September 24, 2019 5:38 PM

"She Said, He Said" Moving Markets

Quick Summary

The Washington Post reported earlier today that House Speaker Nancy Pelosi is expected to announce a formal impeachment inquiry into President Donald Trump this evening. This comes after a whistleblower over the weekend has said that Trump asked Ukraine’s President in a July phone call to investigate Joe Biden’s son. Joe Biden said he supports the impeachment proceedings unless Trump releases the transcripts from the call. Trump responding by tweeting that he will release the transcripts tomorrow. Pelosi says she will proceed with impeachment inquiry. Oh, and by the way, the whistleblower has asked to come before congress.

Why Does this Matter

Markets are moving into uncertainty regarding the “possibility” of a Trump impeachment. Markets don’t like uncertainty and tend to move to risk off mode (selling stocks, buying treasuries) on such occasions. But more importantly, if the process does play out and Trump is impeached, markets may assume there will be no trade deal with China, as well as no USMCA agreement.

Upon the initial announcement of the formal impeachment inquiry both stocks and the US Dollar Index added to their losses on the day. Gold continued higher. As headlines were released throughout the day, volatility ensued. But at the end of the day, most markets took their lumps as we wait for Pelosi press conference at 5:00pm. Let’s look at a few markets and see if we can determine some technical levels, and where we may be headed next:

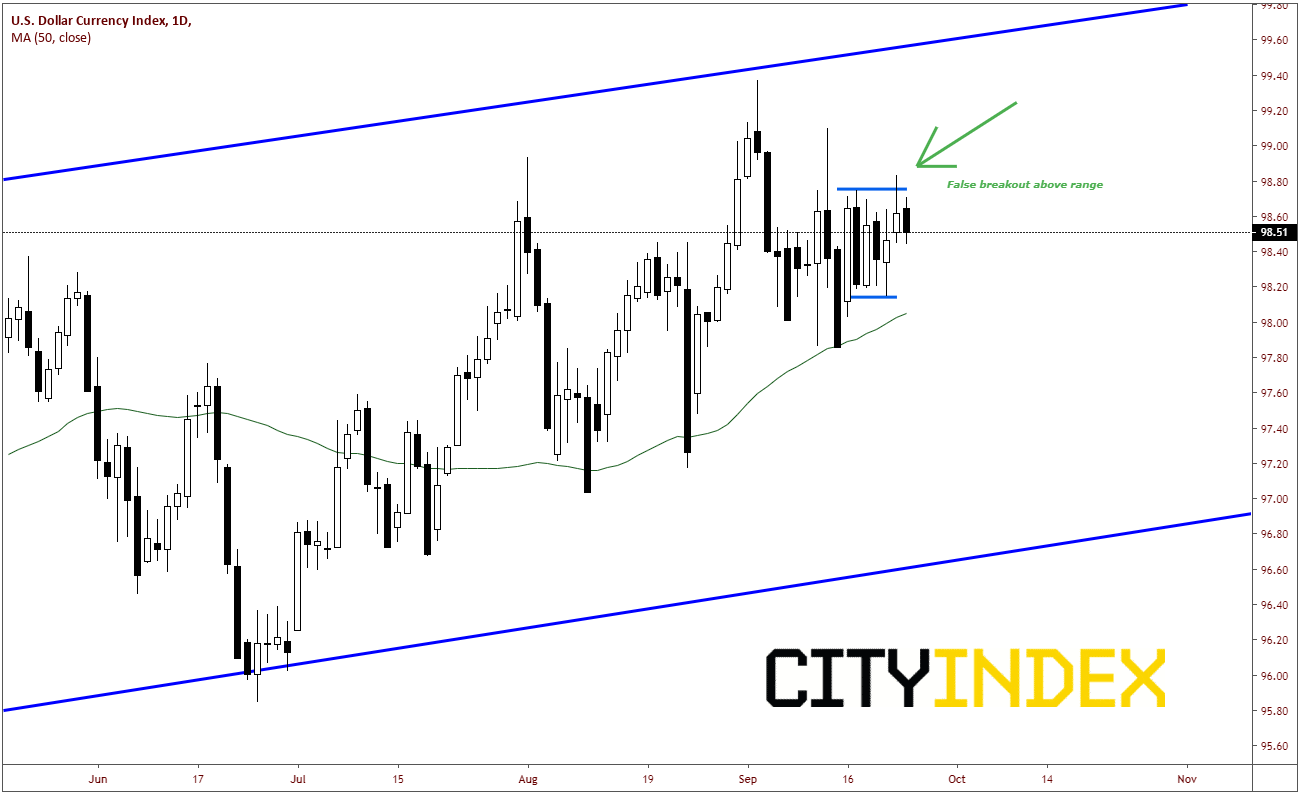

DXY

Not too much to add here today, as we had discussed DXY this morning. Support is at 98.14, the bottom of the trading range we have been in. Just below that is the 50 Day Moving Average near 98.00. First intraday resistance at 98.50, intraday horizontal resistance. Next resistance is yesterday’s highs at 98.83.

