Sterling set for another boost from inflation

Updated 5.34pm BST One of the more pleasant surprises in the wake of the Brexit vote has been undeniable resilience among Britain’s consumers, particularly on […]

Updated 5.34pm BST One of the more pleasant surprises in the wake of the Brexit vote has been undeniable resilience among Britain’s consumers, particularly on […]

The next UK consumer gauge of note will be an update of the official Consumer Price Index (CPI) which will be released on Tuesday 13th September.

It’s been difficult to stand down the alert for a potential near-term upset entirely.

Last week’s British Retail Consortium data showed buyers cut back in August following July’s splurge, supporting the view that good weather and preventative discounting by retailers provided a temporary boost. The weather and promos also partly account for a big bounce in sentiment published by GfK at the end of last month.

Even so, we’re reluctant to play down July’s better-than-expected 0.6% annual CPI rate too much. The absence (in July) of June’s airfare hikes during the European Cup had been expected to shave off a tenth of a point. The lack of that impact (transport actually rose 1.6% after 1.1% in June) led the ONS to state that it saw no obvious impact yet from the referendum. Overall, July’s CPI forced forecasters to reconsider strong spending on discretionary goods on top of stabilising fuel prices after a 14 percentage point bounce in July.

Unfortunately, the more damaging side of the inflation rebound has also begun to show its face.

Sterling’s depreciation has already tightened the raw materials supply chain, lifting manufacturing input prices 4.7% annually in July, the most for three years, leading to a two-year high in the output price balance. The price expectations component of the CBI’s August Industrial Trends Survey consequently also reached a two-year high, suggesting input price inflation will accelerate.

That said, the tough deals large retailers infamously have with suppliers these days (several years-long contracts are now common) and the general atmosphere of uncertainty should prevent widespread haste in passing on price rises.

We therefore expect inflation to have at least continued along a resilient but unspectacular path in August.

We see a largely static 0.6%-0.7% yearly headline reading and a tick above zero from -0.1% month-month at the core, lifting the annual rate fractionally from July’s 1.3%.

At present, in our view, the pound’s rate against the euro is simpler to read through the Eurozone and UK economic backdrops than gauging the US economy to trade sterling against the dollar.

EUR/GBP is not without nuances though. The ECB kept policy on hold on Thursday triggering a near-customary post-ECB euro rally.

However, ECB president Mario Draghi also said on Thursday that he had asked internal committees to look at options to ensure smooth running of asset buys. Draghi had used similar language at the October 2015 meeting, which was followed by an easing package six weeks later. On Friday, Eurozone economic unease was underscored after German data showed exports fell unexpectedly in July. It was their steepest drop in nearly a year. Imports also edged down, in a further sign that Europe’s biggest economy started the third quarter on a weak footing.

There will be multiple tests of the pound’s recent resilience from macroeconomic data next week. Tuesday’s CPI release will be accompanied by producer price inflation readings, employment updates will come on Wednesday, and Retail Sales and the Bank of England decisions on Thursday. We look for retailers to report moderated but continued momentum and think the Bank will be on hold till November. At present, we therefore expect to trade sterling through the remainder of the week on the same short-term bullish view.

