Shell shares set to keep sliding despite dividend pledge

Shell continued to miss analysts’ forecasts on Thursday, but the hit to its stock was relatively contained, despite an enormous $8.3bn write-off. The stock has […]

Shell continued to miss analysts’ forecasts on Thursday, but the hit to its stock was relatively contained, despite an enormous $8.3bn write-off. The stock has […]

Shell continued to miss analysts’ forecasts on Thursday, but the hit to its stock was relatively contained, despite an enormous $8.3bn write-off.

The stock has after all slumped 24% in the last 12 months.

The market’s lenience may also reflect that unlike some of its rivals, Shell left its 2015 $30bn capex forecast (previously lowered from $35bn) intact.

Core earnings still tanked by an eye-watering 70% to $1.8bn, though $1bn of the gap between actual and $2.74bn consensus was currency noise.

There was a ‘kitchen-sink’ undertone to the UK No.1 oil company’s third-quarter report, against which its $83bn takeover of BG is an important backdrop.

The deal, which is expected to be completed in April 2016, provides CEO Ben van Beurden with a useful internal pretext for sharper and quicker efficiencies than some on Shell’s board may be comfortable with.

It also of course drives the need for optimal financial conditions.

Part of that requires an official coming-to-terms with new oil-price realities.

Hence the headline charge included $3.7bn for reduced oil and gas price forecasts.

And whilst ‘upstream’ core production swung to a loss for the first time in years due to the oil price rout, ‘downstream’ refining and products benefited.

That enabled Shell to run refineries more profitably, lifting net income from that unit by 46% at $2.6bn.

The pattern by the world’s majors of redeploying efforts downstream to offset production revenue falls is now well established, discouraging questions about how sustainable the tactic is.

But when the dust settles, investors may still look again at Shell’s all-important dividend outlook.

Obviously, the ‘Elephant in the room’ for investors in oil majors is whether sickly oil prices could eventually weaken dividends.

For Shell, it’s a particularly pointed one, given that it remains—just—above the majority of blue-chip payers, including BP.

Calculation of RDS’s dividend outlook must take into account its deeper-than-average profit fall, and slower-than-average production guidance.

Capital is acceptable—given the climate.

Thomson Reuters data gives a relatively benign reading of Shell’s net debt compared to total capital.

At 13%, Shell is easily the least leveraged major among Total, BP, most-geared Eni (22%) and Statoil.

But whilst the same dividend slated for this year is pledged for the next, there’s no further guidance.

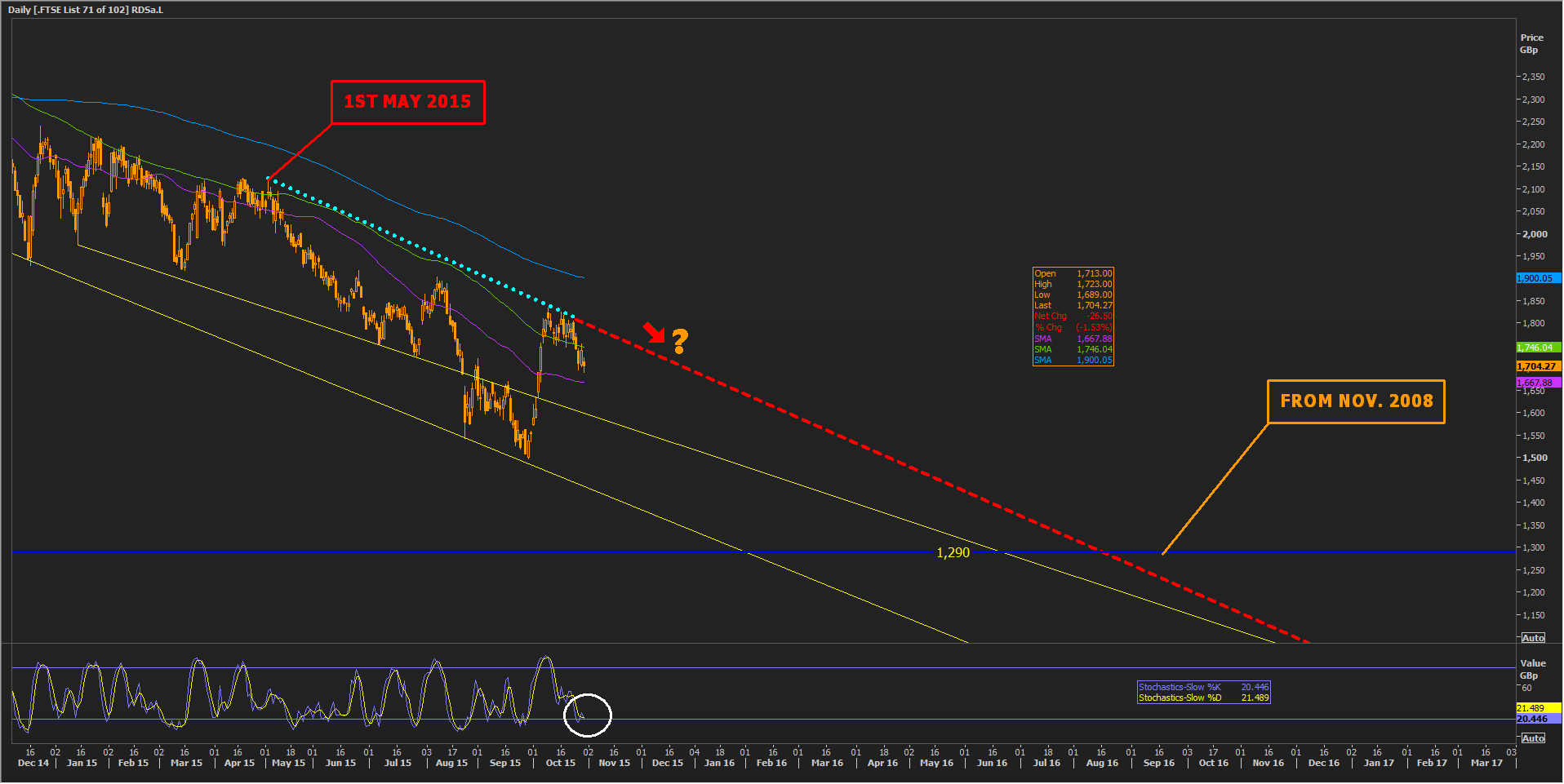

Few shares can rally under such circumstances and RDSA/B’s downtrend looks a surer bet than undiminished pay-outs.

For now, ebbing value at least looks set to remain orderly.

The current wave of near-term selling is almost complete (stochastic sub chart) and has left promising higher lows in absolute prices.

Even so, an imperfect channel established in May doesn’t look likely to break on the upside before ‘global credit crunch’ support around 1300p.

Please click image to enlarge