Source: Tradingview, City Index

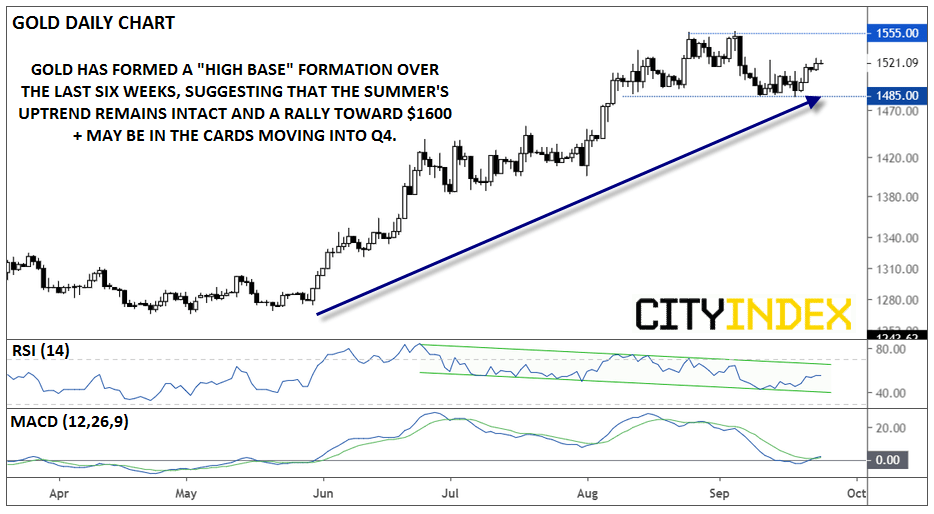

GOLD

As my college Matt Weller had written about earlier, has not yet put in a meaningful “lower low”, and the longer upward sloping trend is still intact. The clear resistance level to watch is 1555, which is the recent highs. The support level to watch is 1485, which has been touched multiple times over the last few weeks but has held.

