This morning saw the markets continue to trade in the way you would expect when rate cuts are on the horizon with stocks, bonds, gold, silver and foreign currencies all rallying against the US dollar. Some investors clearly like the idea of holding stocks as interest rates are now likely to remain low for longer than was previously the case. But I wonder if growth concerns will ultimately outweigh the boost stocks have received from renewed dovish stance by central banks, and therefore prevent an even bigger rally. So this could be a short-lived rally for equities.

Dovish central banks galore

Investors welcomed yesterday’s news that the Fed has caved in to pressure and opened the door to a rate cut as early as next month with nearly half of the FOMC members expecting two rate cuts before the year is out. As a result, the probabilities of July and September rate cuts improved further as investors became more convinced about the Fed’s U-turn on monetary policy. This came after Mario Draghi strongly hinted at the prospects of a rate cut by the ECB earlier in the week. Overnight, the Reserve Bank of Australia’s Philip Lowe said “it is not unrealistic to expect a further reduction” in interest rates, while the Bank of Japan said it expected to keep ‘extremely low rates at least through spring 2020’. The Bank of England also appeared slightly more dovish than expected as it acknowledged risks to growth had risen owing to global trade tensions and the increased likelihood of a no-deal Brexit. However, not all central banks are dovish. The Norges Bank hiked interest rates today by 25 basis points to 1.25% — although this was expected, living up to its status as the only major hawkish central bank among the developed economies.

Are investors overreacting?

But when the dust settles down and investors realise why central banks are cutting interest rates, the jubilations could turn to despair. Rates are being cut because the global economy is, or perceived to be, slowing down amid the escalation of geopolitical risks. With global interest rates already so low, how much of a boost would the economy get from (the promise of) a 25 or 50 basis point reduction in interest rates? Granted, it will increase the marginal supply of cheap credit further, but that is not the issue here; it is all about marginal demand, or lack thereof, for cheap loans from consumers and businesses because of the latest or upcoming interest rate cuts. I think the law of diminishing returns apply here. Also, with central banks keeping rates so low for such a long period of time, what will happen if the economy were to deteriorate even further? Will the Fed and other central banks have any more monetary policy tools left at their disposals then? And what about a situation where we see a sudden economic recovery or a big jump in inflation? Surely in this event, central banks will have to tighten their belts quickly, potentially choking off growth prematurely. So, whichever way you look at it, central banks have pushed themselves into a corner here.

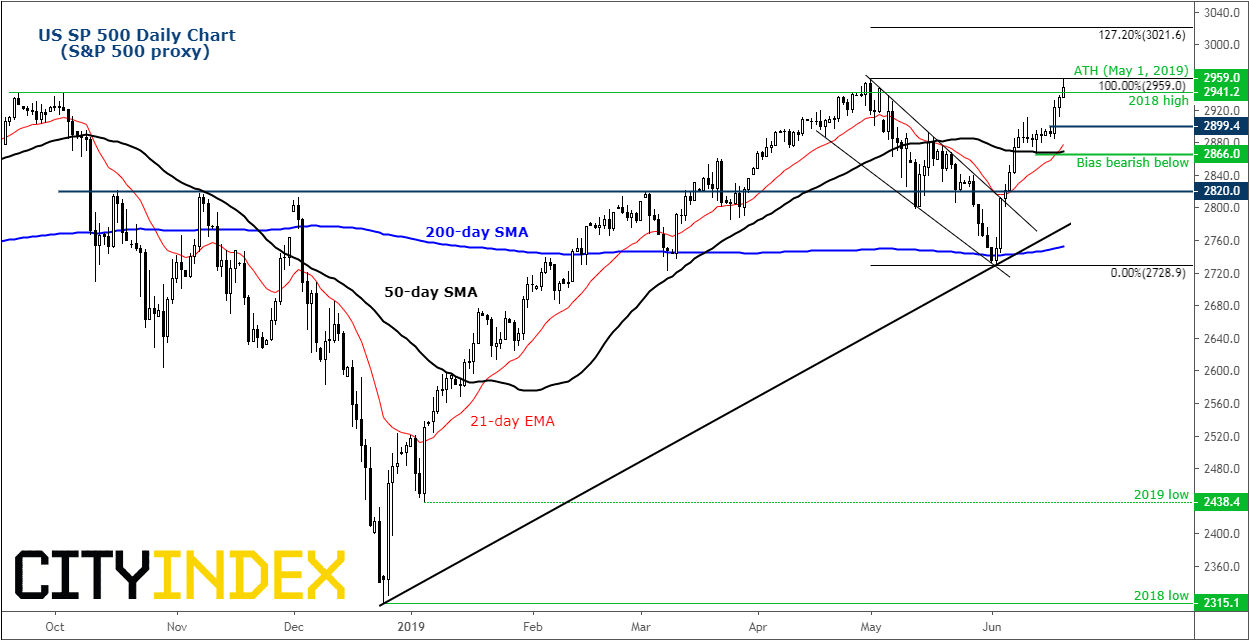

S&P 500 hits new record

But for now traders seem happy to take advantage of the renewed bullish momentum and the S&P 500 could hit new unchartered territories before we see a potential pullback. All it took to get us here was a complete capitulation by central banks! We have identified a few levels on the S&P 500 which could be interesting to watch. The index has already hit a new high above the previous all-time high at 2960 today, but it has eased off slightly. Where it closes today’s session will be important. A close above this level would keep the bulls happy for a while yet, which could see the index aim for 3K next. However a sharp rejection against 2960 could see the bears return quickly. In the event of a sell-off, the next potential support to watch is at 2899/2900, the key breakout point. If this eventually breaks though then the bulls will be in trouble and more so should the last low prior to the latest rally gives way too, at 2866.

Source: Trading View and City Index. Please note this product may not be available to trade in all regions.

Latest market news

Today 08:33 AM

Latest Indices articles

Yesterday 11:00 AM

April 16, 2024 08:00 PM

April 16, 2024 04:54 PM

April 15, 2024 06:08 AM