Boris Johnson’s hopes for a large majority that will enable the Tories to ‘get Brexit done look’ show signs of fading, with terrible timing for sterling. The earlier eye-catching dip suggests that persistent risks of an inconclusive outcome are nowhere near priced appropriately after the pound gained as much as 9% versus the dollar since August.

Still, sterling actually turned higher into the second half of Europe’s Wednesday session. A combination of profit taking after GBP/USD’s 114-odd pip drop from Tuesday’s near 9-month highs, plus pre-Fed statement caution probably accounts for easing pressure. Sentiment wafting back from the final day of campaigning might be playing a part, though it would be peripheral.

Wednesday’s most recent opinion poll, by Opinium looks a likelier prop. It showed the Tory-Labour gap was still narrowing, but the Conservatives were only down 1 point, at 45% with Labour up 2 to 33%. That points to a less drastic outcome than YouGov’s latest multi-level regression and “post-stratification” study. Conducted early this week, YouGov’s data crunch predicted a Conservative majority of 28, down from as much as 68 around a week ago

A broader look at UK assets shows that sterling and a relatively narrow group of domestically focused shares is still where the impact of any market upsets will be focused.

- Demand for sterling hedges and speculation has risen. The standard one-week ‘risk reversal’ option strategy shows bearish puts are favoured more than bearish calls by the most since 2016.

- The drop coincides with a FTSE 250 slide of 1.4%. The index is Europe’s worst-performer on Wednesday, on rekindled concerns over mid-cap companies’ greater exposure to sterling than those on the FTSE 100. Property shares remained the most sensitive sector to Brexit and election developments, with commercial property firms falling the hardest. Great Portland Street, workspace firm IWG and Hammerson fell 0.8% to 1%

- UK gilts tell a more nuanced tale. They have not priced the wave of optimism over a possible Conservative majority in the same way that sterling and other assets. 10-year yields continued to trade close to the top of their recent range on Wednesday afternoon, suggesting any safety-seeking sell-off won’t be drastic in the event of a market-unfriendly election outcome. 10-year gilt yields stood at 0.786% at the time of writing down one basis point on Monday’s close

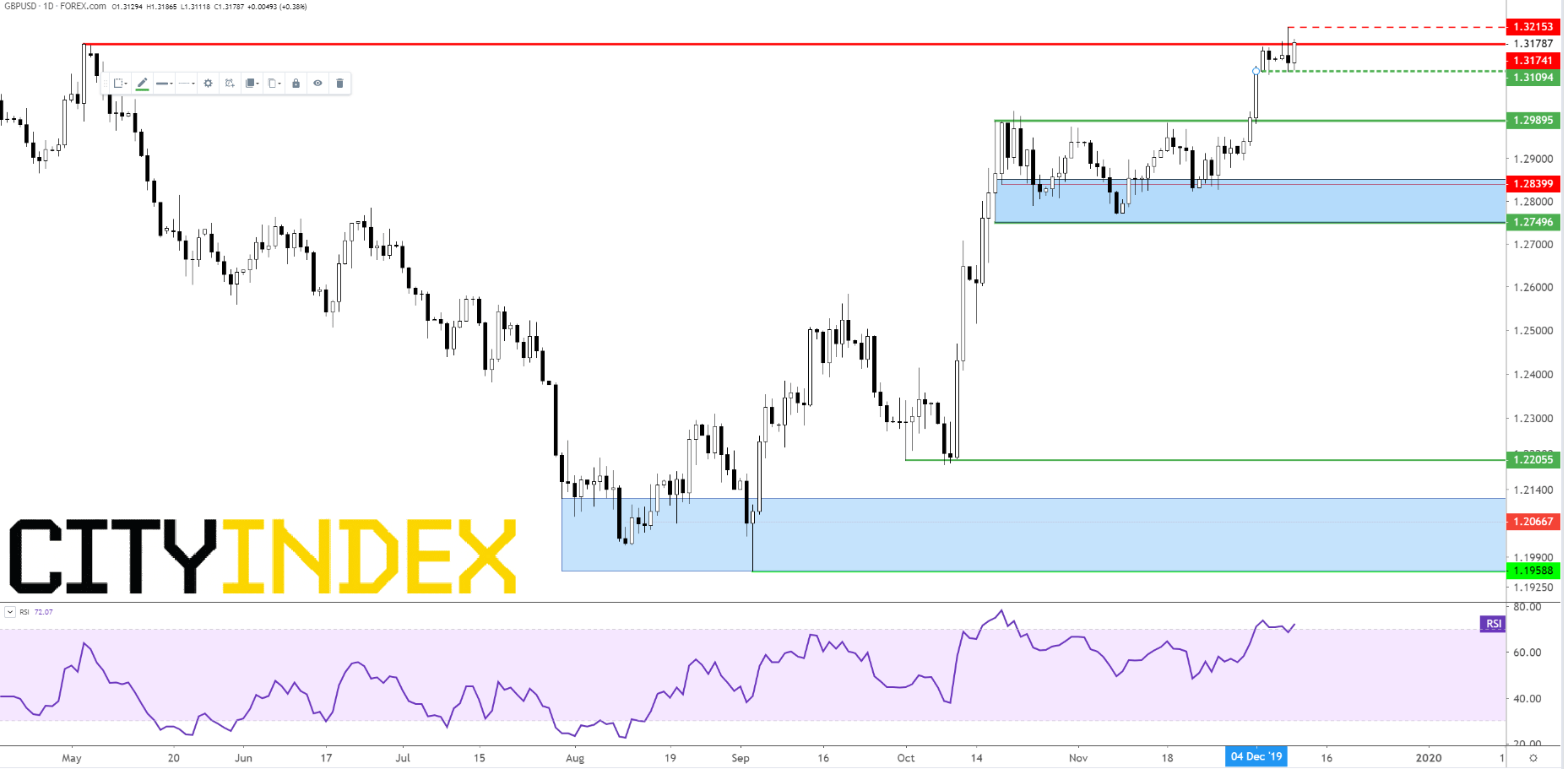

Chart points

GBP/USD’s chart is by no means ominous heading into the biggest sterling risk event of the year. Tuesday’s 1.32 top in context was a first attempt to break May’s $1.3174 high. The rate was marginally above it at last look. Assuming caution returns as the voting begins tomorrow morning, traders will rely on $1.3109, 4th December high and implied support as rough divider of market friendly or unfriendly outcomes. The news blackout that will begin tonight, after at least one further poll, may see the pound drift around current prices and $1.31s ahead of early exit polls on Thursday night. A drop below the next important support region largely referenced by 17th October’s $1.2989 high, would be the final verdict that Boris Johnson has failed to secure a viable majority. With lots of shades of grey in between, GBP/USD should still operate above late 1.29s in the case of a smaller majority than the Conservatives hope for, though the $1.338 March peak (not pictured) probably requires a solid win by the incumbents.

GBP/USD – Daily [11/12/2019 17:07:25]

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest GBP articles

April 3, 2024 02:49 AM

March 29, 2024 10:00 PM

March 9, 2024 04:00 PM

October 24, 2023 02:20 AM