Smiths Group lags sector as profit slides

Smiths Group, one of the UK’s preeminent engineering conglomerates, said annual profits had slumped marking the firm out as a weak link in a sector […]

Smiths Group, one of the UK’s preeminent engineering conglomerates, said annual profits had slumped marking the firm out as a weak link in a sector […]

Smiths Group, one of the UK’s preeminent engineering conglomerates, said annual profits had slumped marking the firm out as a weak link in a sector that’s currently strengthening.

Smiths said full-year operating profit was 10% lower to £504m for the full year ended 31st July from £560m the year before, with particularly weak performance from its medical devices and security detector units. Revenues edged 5% lower to £2.9bn.

Margins in the Smiths Detection unit softened by 4.8% against 10.4% the year before, the group said, due to lower volumes, additional costs and working capital adjustments, according to Smiths Group.

The unit is heavily dependent on government customers like US Department of Defense, US Transportation Security Administration and the UK Ministry of Defence. These customers are known to have reduced spending on security equipment.

As for the medical devices business, Smith’s second largest revenue generator, the margin ebbed to 19.8% compared with 22.2%.

The firm said it remained cautious about healthcare and the state security markets as both sectors were subject to continuing government funding constraints.

The firm, which in July marked 100 years of being listed on the London Stock Exchange, said the relative strength of the pound during its full year had been an additional weight on earnings.

Smiths Group creates as much as 95% of its revenues outside of the UK and so these can be subject to severe translation effects during periods of relative sterling strength.

Whilst the relative strength of sterling has been reported as a potential revenue threat by all of Britain’s major industrial engineers, the majority of the biggest players have appeared to avoid the worst effects due to the compensatory effects of resurgent construction markets in the US and UK.

Two of Smith Group’s FTSE 100-listed industrial engineering peers, Ashtead Group Plc. and IMI Plc., have reported strong revenues and profits up to the middle of the financial year.

By contrast, Smiths seems to have more numerous and persistent challenges than UK engineering firms of comparable size.

In March the company said it would continue its restructuring programme and said it expected to save £60m annually, up from the £50m it forecast earlier. Perhaps Smiths has merely been unfortunate to be undergoing a revamp during a period when it ought to have been firing on all cylinders.

Or perhaps the restructuring might need to progress faster.

For instance, the company’s medical and detection equipment manufacturing units have been troublesome for at least a year with particular turmoil in the detection business.

In October last year, Smiths announced the president of Smiths Detection was stepping down for personal reasons. The group’s information technology chief took over on an interim basis, but Smiths did not appoint a permanent head of the group until April 2014.

Today, Smiths Group’s CEO, Philip Bowman has indicated the firm is not looking to sell Smiths’ Medical business, despite the firm’s continuing caution about the outlook for the sector.

Bowman also stated Flex-Tek, a provider of heating and hydraulic components, subject of similar speculation, was not for sale. There was no mention of the detection business.

Smiths’ on-going restructuring drive may help account for relative signs of weakness in its financials, with its 86.8% gearing on a trailing debt-to-equity basis, putting it way ahead of its peers’ median of 56.9%.

With the company today announcing an increased dividend of 40.25p per share from 39.5p per share last year, attention may also fall on Smith’s below-peer group average dividend coverage for the last 12 months of 8.2, versus the 22.7 median of its close peers.

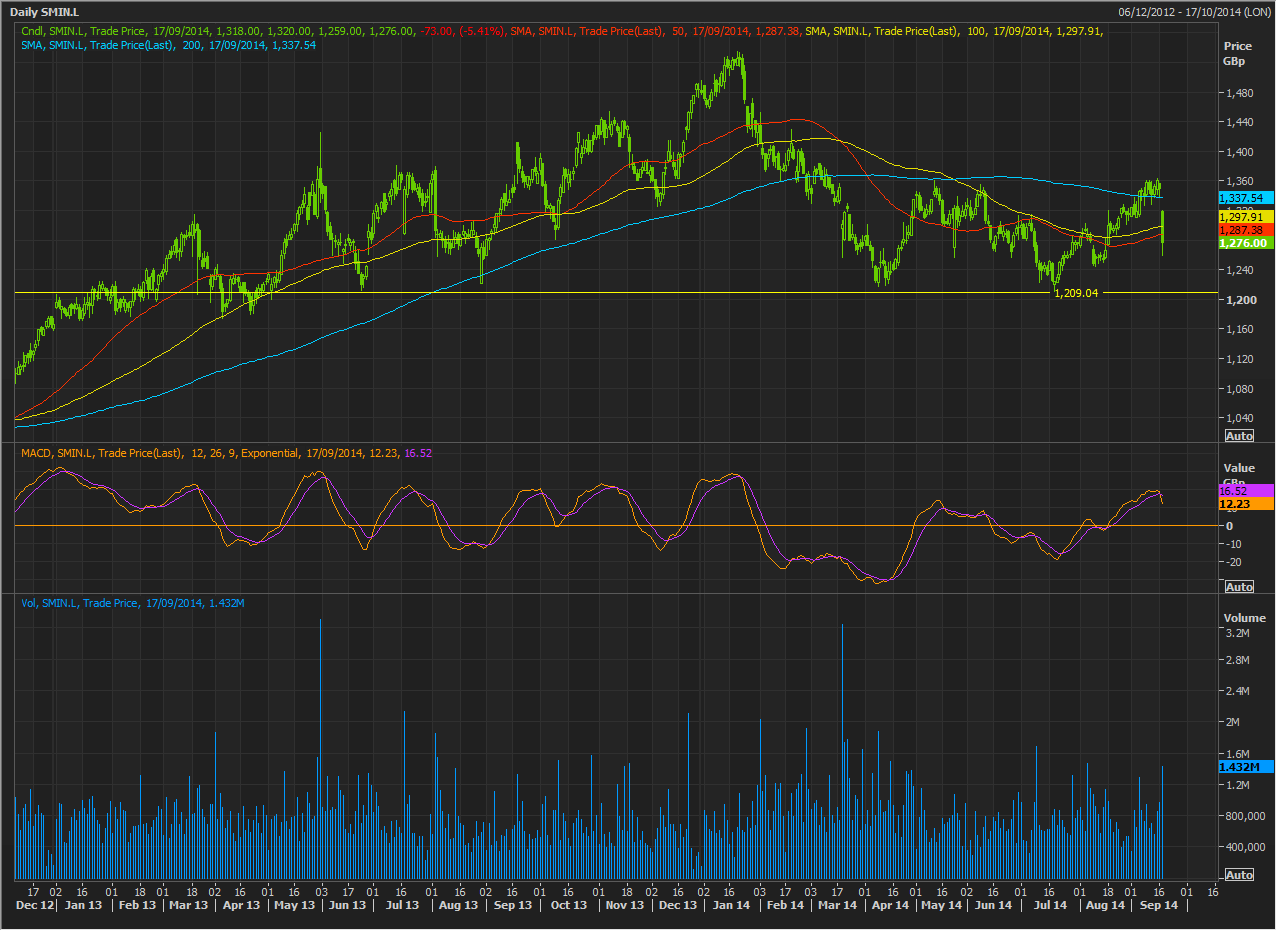

Smith’s Group stock has slumped as much as 6.6% today.

Even so, these multiples argue for reconsideration of the stock’s rating after a 5% advance over the last month before Tuesday’s close.

Smiths’ price-to-earnings ratio of 15.2 times prospective earnings represents a near-record multiple for the firm.

The stock chart corroborates the view that it’s too early to call a rebound in the firm’s operations, in the same way it looks too early for the stock to stray too far from a long-term support area close to 1209.04p.