Risk aversion returns with stocks opening on the back foot after UK GDP dramatically misses forecasts, amid elevated US China tensions over offshore resources in the South China Sea and intensifying coronavirus fears. Upbeat China data showing a strong rebound in both imports and exports has been shrugged off.

A late sell off on Wall Street spilled over into Asia and is dragging on European stocks on the Open.

Sentiment soured on Wall Street after the state of California imposed new restrictions on business as coronavirus cases spiral out of control and hospitalisations soar. The shutdown fuels fears that the growing number of coronavirus cases will hamper the fragile economic recovery.

The fresh US restrictions come after the WHO gave a stark warning that the pandemic could get worse and worse with too many countries headed in the wrong direction. The comments from the WHO Chief came after 230,000 new daily cases were record, in the worst day of the crisis so far.

UK GDP +1.8% vs 5% expected

UK economic growth massively under shot expectations increasing just +1.8% month on month as lockdown measures were gradually eased. This is a very shallow rebound given the -20.4% contraction in April. Analysts had been expecting a 5% jump in GDP in May. The data reveals that the UK economy is recovering at a much slower pace than initially expected pouring cold water over any V-shaped recovery talk.

However, it was only at the end of May that non-essential shops reopened and the leisure and hospitality sectors remained behind closed doors. With these sectors reopening in June, the data should steadily keep improving. Patience will be the name of the game here. Andrew Bailey pointed out yesterday there are signs of economic recovery, but there is still a very long way to go.

A bright spot in the raft of UK data released was UK manufacturing production which rebounded at a much stronger rate than expected, jumping +8.4% mom in May, rebounding from -20.9% in April. Whilst the manufacturing sector only accounts for around 10% of activity in the UK economy, the data was offering some support to the Pound which dropped just 0.1% following the disappointing GDP reading.

US banks earnings & US inflation

Looking ahead big swings are expected in the US banking sector as JP Morgan, Citigroup and Wells Fargo kick off the banks’ earnings season. Financials have been badly hit in the coronavirus crisis and have underperformed the broader market in the recovery. The second quarter earnings are expected to be the nadir. We could see investors looking to buy the bottom once the scale of the coronavirus impact is out in the open.

US inflation data is expected to show +0.5% increase mom in June, up from -0.1% decline in May. Whilst the data would show the US economic recovery is on the right track optimism could be offset by fears that the rolling back of reopening measures could undermine the economic recovery.

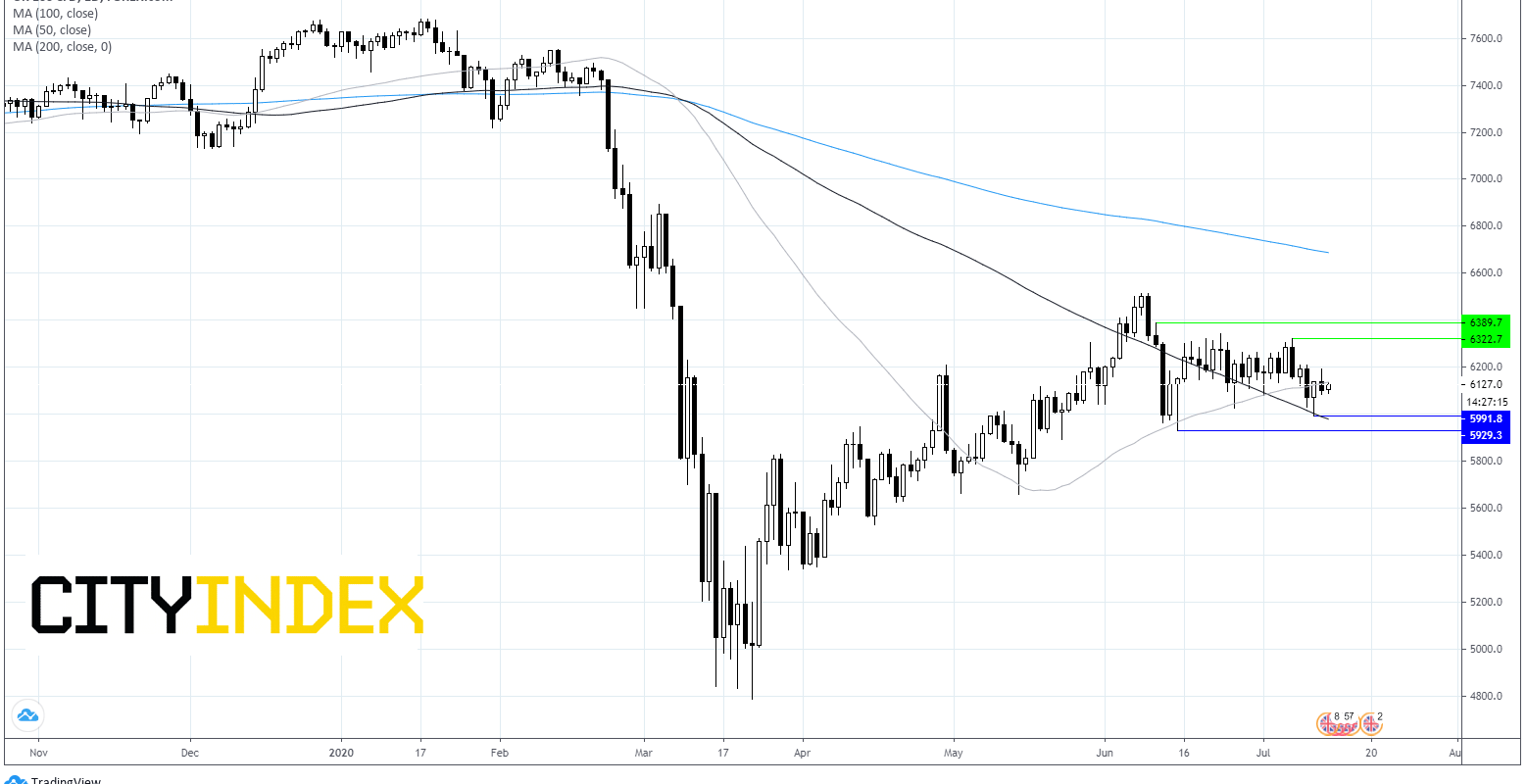

FTSE Chart

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Yesterday 01:23 PM

Yesterday 11:00 AM

Latest FTSE 100 articles

March 11, 2024 04:30 PM

March 5, 2024 12:00 PM

February 12, 2024 10:30 AM

January 15, 2024 12:30 PM