Source: Tradingview, City Index

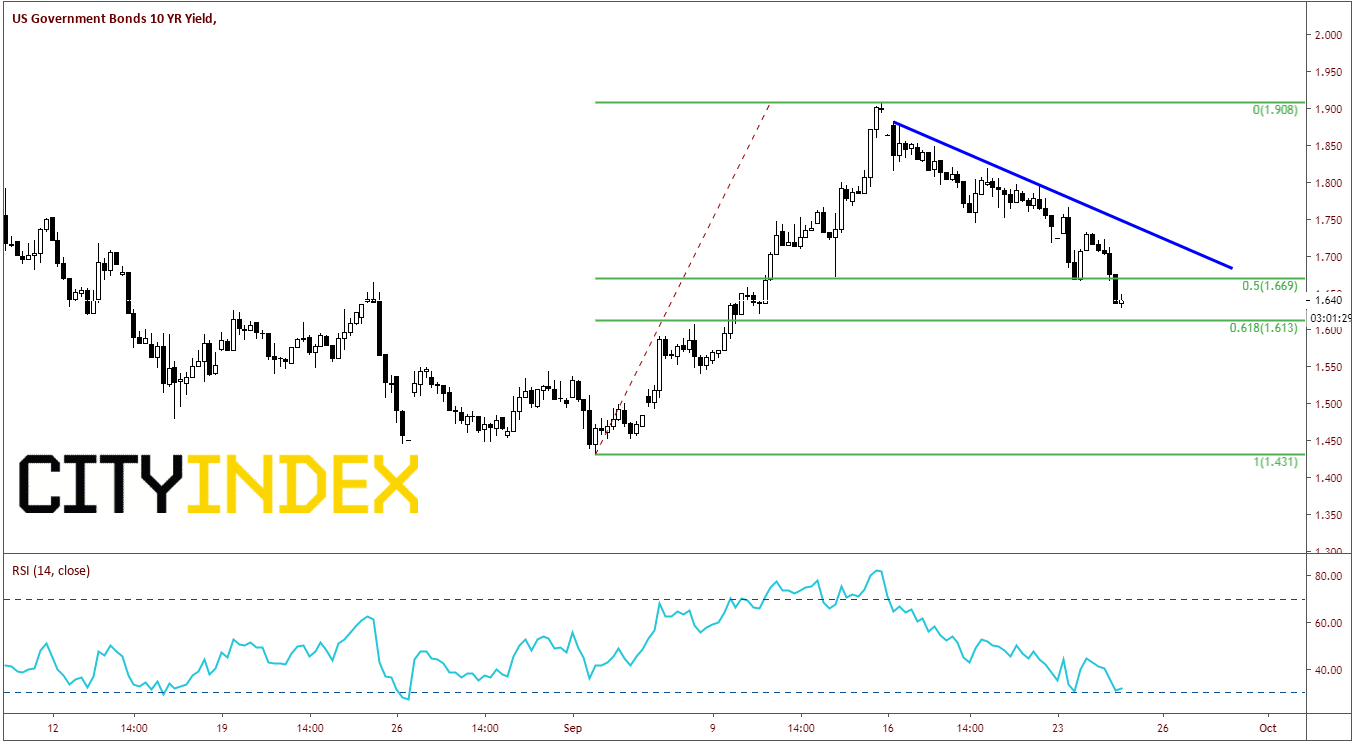

YIELDS

10-Year Yields really took it on the chin today down over 5% on the day. The high today was 1.73%, however bonds closed down near the lows at 1.64% 10 Year Yields have not retraced over 50% of the move higher from the lows on September 3rd to the highs on September 13th. Resistance comes in at the descending trendline near 1.75%, which support is close at 1.61%, which is the 61.8% retracement of the previously mentioned move.

Source: Tradingview, City Index

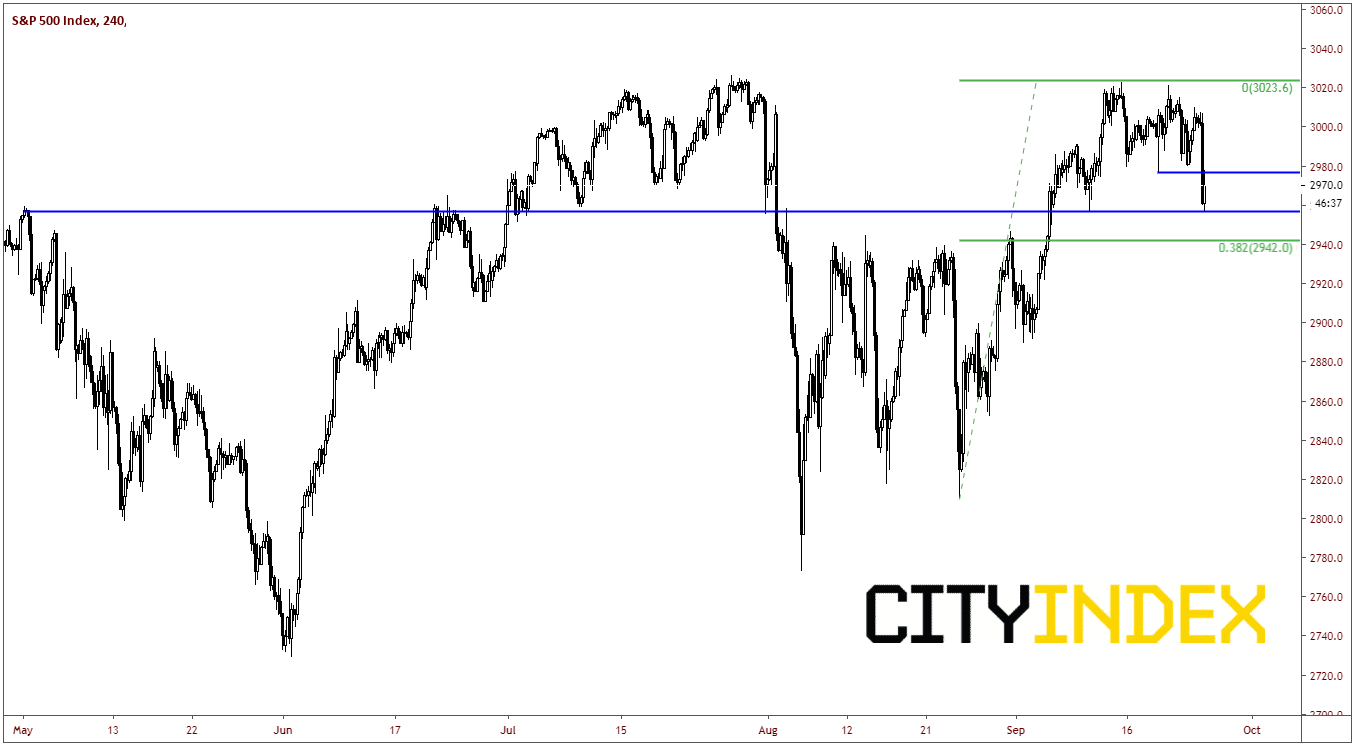

SPX500

Stocks closed lower on the day, down almost 1% near 2970, however held the all-important horizontal support level at 2957, which has acted as a pivotal support and resistance area for the second half of this year. Next support comes in at 2942, which is the 38.2% retracement level from the August 23rd lows to the highs on September 13th as well as previous resistance (which now acts as support). Intraday resistance comes in at 2975 and the day’s highs at 3009.8.

Source: Tradingview, City Index

What’s Next?

As we mentioned this morning, watch for more headlines and tweets. Not only could they move the markets, but the comments could be made shortly, in an illiquid and quiet market, which could add to any volatility.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Latest Bonds articles

April 23, 2024 11:09 PM

April 22, 2024 03:42 AM

April 18, 2024 06:20 AM

April 10, 2024 01:09 AM