December 26, 2019 9:32 AM

Our last update on the S&P500 was in early December, shortly after an apparent escalation in President Trump's trade war over a 24-hour period, which included tariff threats against Argentina, Brazil, China and France as well as NATO members whom he considered weren’t spending enough on defense.

Fearing the damage that a trade war escalation would do to the global economy, equity markets were quick to respond. Headlines predicted that Trump's tariff tirade had curtailed the usual end-of-year Santa stock market rally before it had even started. We argued to the contrary and that after a brief pullback, the Santa rally would take place as usual in 2019 here.

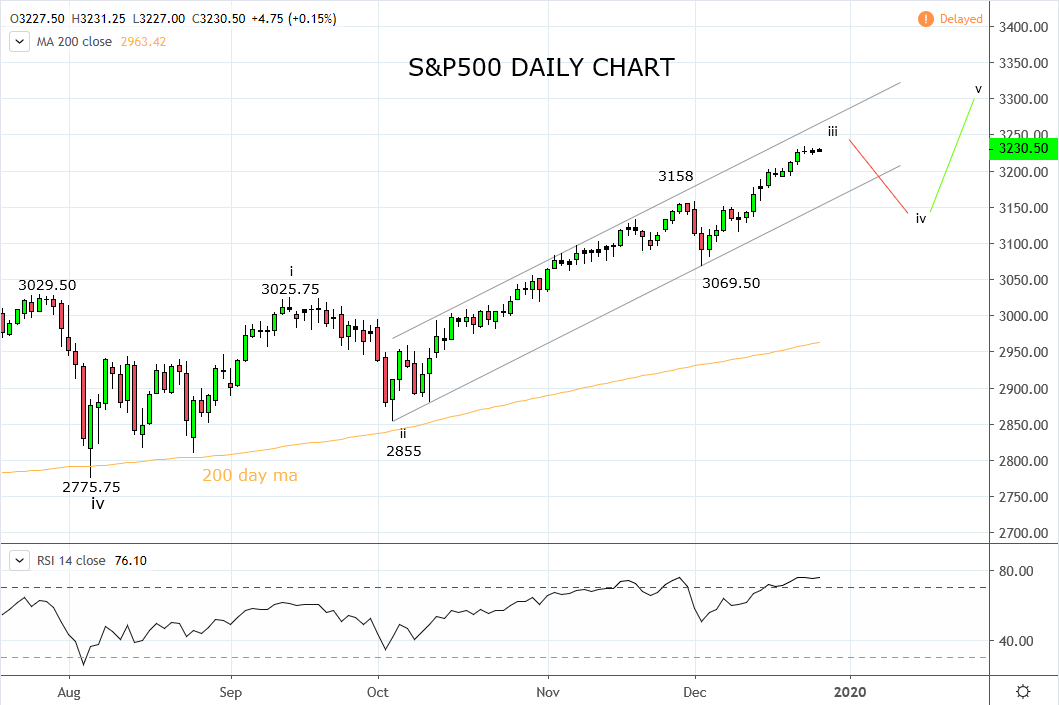

After reaching and breaching our 3200 target last week, the S&P500 is exhibiting short term signs of being overbought. However, with the festive season in full swing, light trading volumes, fund managers unlikely to sell their favourite stocks before year-end and investors optimistic after the U.S. and China agreed to a trade deal, the S&P500 looks set to end 2019 near to all-time highs.

In light of this, the most likely window for a pullback is in early January. Although with economic data continuing to show signs of improvement, subdued inflation and supportive monetary policy, dips in the S&P500 are likely to be shallow, within the 3-5% range.

Technically, following the break to new highs in late October, the S&P500 has been trading within a bullish trend channel. Should a pullback occur in January, the first level of support would come from the lower bound of the trend channel, currently 3150/3130 area. Below there, medium-term support starts at 3070 and extends down to the previous highs 3030/3025 area.

With this in mind, dips towards the support regions mentioned above would be viewed as buying opportunities, in expectation of the uptrend resuming in February 2020. Only a break and close below 3020/10 would be cause to reassess the bullish view.

Source Tradingview. The figures stated areas of the 26th of December 2019. Past performance is not a reliable indicator of future performance. This report does not contain and is not to be taken as containing any financial product advice or financial product recommendation

Latest market news

Today 08:33 AM

Latest Wall Street articles

August 8, 2023 09:54 AM

July 26, 2022 03:39 AM

June 30, 2022 08:10 AM

June 22, 2022 02:56 AM