Shell shares rise from year lows on earnings and magic words

Royal Dutch Shell, Supermajor Oil Company Number 2, said the downturn in oil prices could last “several more years”, essentially sealing the fate of itself […]

Royal Dutch Shell, Supermajor Oil Company Number 2, said the downturn in oil prices could last “several more years”, essentially sealing the fate of itself […]

Royal Dutch Shell, Supermajor Oil Company Number 2, said the downturn in oil prices could last “several more years”, essentially sealing the fate of itself and its peers for the foreseeable future.

The biggest FTSE 100 company by market capitalisation said it was cutting 6,500 jobs and 20% of expenditure to begin squaring up with the fallow future it now sees as more baked in.

But it’s a fine balancing act to pull off whilst keeping shareholders on board.

Especially with RDSA stock sitting on loss of 30% since Q3 2014, pretty much in synch with the circa 60% fall of oil prices over the same time period, but with Shell underperforming peers due to its greater resistance to curbing ‘big ticket’ projects.

Not to mention Shell’s decision to undertake one of the most expensive takeovers of the year, with its acquisition of BG Group.

Shell’s CEO Ben van Beurden, is taking a similar tack as the Supermajor men who helm Exxon, BP, Chevron, Conoco and Total.

Their quarterly earnings and comments have been closely scrutinised in recent days or will be in the next few.

Van Beurden walked a fine line, between a somewhat more pessimistic assessment of oil prices than many investors might have expected, and about a bullish a stance as is currently credible about ‘big ticket’ projects, plus the hot topic of returning cash to shareholders.

“We have to be resilient in a world where oil prices remain low for some time, whilst keeping an eye on recovery,” he said.

Shell’s increased prudence still needs to be taken with a small pinch of salt.

It’s still gunning full steam ahead on big projects.

Whilst ‘Supermajor’ peers have cut 10%-15% of spending since 2014 to date, Shell is reaching the lower end of that range with a seven-month lag.

Its peers have also largely delayed approval of big ticket projects.

But despite Shell announcing on Thursday fresh “cost reductions, project cancellations and re-phasing of growth options”, it is still pressing on with its deep-water Appomattox oil field in the Gulf of Mexico.

It also announced this month that it would finally begin drilling in the Alaskan Arctic.

It’s been a decade since Shell began buying new leases in the Arctic, and it has spent about $7bn on the project there, which as yet remains officially one of exploration, not production.

A somewhat more quickly accretive ‘big ticket’ deal is Shell’s planned buy of BG Group, which will probably catapult Shell among the biggest liquefied natural gas producers in the world.

Despite a trail of briefings and comments leading up to Thursday’s quarterly results, Shell has not, as many had expected, provided a firm upgrade of expected synergies.

It has left the impression that they will be a multiple of $1bn per annum, but suggested it cannot yet quantify these savings further in a way that would be acceptable under takeover rules.

The market sees current pre-tax benefits around $2.5bn a year, from 2018.

Shell did note that spending by the combined company, if the deal is sealed as planned early in 2016, will be around $35bn in that year, about $7bn below market views.

Shell’s ‘LNG for Transport’ booth at LNG17 conference, Houston, Texas, April 17th 2013

Please click image to enlarge

Still on closer examination, forecast-beating key earnings aside, the Royal Dutch Shell that’s going into the second half of the year does not seem that much different to the one from H1.

The main reason its stock sat at the top of the FTSE 100 for most of Thursday is that van Beurden was sure to include magic words among his utterances this morning.

“We’re taking a prudent approach, pulling on powerful financial levers to manage through this downturn, always making sure we have the capacity to pay attractive dividends for shareholders.”

Shell is still a few ticks above the world’s biggest oil producers on dividend pay-outs: 0.9% above the average with a 2.5% premium forecast during the next twelve months.

Obviously its margin for error for maintaining that lead could have better odds than those outlined above.

