Spirent shares get real after profit warning

Spirent Communications Plc., a telecom testing firm, warned that weak trading conditions in the US and China would hamper third-quarter revenue. Spirent’s FTSE 250-listed stock […]

Spirent Communications Plc., a telecom testing firm, warned that weak trading conditions in the US and China would hamper third-quarter revenue. Spirent’s FTSE 250-listed stock […]

Spirent Communications Plc., a telecom testing firm, warned that weak trading conditions in the US and China would hamper third-quarter revenue.

Spirent’s FTSE 250-listed stock has plunged 21% today, its biggest fall in a decade and the biggest percentage faller on the London Stock Exchange.

Spirent said it expected marginal revenue gains for the third quarter following persistently lacklustre business conditions in the United States and China.

Spirent’s customers include such telecommunications and telecom equipment makers as Cisco Systems Inc. and Nokia for which it tests Ethernet networks, 3G and 4G wireless networks to international standards.

It said third-quarter revenue was now seen below $110m compared with Q3 revenue of $107.7m reported for the same time period a year ago.

Spirent attributed the expected slowdown in its revenue stream to mergers and takeovers amongst its customers and spending delays.

“Demand levels dipped sharply as a result of merger activity and delays in capital expenditure as future new technology deployments are being assessed in areas in which Spirent has increased its investments,” the company said a statement.

Spirent did not specify which merger activity is affecting its sales.

However, given its biggest customer to date has been US telecom conglomerate AT&T Inc., which recently bought satellite TV firm DirecTV for $49bn, it seems sensible to assume Spirent was referring AT&T.

It follows AT&T would be pressuring many of its suppliers in the forthcoming quarters in the same way it may be pressuring Spirent.

The UK-based firm’s networks and applications business, its largest division by revenue last year, was expected to suffer the most impact from the revenue crunch, Spirent said.

Spirent received over 50% of its revenue from the United States in 2013 and around 35% from the Asia Pacific region.

Its fourth-quarter revenue would be between $120m and $125m compared with $115.4m in 2013, the company said.

In delving deeper into the trend of Spirent’s recent business, two clear strengths and two clear weaknesses emerge.

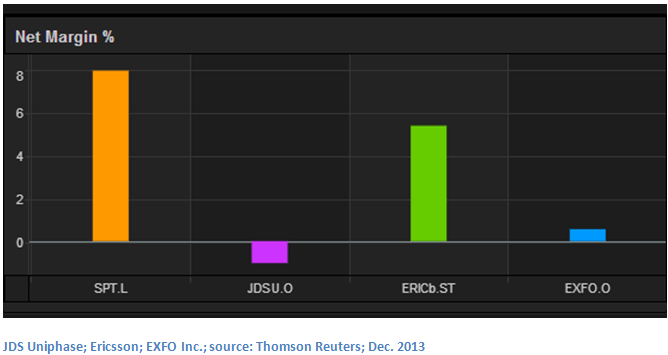

The five-year historical growth rate of Spirent’s earnings per share appears to lag the average of sector peers by at least four percentage points, whilst revenues were $413.5m, sharply lower than its main sector competitor, JDS Uniphase Corp.’s $1.7432bn in the year ending 31st December 2013.

An implied relatively slower-rate of growth, if confirmed, can often be an indicator that strategic focus or execution differs between a company and its peers to an extent that might be material.

With return on assets having declined from above median to about median over the last five years, Spirent’s relative operating advantage may be in question.

Spirent appears to have zero debt.

Coverage of 2.73 times the latest reported dividend per share of 4 cents appears more than adequate

Overall, would it be unfair to judge Spirent currently as a steady player in an unsteady operating environment?

It surely ought to have moved faster to diversify its customer base to the extent that one major client being called into question did not have such a glaring impact on revenue.

On the other hand with no debt, and good dividend coverage (albeit weaker-than-market median yield) there should be no immediate crisis.

It appears that following a successful turnaround in the firm towards the end of the last decade, the stock price got way, way ahead of itself.

(I suspect the removal of some rivals, like Teledyne Lecroy Inc. and Keithly Instruments Inc., from the listed market place over the last five years, bolstered Spirent’s investment case by default.)

The ten-year average price-to-earnings ratio of 19 times simply doesn’t match the earnings growth rate over the same period in aggregate and would only make sense on the expectation Spirent might have been acquired.

Though there have been relatively sound reasons for such a high multiple over the years.

For instance, whilst annual net income after tax has been volatile since a post-restructuring peak of $90.7m in December 2009 to $32.7m in December 2013, Spirent’s net margin at the end of last year was comfortably above a selection of its close peers.