Shire party is over

Shire Plc. shares tumbled 28% right out of the gate on Wednesday after AbbVie Inc. the US bio-pharmaceutical giant said overnight it would re-consider its […]

Shire Plc. shares tumbled 28% right out of the gate on Wednesday after AbbVie Inc. the US bio-pharmaceutical giant said overnight it would re-consider its […]

Shire Plc. shares tumbled 28% right out of the gate on Wednesday after AbbVie Inc. the US bio-pharmaceutical giant said overnight it would re-consider its $54.5bn takeover of the Ireland-based company.

Chicago-based AbbVie announced late on Tuesday it would hold a board meeting to discuss the recommendation that shareholders vote in favour of the deal with Shire.

“AbbVie’s board will consider, among other things, the impact of the US Department of Treasury’s proposed unilateral changes to the tax regulations announced on September 22, 2014, including the impact to the fundamental financial benefits of the transaction”, AbbVie said in a statement.

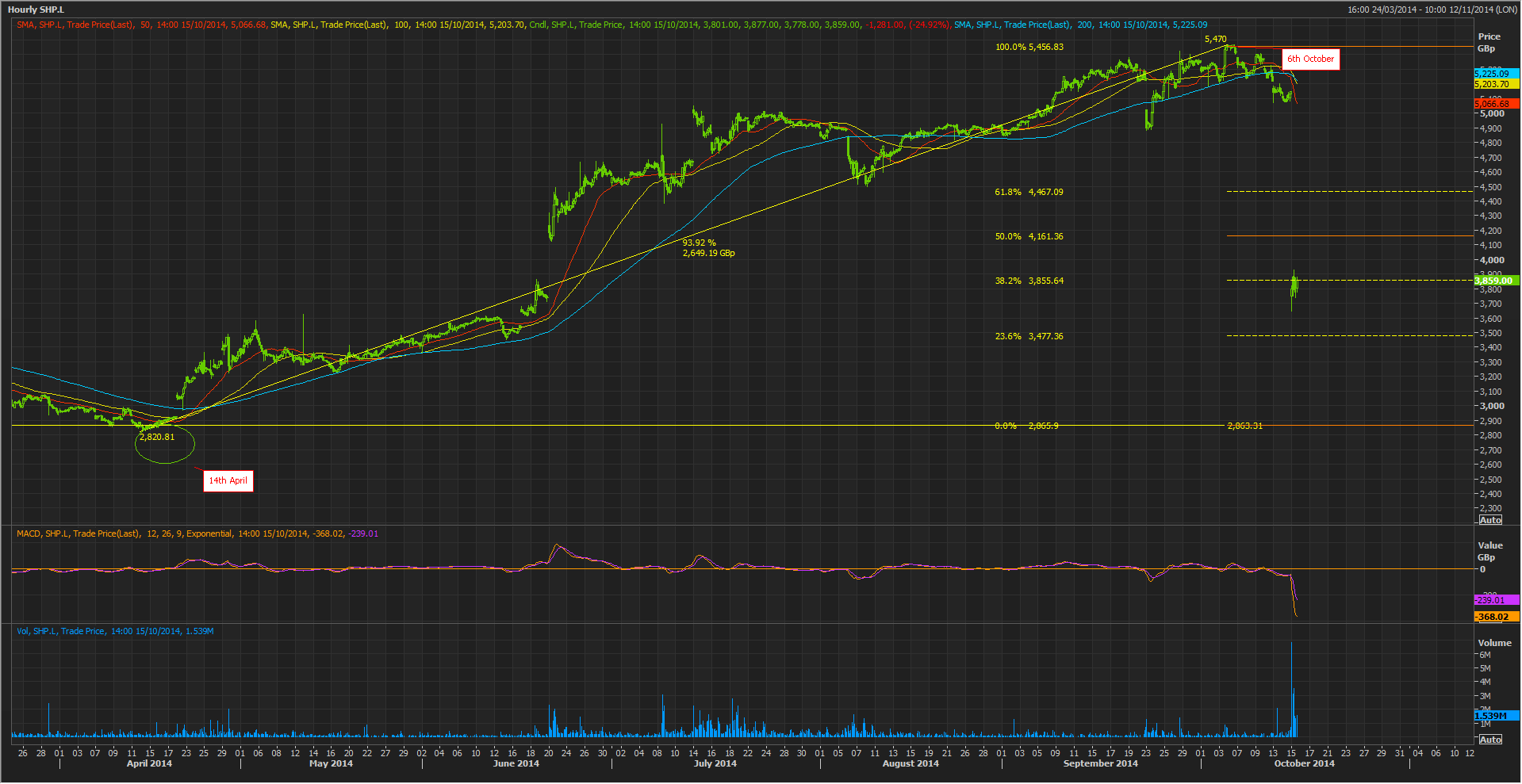

The news is an obvious blow to Shire shareholders, who have seen their stock climb 93% since mid-April.

The writing ought to have been on the wall though after US Treasury officials took steps to curb “inversion” deals through which US firms sought to escape high US taxes, although AbbVie sought to reassure all involved in the mooted transaction that it would go ahead, despite the rule changes.

It was only two weeks ago AbbVie’s CEO Richard Gonzalez sent a letter to Shire employees proclaiming he was “more confident than ever about the potential of our combined organizations”.

This was after insisting in July AbbVie wasn’t buying Shire “just for the tax impact”.

It’s fair to say most observers took that notion with a pinch of salt.

The taxation benefits for AbbVie would theoretically be significant, given the company’s own estimation that the deal would reduce its tax rate to 13% from 22%.

It should be born in mind though AbbVie is the result of a de-merger from its former owner Abbot Labs, in October 2011.

During the first few years of its existence its average tax rate has been much closer to the stated beneficial rate it would get after buying Shire.

The more significant benefit for AbbVie from the deal would be that the US firm would be free to spend offshore cash, without having to remit 35% to the US tax authority (IRS).

Obviously, the chances of the deal going forward now have fallen.

Still, since it’s the US Treasury’s tax rule changes which have given AbbVie’s pause for thought, let’s look at these new rules in a little detail.

