Sterling again the M amp A trade

The FX markets have traded in extremely tight ranges again overnight despite a rebound in Asian equities as investors await the next developments from Ukraine. […]

The FX markets have traded in extremely tight ranges again overnight despite a rebound in Asian equities as investors await the next developments from Ukraine. […]

The FX markets have traded in extremely tight ranges again overnight despite a rebound in Asian equities as investors await the next developments from Ukraine.

It was a national holiday in Russia yesterday so the political turmoil could well return today.

The BoJ maintained its current policy, while sending a cautious vibe on exports – sighting demand – as most investors now look to the effects on the Japanese economy from further increases in sales tax due to start in April and what potential policy change could subsequently be implemented.

The AUD came under some pressure following a weak business confidence survey from the NAB, which revealed business conditions at 0 from the previous reading of 0.5.

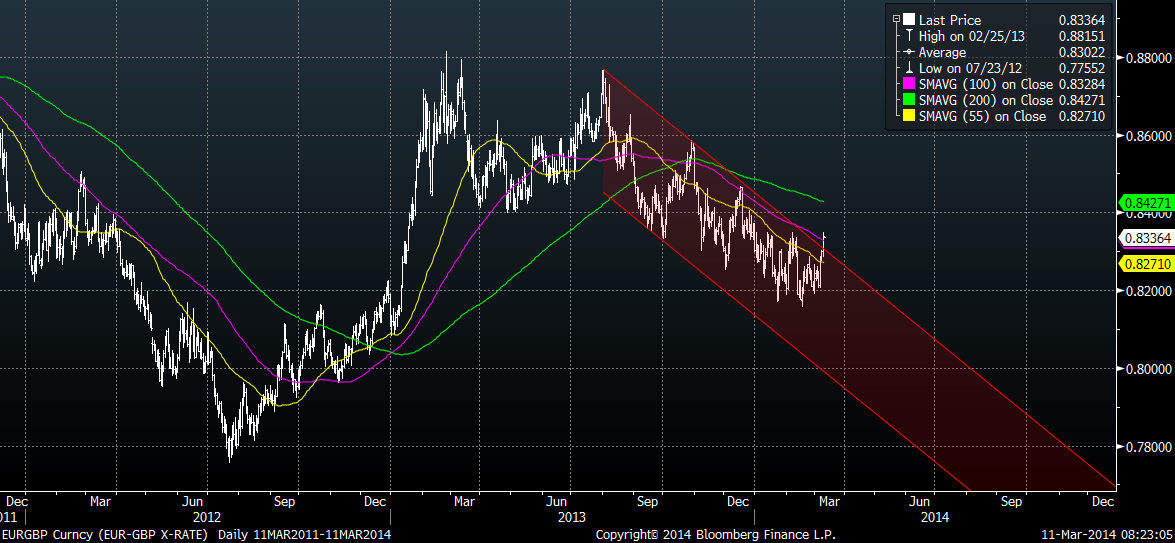

Eur/USD stands out as the outperformer this week as the pair break resistance levels at 0.8315 and 0.8330, which brings the 200-day moving average into focus at 0.8427.

The demand for the pair derives from speculation regarding acquisitions; with Vodafone rumoured to have an interest in European telecommunications company, Ono, while Daimler has been sighted as potential suitor for the British car manufacturer, Rolls Royce.

The only data of note comes this morning in the form of UK industrial and manufacturing production.

![]()

![]()

EUR/USD

Supports 1.3825-1.3780-1.3705 | Resistance 1.3920-1.3980-1.4000

![]()

![]()

USD/JPY

Supports 103.15-102.85-102.20 | Resistance 103.45-103.80-104.25

![]()

![]()

GBP/USD

Supports 1.6605-1.6580-1.6540 | Resistance 1.6710-1.6775-1.6825