Stocks Banks lead European market bounce earnings in focus

European stock markets have turned higher, led by banks, although HSBC’s disappointing earnings results and the underperforming mining stocks were still keeping the UK’s FTSE […]

European stock markets have turned higher, led by banks, although HSBC’s disappointing earnings results and the underperforming mining stocks were still keeping the UK’s FTSE […]

European stock markets have turned higher, led by banks, although HSBC’s disappointing earnings results and the underperforming mining stocks were still keeping the UK’s FTSE 100 in the negative territory as went to press. Nevertheless, investors don’t seem to be too concerned about China after the latest manufacturing PMI data there failed to provide any positive or nasty surprises. They are still in an upbeat mood after equities have just had one of their best months in recent years, thanks in part to the promise of more stimuli from the ECB, and dovish central banks elsewhere (the Fed being the only exception). As well as decent earnings results from Commerzbank, sentiment in the banking sector has improved today after the European Central Bank’s stress tests on the big four Greek lenders showed a capital shortfall of only €14 billion. This outcome was much better than many had feared. As a result, shares in Greek banks are surging higher.

At the end of last week, the markets paused for breath as investors digested US quarterly earnings, economic data and central bank announcements. Although the European Central Bank had delivered a super dovish message at its press conference a couple of weeks ago, there were no such remarks from the Bank of Japan, while in the US, the Federal Reserve suggested that a 2015 lift off was still a possibility. However the incoming macro data have been far from convincing, while inflation is literally non-existent across many developed economies.

Indeed the latest data from China, the world’s second largest economy, was lacklustre to say the least. At the weekend, the official manufacturing PMI for October came in unchanged at 49.8, disappointing expectations for an increase to 50.0. The Caixin Manufacturing PMI, released overnight, was even weaker at 48.3, though it was still up from 47.2 previously and better than 47.7 expected. The former has now remained below the expansion threshold of 50 for the third straight month, while the latter has only been above 50 once this year – in March. Meanwhile, the official Non-Manufacturing PMI expanded at a slightly slower pace of 53.1 in October, down from 53.4 previously.

In Europe, however, the PMIs were mostly better-than-expected, with Spain being the only weak spot where the PMI fell to 51.3 from 51.7 previously. Nevertheless, this was overshadowed by stronger readings from Italy, France and Germany, which helped to lift the final Eurozone manufacturing PMI to 52.3 from 52.0 previously. The UK Manufacturing PMI meanwhile came in at 55.5 for October. Not only was this much higher than 51.3 expected and 51.8 recorded in September, it was also the strongest print since June 2014.

The combination of ultra-low interest rates and inflation, combined with a weaker euro, continues to boost the appeal of European stock markets in particular. Here, equities could get a further lift if the upcoming corporate earnings results provide positive surprises. Today’s results have been mixed. Commerzbank has reported that its third quarter profit rose by an above-forecast 25%, with the bank also confirming that it plans to pay investors a dividend for the first time since 2007. HSBC, however, reported a 4% decline in revenues, although its pre-tax profit beat forecasts. After a weaker start, share in Ryanair have risen after the low-cost Irish carrier lifted its full year passenger numbers and profits forecasts.

Some of this week’s key earnings/trading statements to watch out for:

Tuesday:

Wednesday:

Thursday:

Friday:

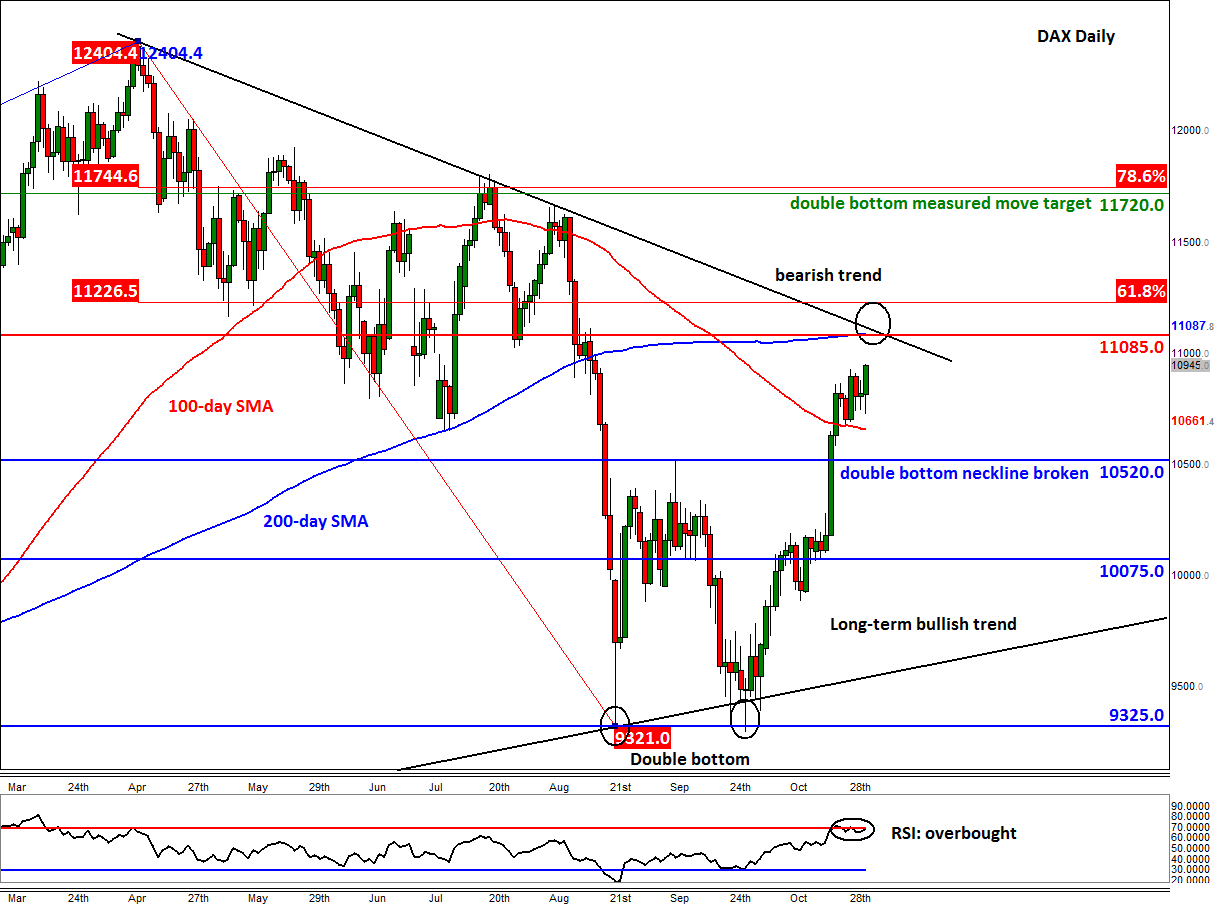

Technical outlook: DAX

From a technical point of view, the DAX’s sustained break of the double bottom neckline at around 10500/20 is a positive outcome. There is not much further resistance seen in the immediate near-term until we reach the 11085 to 11225 range. This area is where a bearish trend converges with the 200-day average and the 61.8% Fibonacci retracement of the down move from the record high. If and when this key resistance area is cleared then a run towards the double bottom target at 11720 could get underway. This target is derived by adding the height of the double bottom pattern (10520-9320 = 1200) to the neckline (10520). Incidentally, this 11720 level comes in just ahead of the 78.6% Fibonacci retracement at 11745. Beyond these levels, there are no further significant resistances until the all-time high of around 12400. Meanwhile, the RSI momentum indicator suggests the market may be a bit overbought, so short-term bullish speculators may wish to proceed with a degree of caution from here especially while the bearish trend is still in place.