When the measures were announced by US Treasury Secretary Jack Lew in September, he said he expected the “initial steps”, to “make companies think twice” before carrying out inversions.

“For some companies considering deals, today’s actions will mean that inversions no longer make economic sense,” he added.

The main question for Shire and AbbVie now is how effective will these obstacles be in preventing AbbVie from buying and essentially becoming, for taxation purposes, a UK taxation resident domiciled in Jersey?

A good first point to make here is that AbbVie faces a penalty worth 3% of the $54.5bn deal if it walks away.

In theory that suggests it may have to cough-up $1.635bn, or almost 32% of the value of forecast net income this year, currently seen at $5.122bn.

AbbVie was already expected to pay out a dividend worth 17% less than the year before.

Assuming it opts to pay the potential penalty for not buying Shire, it would be faced with a difficult choice: either it will have to disappoint investors even more than they already expect, or it will have to allocate the financial pain elsewhere on its balance sheet.

It has a strong motive for going ahead with the deal.

As can be seen, opting for most of these choices would make AbbVie’s takeover of Shire ‘just another multi-billion dollar mega-merger’.

There would be obvious benefits to be had for all parties, even under reduced terms, but it’s questionable whether these potential benefits would be sufficient to satisfy AbbVie’s board and shareholders.

For Shire shareholders, whether a deal takes place or (more likely) not, to us, it looks like the party is over.

Any acquisition of Shire by AbbVie seems likely to take place under different terms or external conditions that would hamper its new owner for years.

There have been other takers for Shire over the years, but these have been few and of course, no deal was sealed.

Its forward price/earnings multiple of 18 times calls for recalibration.

The group’s specialisation, attention deficit disorder treatments, whilst clearly still an asset, is just that: a concentration of resources largely in one field.

For the shorter term, whilst the stock certainly looks oversold now, the strike to sentiment it has experienced today alone suggests a precarious ride.

The price may be no respecter of Fibonacci retracement levels, although today’s extension of a fall from the stock’s historical peak, reached earlier this month, leaves the shares in the ball park of a 38.2% level.

The April commencement point of this year’s ascent around 2820p seems distant and unlikely at least for the medium term.

Levels close to 3360p draw the eye. It’s where the shares hovered, or revisited for a couple of months in the summer, as per its 200-day moving average.