Services ISM bounce amp USD recovery

Is the USA back? Four days after the release of the sixth consecutive monthly NFP reading of +200k (not seen since 1997), the July services […]

Is the USA back? Four days after the release of the sixth consecutive monthly NFP reading of +200k (not seen since 1997), the July services […]

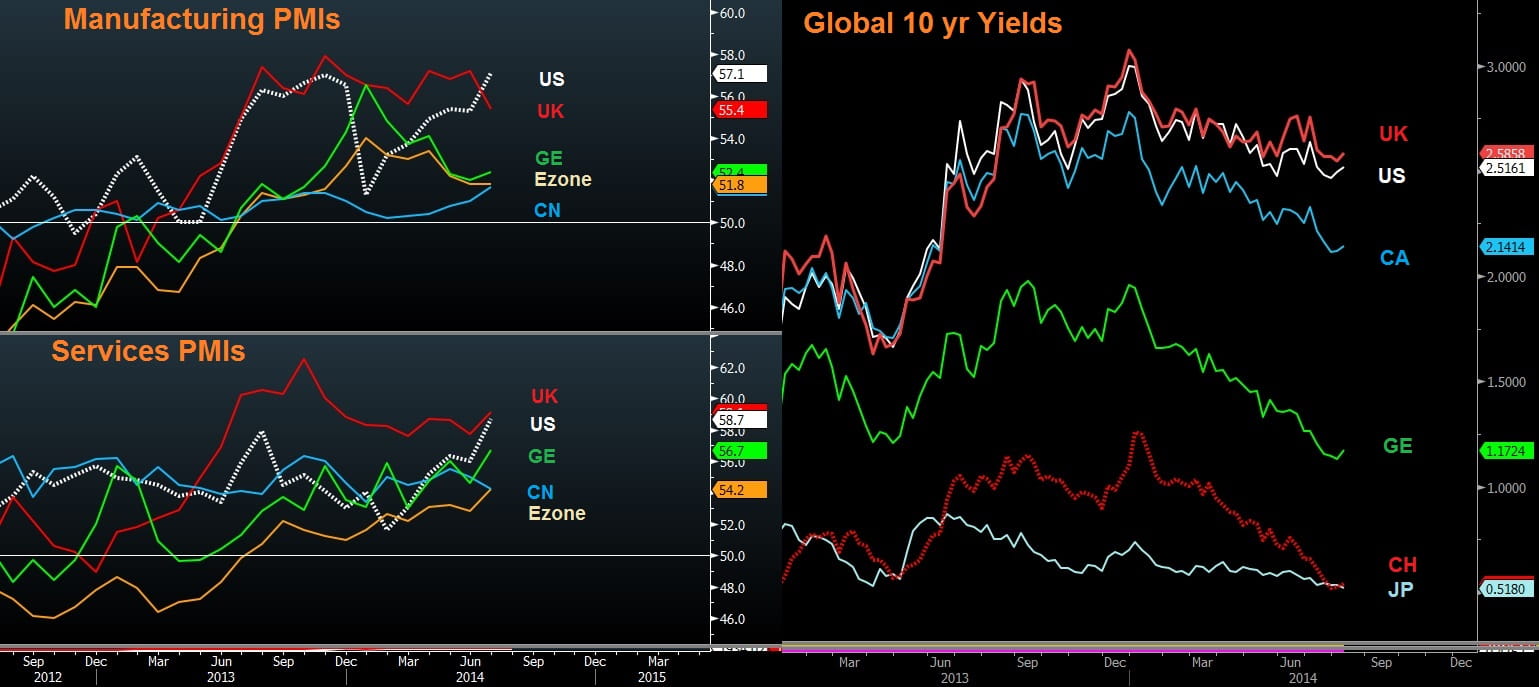

Is the USA back? Four days after the release of the sixth consecutive monthly NFP reading of +200k (not seen since 1997), the July services ISM posted its biggest monthly rise in five years, reaching a nine-year high of 58.7. The employment component hit a six-month high at 56.0 and the new orders component surged to 64.9, also a nine-year high. Meanwhile, the US dollar index is at 12-month highs.

Last Friday’s release of the July ISM hitting the highest level since April failed to support the USD and yields due to the a few disappointing details from the July jobs report.

Looking at the chart below, the US manufacturing ISM crossed above its UK counterpart for the first time since March 2013 (excluding a one-time appearance) in October.

The services chart remains dominated by the UK, but the margin may change later this year.

Having said that, UK services PMI has undergone a period of consolidation during the last seven months, while its US counterpart is playing catch-up. As the US economic machine attempts its great post-Q1 rebound, the US dollar will likely build further gains due to US economic merit rather than the ills of others.

The US dollar index seeks to post its fourth consecutive weekly gain, the biggest streak in over 17 months. The rally will deserve more attention upon a breach of the 83 level from the current 81.50.

A USD rally based on shifting monetary policy expectations may need to be manifested through stabilising US bond yields, which has not been the case, beyond a 2-3 day rally. In fact, the last time we saw some form of simultaneous rally in US yields and USD was in June 2013, when the taper tantrum (fears of tapering from the Fed) triggered a rush back into the USD currency away from EM currencies.

Twelve months later, we moved on to a new unofficial guidance. Just as in the UK, improving US data will require notable improvement in wage/earnings figures in order for the Fed to give inflation any serious thought.