Sterling aims higher pre inflation jobs and Carney

The Tumultuous Trinity of the pound, the Bank of England and inflation will be back in focus on Tuesday.

The Tumultuous Trinity of the pound, the Bank of England and inflation will be back in focus on Tuesday.

BoE Governor Mark Carney appears before Parliament’s Treasury Committee, half an hour after a Consumer Price Index update (9.30 GMT).

For only the second time in many years, the Inflation Report Hearings will have a significant amount of that quality on hand as grist for the discussion, the aftermath of Britain’s shock devaluation.

At the same time, sterling’s revival following a summer and autumn of economic, political and financial mayhem is being as welcomed by the political class as it is by investors, though a measure of trepidation is just as present in Westminster as in the City, given ambivalent reasons for the pound’s bounce.

Strategists were keen to sell sterling’s quasi ‘safe-haven’ story at the end of last week, though few could shrug off the irony of a Brexit–battered pound playing that role amid another anti-establishment shock.

It’s still clear to all that exchange rates remain the clearest financial signifier of a splintering EU and uncertainty in its wake.

After all, Westminster, The City and indeed consumers themselves are wary of the day when price rises hit harder than has been seen so far, with a few high-profile but relatively trivial items becoming pricier (Marmite; Toblerone; Walkers Crisps).

And, in keeping with the new era of shifting political and economic sands, Carney and his fellow BoE policymakers have had to change trains since unleashing a barrage of measures in the summer to prevent an economic confidence shock.

A more resilient than expected economy scuppered plans for a deeper interest rate cut and instead the governor was forced to warn that the next move could be either up or down.

For the moment, that is likely to remain the extent of Carney’s willingness to forecast the rate path.

With inflation growth widely expected to pause in October after the rate surged to a two-year high in September, the governor will probably have little more to offer on that front either.

The BOE said it foresaw 2.5% in late-2019, the biggest three-year overshoot ever predicted.

However, we expect Mr Carney’s typical eloquence, erudition and even-handedness, to be his only answer for now.

As inflation pressures build and economic compression deepens in coming months (and years) such questions and answers will grow more strident.

But it is still likely to be some time before economic readings, like inflation and labour market data, due on Wednesday (9.30 GMT) deteriorate and pile on that pressure.

In turn, the pound can be expected to continue its recovery, albeit with further volatile eruptions (see flash crash) of the kind that accompany economic, political and financial paradigm changes like Brexit.

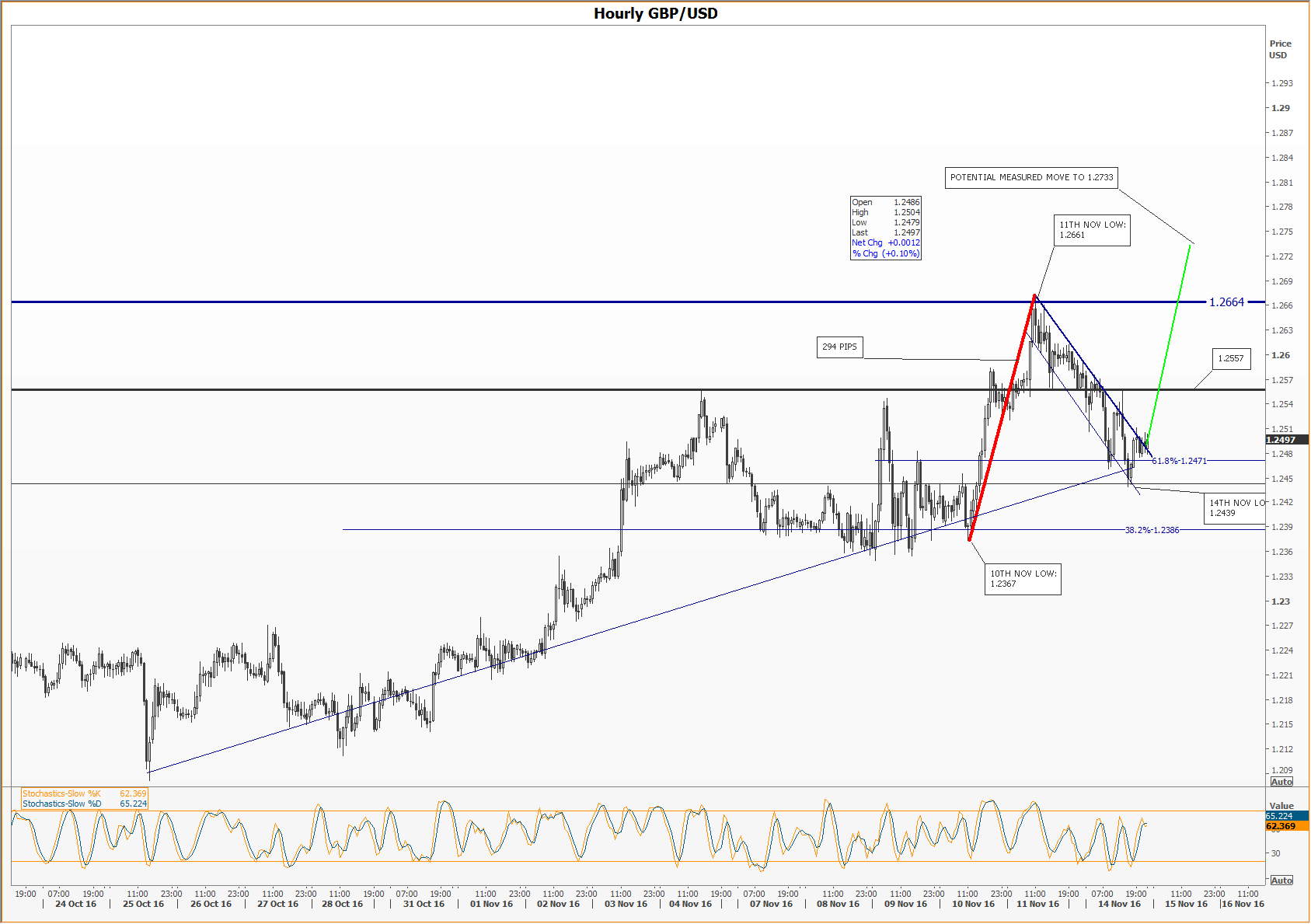

From a technical point of view, the recuperation of sterling against the dollar from flash crash lows has continued for well over a month.

However, U.S. ‘election outcome volatility’ at the end of last week magnified a challenge for cable, when it attempted to match highs ($1.2664) coinciding with the last ‘bid’ hour of the evening before 7th October’s dump.

It makes sense to expect stops to remain peppered around the vicinity.

At the time of writing though, cable was looking to break beyond the better edge of a pennant formed following last week’s failure at the high mentioned above, and the rate was eyeing support-turned resistance along $1.2557.

Should the tacit signal from this week’s British economic data be read as providing no further impediment for sterling in the near term, a further attempt at $1.266 looks probable.

Such a move would also aim to complete a bullish pennant continuation pattern.

That theoretical measured move would match the impulsive run from a 10th November hourly low ($1.2367) to the 11th November $1.2661 high, some 294 pips.

If realised, cable would certainly break troublesome resistance at $1.2664, and then some.

However if GBP/USD runs out of steam at current rates or even at $1.2557, a further test of lows on the day after the U.S. election ($1.2365-$1.2367) will be the first stop.

Please click image to enlarge