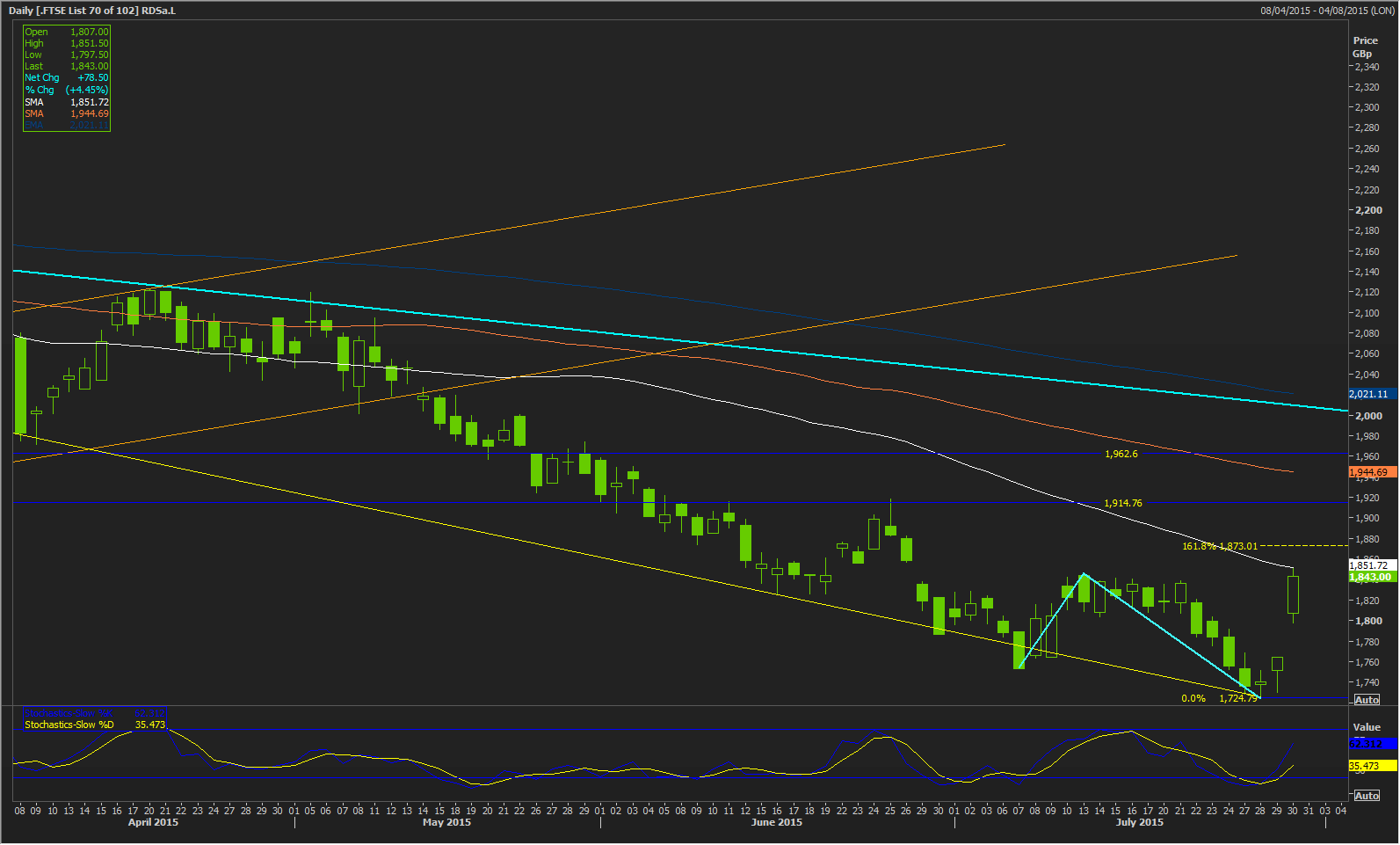

These odds pushed its stock to their lowest levels of the year earlier this week.

The stock is now touching its 50-day moving average, something it has not done for since May.

Some room remains above before potential completion of a continuation pattern from earlier in July that will end at an important 161.8% interval.

At some point, the gap below Thursday’s strong open and Wednesday’s highs will probably be filled, though strong current momentum argues against that happening in the immediate term.

Either way, long-standing resistance between 1914.76p and 1962.6p lies ahead, whilst the recently established 2015 low is likely to remain magnetic for the medium term.

Please click image to enlarge