Whatever the polls say, the pound will soon be under pressure

The pound continues to react to a downtick in Conservative support ahead of next month’s general election. An ICM/Reuters poll out on Monday put the Conservatives at 41%, Labour on 34% and the Lib Dems at 13%. The Brexit Party notched 4%. That compares with Kantar’s Tuesday poll showing the Conservative lead lengthening again, with a potential 43% of the vote vs. Labour’s 32%. Just over a week ago, the Tories polled as much as 45%, yet the 34% showing by Labour on Monday was their best since early October.

It’s a slight moderation of the recent trend that has seen the Conservatives consolidate a strong lead against Labour, raising the probability that the incumbent party could secure a Parliamentary majority. If that pattern played out in the election, a solid Tory win could pave the way for Commons approval of Boris Johnson’s Brexit deal, particularly given that all Conservative candidates signed a pledge to vote for it. Understandably then, with Labour narrowing the gap to the Tories in some polls, jitters are reappearing in sterling. It’s worth remembering that whilst an outright Labour win remains a distant possibility, a smaller gap between the parties points to a wider margin of error. Note polls have been notoriously unreliable in recent years. For sterling buyers, betting on hopes that an unblocked Brexit process could ease the UK’s economic malaise, the chief worry is that Labour could yet find themselves in a position to form a coalition government. Markets have traditionally been wary of prospective Labour governments, though there may be added of concern ahead of December’s election, given that the party envisages higher spending and tax rises than other contenders.

Sure enough, sterling’s 0.3% dip on Tuesday comes with convergent trimmings. These include a five-week high in sterling volatility implied by option contracts covering the four weeks. To be sure, there are questions about the timing of any relapse for the pound, after a ramp that stretched almost 9% from September lows to October’s $1.30 peaks. The significance of a poll lead that has narrowed by a few points over recent data points is also open to question. But with the toughest part of Brexit—EU trade negotiations—still ahead, and real UK yields negative in step with a weakening economy, there’s less doubt sterling buyers face an uphill struggle in the weeks and months to come.

Chart points

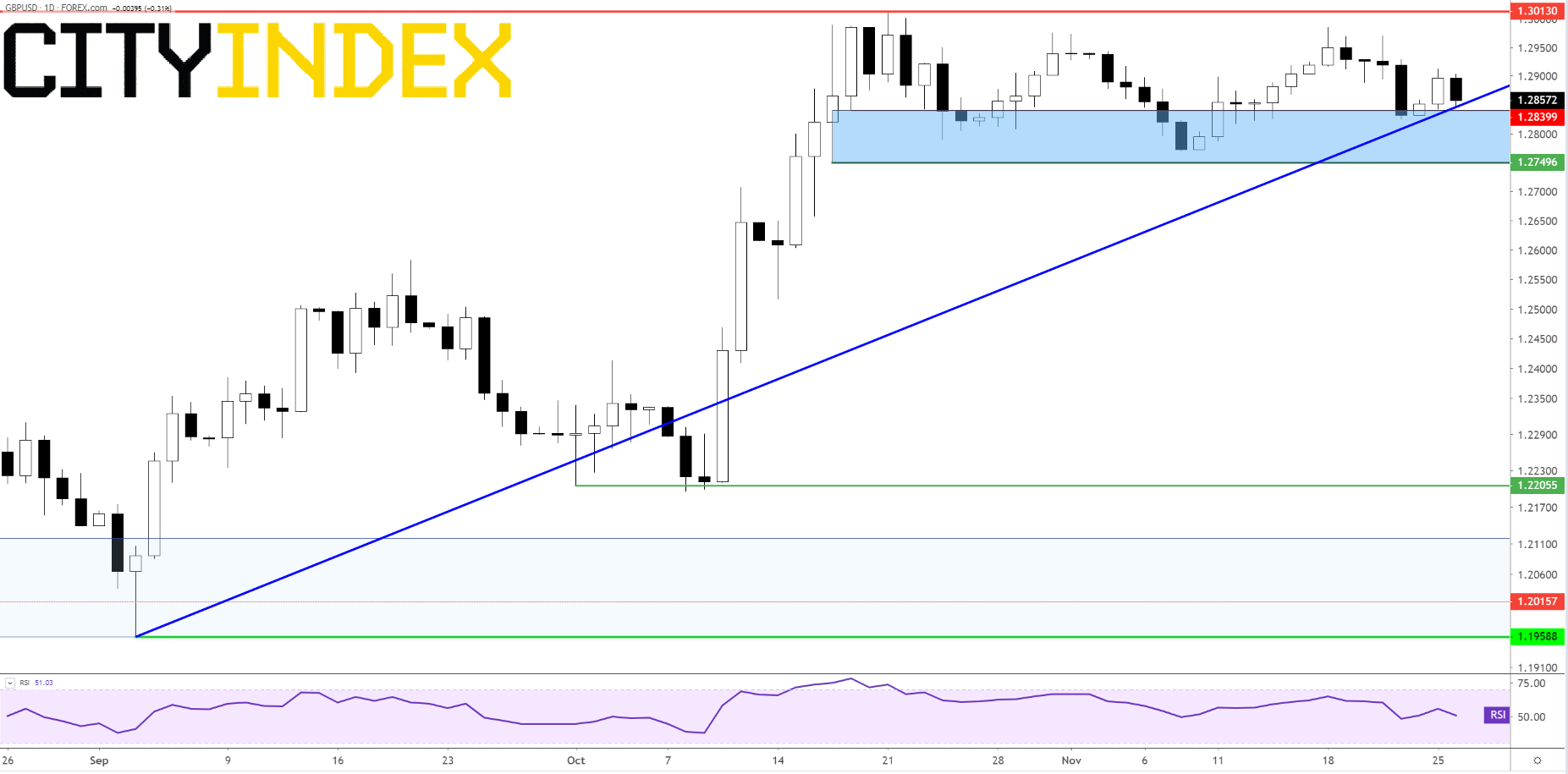

Following GBP/USD’s resurgent progress since September, its biggest potential upset on the charts is easy to spot. The market remains structurally short within close range of the psychologically charged $1.30 marker. As we head into the year’s main risk event, little wonder that offers have repeatedly dried up on approaches to that top. At the same time, GBP/USD’s muscular trend off 20-odd month lows could soon transform into a hinderance from a help. As triangulation tightens into December, the Tories will need to hit Labour for six if GBP/USD is to avoid breakdown below the $1.285-$1.275 support structure.

GBP/USD – Daily [26/11/2019 14:35:45]

Source: City Index

Latest market news

April 25, 2024 03:09 PM

April 25, 2024 03:00 PM

April 25, 2024 01:12 PM

April 25, 2024 11:14 AM

Latest Forex articles

April 24, 2024 03:14 PM

April 24, 2024 11:00 AM

April 23, 2024 11:09 PM