Thin air at highs accounts for sterling fall more than Corbyn’s debate performance

Labour’s Jeremy Corbyn didn’t ‘lose’ the first big TV debate of the election campaign by a big enough margin. Hence the result pretty much qualifies as a ‘draw’, according to a poll conducted and released immediately after the screening. YouGov’s snap poll gave the Conservative’s Boris Johnson the win by 51% to 49%. But the research firm also said 67% of respondents thought Jeremy Corbyn performed well.

It’s the first campaign setback for Johnson, who’s Conservatives saw their highest lead yet in weekend polls, 17 points above Labour. Sterling has reacted negatively. It’s a second-straight declining session after the rate vs. USD broke a four-day run higher on Tuesday for a first clear reversal since earlier in the month.

In a sense, the chorus of opinion that saw Johnson as having more to lose from participating in the debate than Corbyn has proved correct. Labour, who have trailed the Tories all year, still have little chance of winning more votes than the incumbent party, according to polls. But, Johnson’s failure to crush his opponent—in terms of ‘intangible’ performance standards—is raising doubts; with voters and traders.

Still, a key question is whether the debate changes election prospects much. If it doesn’t, sterling’s downturn may turn out to be a shallow one. YouGov’s latest poll, out on Wednesday morning, had the Conservatives on 43% vs. Labour’s 30%. That’s a two-point drop for the Tories since the research firm’s weekend poll, and a two-point uptick for Labour. Both changes can be read as a reaction to the TV debate. On the other hand, whatever the cause, pollsters’ have had a terrible record of predicting the outcome of public votes over the last few years. As such, it’s doubtful that the debate verdict can be accorded more significance than as a Labour blip.

This does not mean that sterling bulls will necessarily double down on pound buys. GBP/USD remains about 8% higher above August lows. That more than prices a possible Conservative election that affords a sufficient parliamentary majority to approve Boris Johnson’s Brexit deal. At the same time, the elevation may misprice Britain’s growing economic vulnerability and continuing uncertainty about the next stage of Britain’s EU departure, when substantive negotiations on a post-split relationship begin. Even so, incentives to commit hard to a fresh bearish stance also look light for the moment. Implied volatility in sterling trades is on the wane overall, though this may change as the election draws nearer.

Chart thoughts

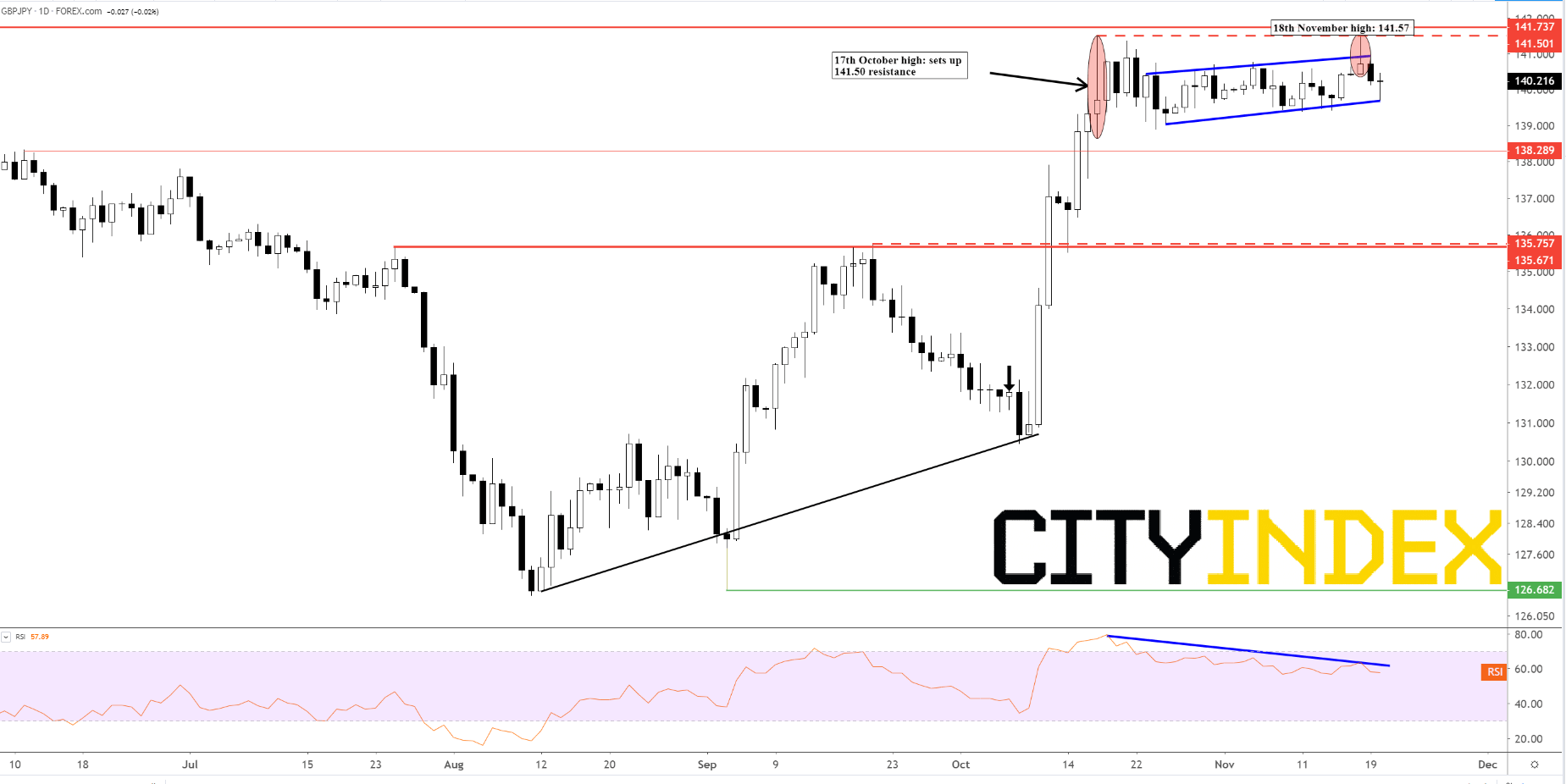

Technically, a pound reversal has been a heightened probability since 17th October. The rate reached ¥141.50 on that date, just short of an aggressive looking failure high from 21st May that appears to have capped sterling about five months later. Systemic resistance is thus continuing to exert pressure. The challenge for sterling is underlined by its relatively range bound progress since October tops, with corroboration from clear rejection after notching ¥141.57 earlier this week. Also since mid-October, divergence has built between price trend and RSI trend, topped by a classic higher high on Monday 18th November. The momentum gauge failed to replicate that. None of the foregoing predicts much about the depth of any sustained correction. Indeed, longer-term oscillators point to more upside before exhaustion. A better tell may be whether GBP/JPY breaks below the flag that began to develop in October’s final week. If it does, the next level to watch would be an intermediate-looking one from mid-June at ¥138.29. Below, high-135s were marked by the last daily gain in July before a sharp down leg to the year’s lows in August. September tops also echo high-135s. Let’s see how distant they remain in the short term.

GBP/JPY – Daily [15.20 GMT, 20th November 2019]

Source: City Index

Latest market news

Today 10:37 AM

Today 08:25 AM

Latest GBP articles

Yesterday 12:26 PM

May 4, 2024 08:00 PM

April 3, 2024 02:49 AM

March 29, 2024 10:00 PM