Spain upgraded peripheral spreads plunge euro firms

Fitch has upgraded its rating on Spain’s sovereign bonds by one notch to BBB+, on the basis of a forecast that government debt will peak […]

Fitch has upgraded its rating on Spain’s sovereign bonds by one notch to BBB+, on the basis of a forecast that government debt will peak […]

Fitch has upgraded its rating on Spain’s sovereign bonds by one notch to BBB+, on the basis of a forecast that government debt will peak within two years.

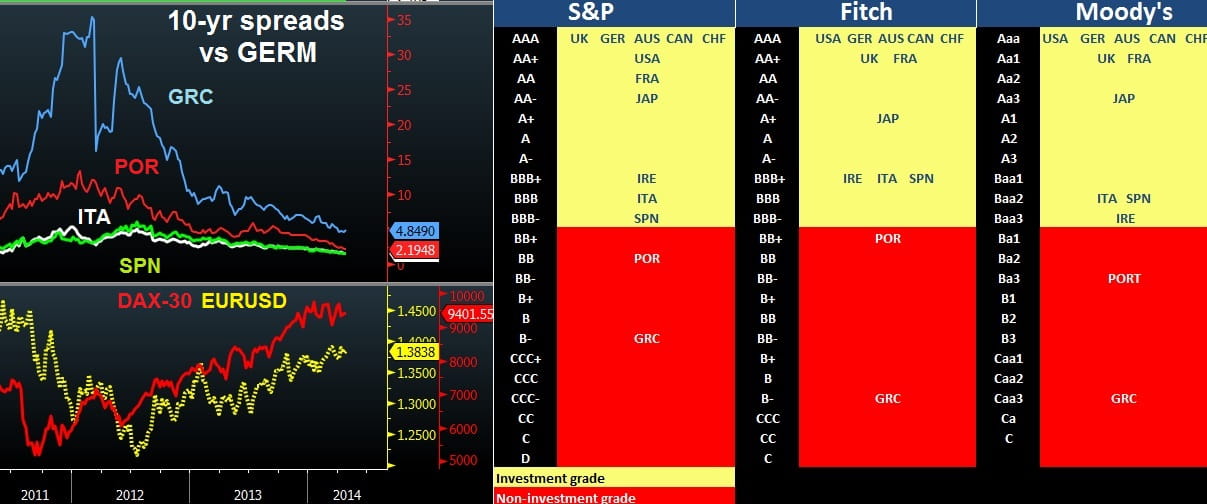

The BBB+ rating joins the rank of Italy and Ireland and emerges 2 months following Moody’s upgrade of Spain to Baa2, but remains comparably lower than that by Fitch. Standard & Poor’s maintains its BBB- rating on Spain, which is not only the lowest for Spain among the three major agencies, but also the lowest within in the investment grade category.

This leaves Greece and Portugal in ‘junk’ territory rating by all 3 credit agencies, with set to return to the capital markets when its €78bn bailout program ends next month.

The 58% decline in Spain’s 10-year yield from their 2012 highs to a record low of 3.1% is part of a Eurozone-wide improvement in government paper, prompting credit agencies to upgrade their sovereign outlooks. In the year when Ireland, Portugal and Greece have all regained access to global bond markets, Spain is continuing to tap the markets in 3 and 10-year bonds, with €5.6bn raised this past week.

Earlier in the week, Madrid revealed a 0.4% increase in Q1 GDP growth, the fastest pace in six years and twice the level of Q4.

Such measures are agreed upon by the economics ministry as well as the central bank. Chronic unemployment has not stabilised, but cost of bank debt has halved over the past two years to the extent that bad loans at the Spanish banks have finally begun to fall. The charts below show the plunge in peripheral bond spreads, which emerged in tandem with the recovery in the euro and global equities following Draghi’s speech proclaiming the euro “irreversible” and backing it with a 2nd LTRO operation, further bolstering Eurozone banks’ access to capital with 5-6 basis points worth of carry trades.

These above dynamics certainly do not lift Greece out of the burden of prolonged austerity, or shed clear light on the policy rout of Italy’s new Prime Minister. But they certainly put GDP growth back in the green, improve banks’ capital and reduce the need to raise USD-funding, thereby normalizing EUR-spreads vs. UK to the benefit of stabilization in the euro. And since our objective is to make calls on prices of currencies (rather than simply ruminate on the long term merits and challenges of currency unions), the course for a robust EURUSD rate shall remains as long as US interest rates are not sufficiently priced to account for higher US inflation. And as long as the euro panic in capital markets has been left behind, it remains difficult for the ECB to make the case for negative interest rates.