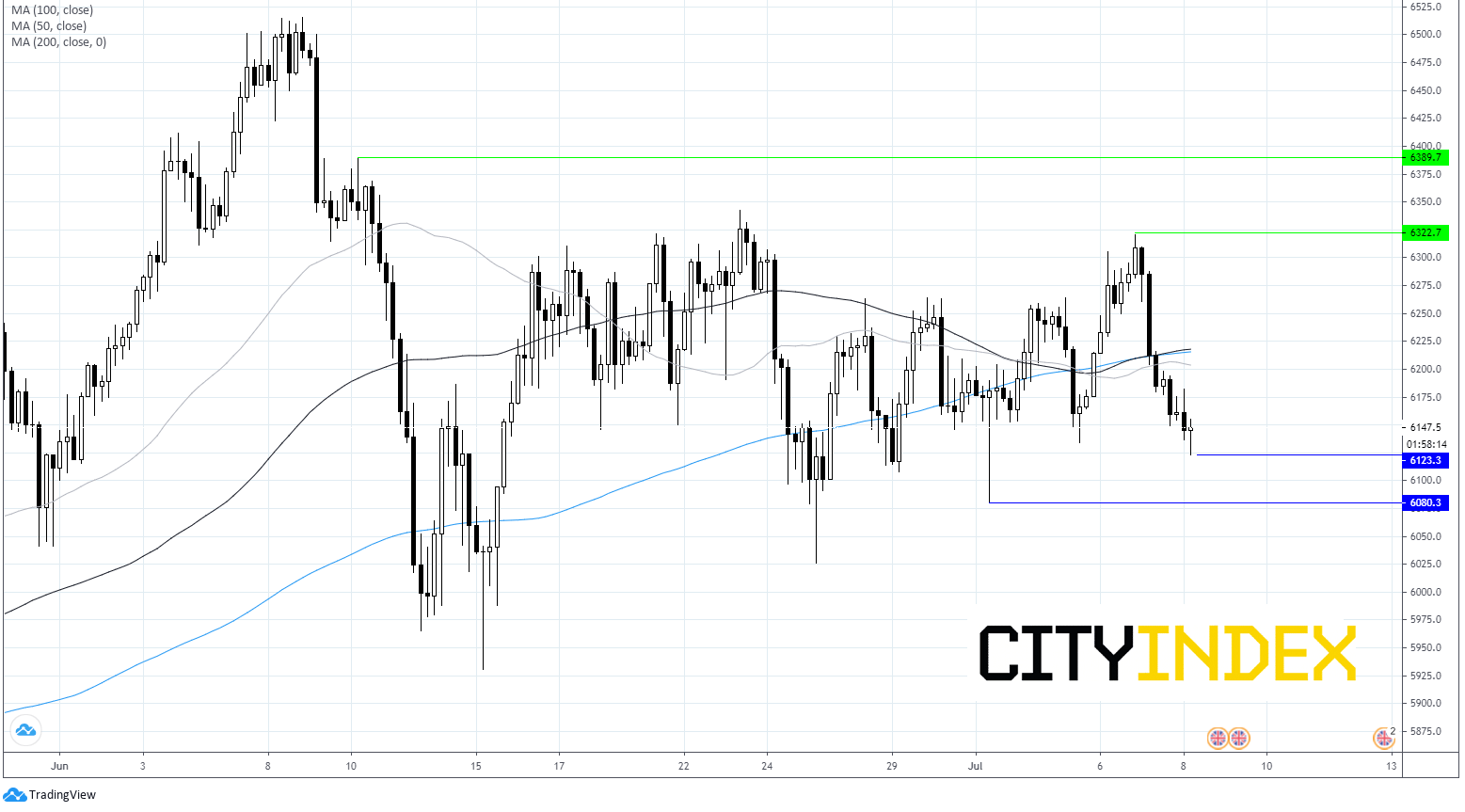

FTSE 100 Chart

Latest market news

Yesterday 03:30 PM

Yesterday 01:23 PM

Yesterday 11:00 AM

Yesterday 08:15 AM

Latest FTSE 100 articles

March 11, 2024 04:30 PM

March 5, 2024 12:00 PM

February 12, 2024 10:30 AM

January 15, 2024 12:30 PM