July 17, 2019 1:44 AM

Pre FOMC nerves on display as overnight events conspired to leave traders deeply divided over whether the Fed will cut by 25bp or by 50bp at their upcoming July 31st FOMC meeting.

Commencing proceedings, an unambiguously strong U.S. retail sales number for June. The retail control measure (ex-autos, gasoline, building materials) printed at +0.7%, well above consensus expectations of a +0.3% gain. The June number was accompanied by upward revisions to previous months numbers, the result of which will be upside revisions to U.S. Q2 GDP forecasts.

In more normal times, evidence of robust consumer spending coming hot on the heels of stronger than expected Non-Farm Payrolls, CPI and PPI data would prevent any thoughts of a rate cut entering traders’ minds.

However, we live in unusual times and ahead of Pre FOMC blackout period which begins this weekend a host of Fed speakers hit the wires overnight to emphasize this. Perhaps the most notable comment was from Dallas Fed President Kaplan who just three weeks ago argued against an immediate rate cut, stating he is now open to a “tactical adjustment” in the form of a “modest, restrained, limited move”.

Keeping the pressure on both the Fed committee and China, U.S. President Trump warned that he could impose more tariffs on China “We have a long way to go as far as tariffs where China is concerned if we want. We have another $325 billion we can put a tariff on.” Little wonder then why there remains 31 bp of cuts priced for July and why S&P500 traders elected to take some profits off the table.

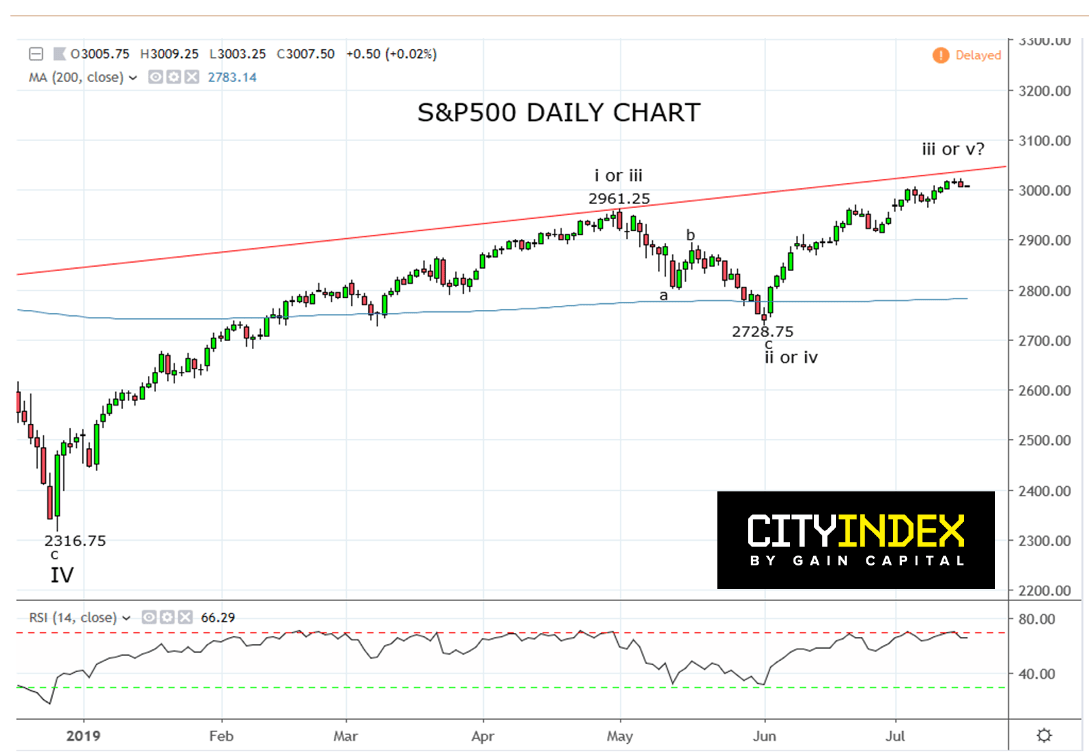

Technically the S&P500 has stalled from ahead of the critical 3030/3050 resistance area, highlighted in recent reports and which comes from the broken uptrend line, from the 2016 1802, low.

While it is possible that the S&P500 is in the early stages of a fourth consecutive rejection and breakdown from the broken uptrend line, more evidence is required. That evidence would be a break and close below the May 1st, 2961 high. Until then, a retest and push above 3030/3050 cannot be ruled out.

Source Tradingview. The figures stated are as of the 17th of July 2019. Past performance is not a reliable indicator of future performance. This report does not contain and is not to be taken as containing any financial product advice or financial product recommendation

Disclaimer

TECH-FX TRADING PTY LTD (ACN 617 797 645) is an Authorised Representative (001255203) of JB Alpha Ltd (ABN 76 131 376 415) which holds an Australian Financial Services Licence (AFSL no. 327075)

Trading foreign exchange, futures and CFDs on margin carries a high level of risk and may not be suitable for all investors. The high degree of leverage can work against you as well as for you. Before deciding to invest in foreign exchange, futures or CFDs you should carefully consider your investment objectives, level of experience, and risk appetite. The possibility exists that you could sustain a loss in excess of your deposited funds and therefore you should not invest money that you cannot afford to lose. You should be aware of all the risks associated with foreign exchange, futures and CFD trading, and seek advice from an independent financial advisor if you have any doubts. It is important to note that past performance is not a reliable indicator of future performance.

Any advice provided is general advice only. It is important to note that:

- The advice has been prepared without taking into account the client’s objectives, financial situation or needs.

- The client should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation or needs, before following the advice.

- If the advice relates to the acquisition or possible acquisition of a particular financial product, the client should obtain a copy of, and consider, the PDS for that product before making any decision.