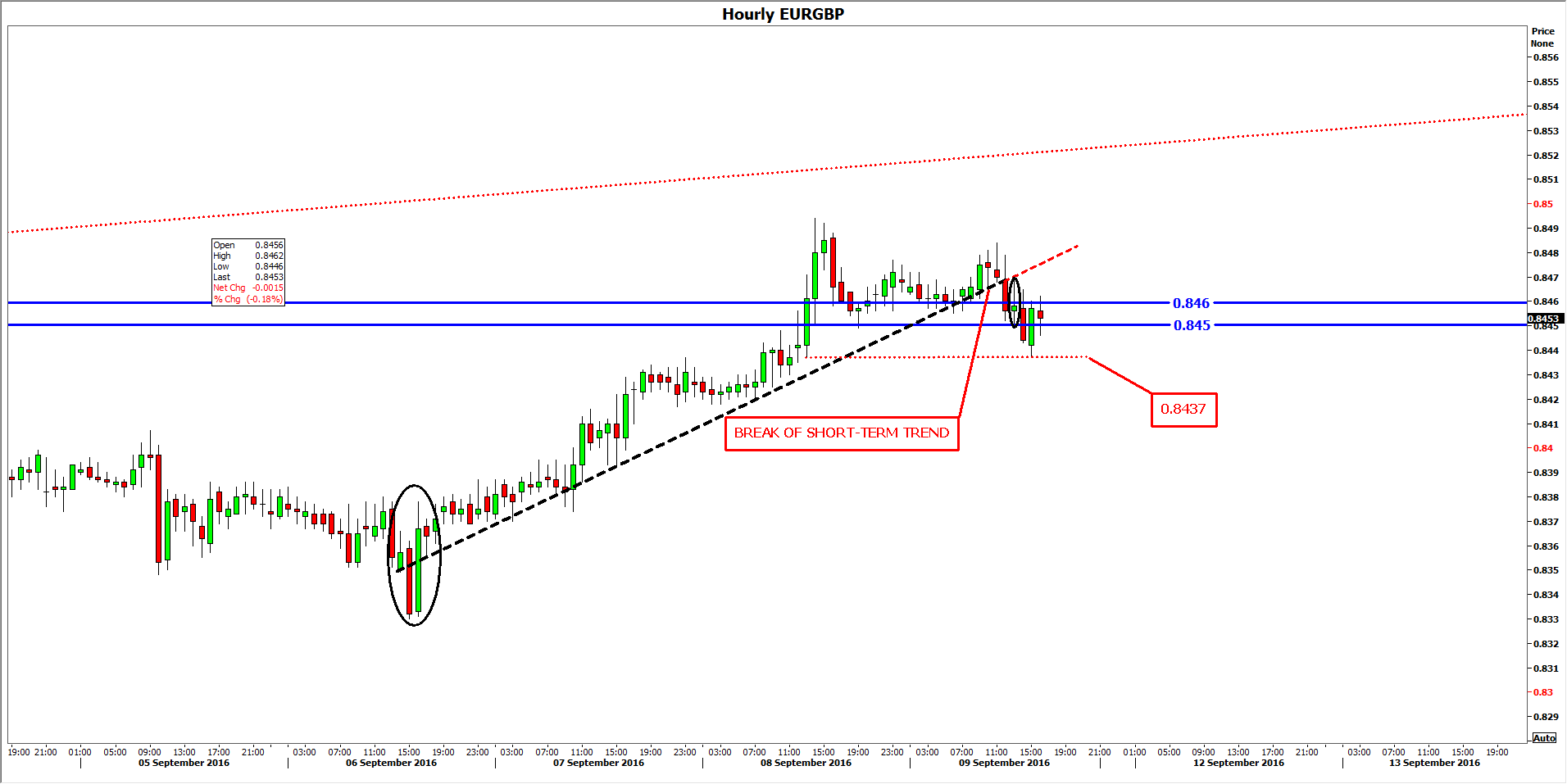

From a technical perspective, whilst we fully expect a further attempt by euro bulls to reinstate the 26th June-1st September ‘beggar-thy-neighbour’ post Brexit rising trend, we see chances of that happening as strongest when or if Britain’s economy can be shown to be weakening definitively.

For now, failure of the week’s hourly rising trend on Friday opens the way towards a conservative short-term target. We opt for the kicking-off point of this week’s attempted comeback. The hourly low that began the bounce was at 0.8330. For additional safety we limit our trade to that hour’s high at 0.8362.

Our stop is the likely point at which a sustained rebound would strike this week’s previous rising trend from underneath. The hourly high that immediately followed Friday’s breach of this week’s short-lived rise was 0.8470.

This bearish set-up is likelier to fail should the rate successfully push above the 0.845/6 support/resistance zone. A breakdown and perhaps confirmation from 0.8437 would improve the trade’s chances.