May 17, 2019 1:02 AM

U.S. equity markets commonly follow two seasonal patterns each year. The first of which is “Sell in May and go away”. The second is the Santa Clause rally, which usually results in stocks rallying from mid-December into the first months of the New Year. Last year, the Santa Claus rally started a few weeks later than usual. However, it was very much a case of “better late than never” following a -20% fall in the S&P500.

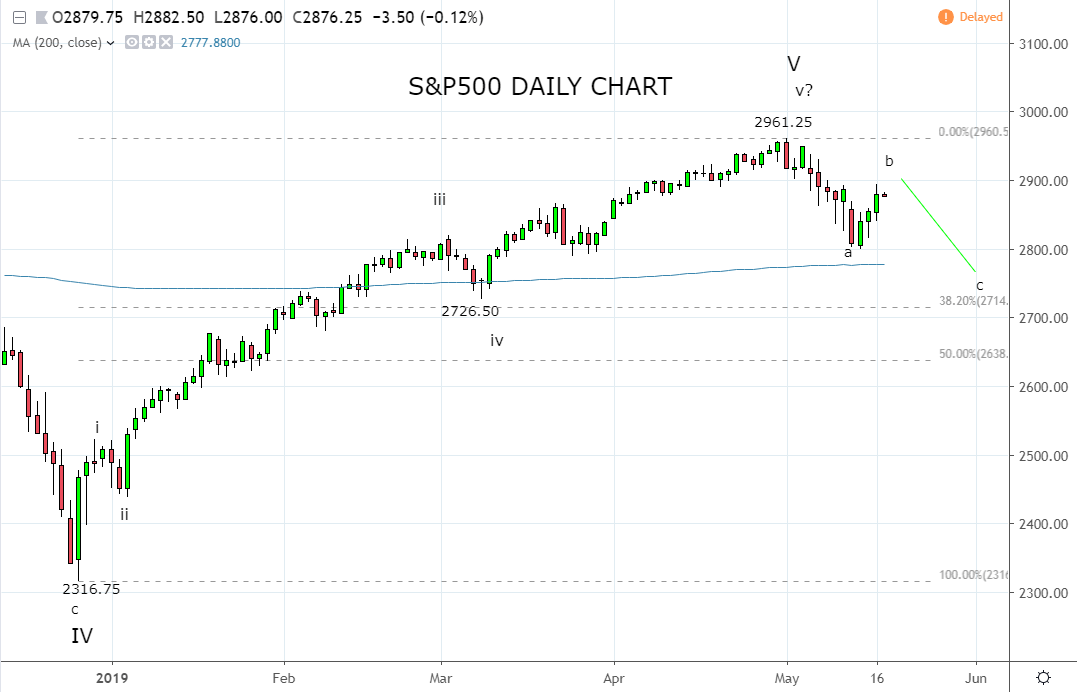

No such timing issues this month, as the S&P500 made a new cycle high on May 1st, before falling almost -5.5%. The decline of course exacerbated by tweets from President Trump which confirmed that U.S. – China trade talks were not progressing as hoped for and tariffs would be increased on U.S. $200 billion of Chinese imports.

This week the S&P500 has recovered about 50% of its May losses, supported by hopes the Federal Reserve would cut interest rates to support the economy and optimism that talks with China were back on track. Thus, prompting the question has the May seasonal effect come and gone for another year and is the S&P500 set for new highs?

In terms of the May effect, it is possible. The magnitude of the recent -5.5% fall is within the range of what to expect. In terms of timing, on average, a low is typically put in place at the end of the third week of May. Despite this, I am not convinced the S&P500 is immediately destined for new highs.

As U.S. investment bank JP Morgan outlined in a recent note on the Trump administrations behaviour, “The market moving higher generally leads to a hardened stance and more confrontational tone, and the market moving lower generally leads to either verbal or actual progress towards trade resolution.” After a three-day rally in the S&P500, the timing of last night’s announcement aimed at curbing telecom sales from foreign entities fits this pattern.

In summary, while the May effect could well be over for another year, markets continue to be driven by the game of brinkmanship being played out between the U.S. and China. As such, the topside in the S&P500 is likely to be limited for now as is the downside.

Source Tradingview. The figures stated are as of the 17th of May 2019. Past performance is not a reliable indicator of future performance. This report does not contain and is not to be taken as containing any financial product advice or financial product recommendation

Disclaimer

TECH-FX TRADING PTY LTD (ACN 617 797 645) is an Authorised Representative (001255203) of JB Alpha Ltd (ABN 76 131 376 415) which holds an Australian Financial Services Licence (AFSL no. 327075)

Trading foreign exchange, futures and CFDs on margin carries a high level of risk and may not be suitable for all investors. The high degree of leverage can work against you as well as for you. Before deciding to invest in foreign exchange, futures or CFDs you should carefully consider your investment objectives, level of experience, and risk appetite. The possibility exists that you could sustain a loss in excess of your deposited funds and therefore you should not invest money that you cannot afford to lose. You should be aware of all the risks associated with foreign exchange, futures and CFD trading, and seek advice from an independent financial advisor if you have any doubts. It is important to note that past performance is not a reliable indicator of future performance.

Any advice provided is general advice only. It is important to note that:

- The advice has been prepared without taking into account the client’s objectives, financial situation or needs.

- The client should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation or needs, before following the advice.

- If the advice relates to the acquisition or possible acquisition of a particular financial product, the client should obtain a copy of, and consider, the PDS for that product before making any decision.

Latest market news

Yesterday 01:23 PM

Yesterday 06:01 AM

April 18, 2024 11:27 PM

April 18, 2024 04:46 PM