Serco share downside still extensive

Serco Group Plc. has seen around £600m wiped off its market value after it shocked the markets with a multi-million pound write-off and by announcing […]

Serco Group Plc. has seen around £600m wiped off its market value after it shocked the markets with a multi-million pound write-off and by announcing […]

Serco Group Plc. has seen around £600m wiped off its market value after it shocked the markets with a multi-million pound write-off and by announcing it would issue new shares, sending its existing stock careering 35% lower.

The outsourcing services firm said it would release £500m-worth of new stock and it needed to restate the value of assets on its balance sheet by a massive £1.5bn.

To an extent, the day’s news represents the culmination of the collapse of Serco’s reputation and core business after the government took the unprecedented step of ‘naming and shaming’ the group for overcharging on contracts with the UK’s prison service.

Serco was banned from bidding for new government contracts for 6 months, along with G4S Plc.

G4S shares have also been hit today, but by just a fraction of the extent to which Serco was slammed.

In an unscheduled announcement this morning Serco said it would

Serco, which still employs around 100,000 people in more than 30 countries, cut its forecast for 2014 adjusted operating profit by around £20m to a target of between £130m and £140m.

It also cut its forecast outlook for 2015.

The downgrades, which do not include the impairment charge, are partly aimed at providing Serco with time during which it can take measures to tackle a string of failed contracts, said its chief executive Rupert Soames, who joined the firm in May.

“We are able to provide an initial estimate of the impairments, write-downs and onerous contract provisions that are likely to be required at year end,” Soames said in the release.

“We now have a number of contracts which are making large losses, and others which are in sectors where we are subscale,” Soames added.

It’s worth noting Serco’s strategic review, including contracts and finances remains on-going and would not be completed before March, meaning more bad news may still await.

The company warned in its statement: “The range of possible outcomes is still wide.”

Overall, in terms of kitchen sinks, today’s from Serco, is just about as big and as bad as they come.

And the worst may not in fact be over either operationally or on the bottom line.

We note market forecasts of 2014’s net income margin still call for a respectable recovery of some 230 basis points from a 0.5% net margin reported at the end of 2013.

Chances of a 2.8% margin being reported in December, as per current forecasts, now appear low.

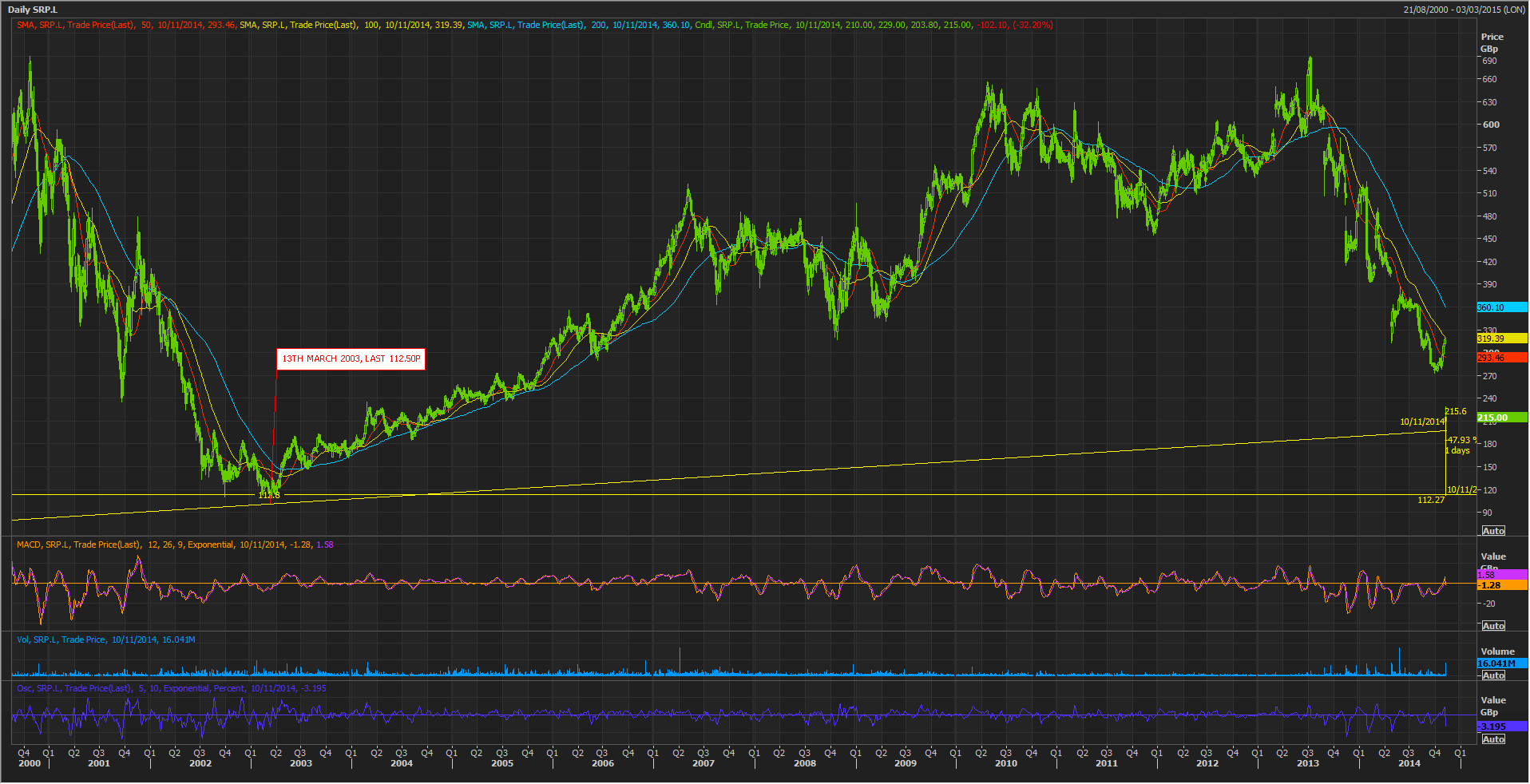

If Serco is indeed being dialled back to ‘first principles’, the major closing low of 112.50p in March 2003 gains some magnetism, though that price might represent too extreme a scenario, even following today’s mega de-rating.

Working in reverse from earnings expectations may help a bit.

Taking the mean of a 24-month forward price/earnings ratio the market currently applies suggests an 11 times ratio.

Applying that over the next twelve months suggests an EPS of 16.88p.

And that in turn is suggestive of a price that is still 15.4% lower than this evening’s settlement price of 221.68p, implying a further fall to at least 187p.

But these are quite generous assumptions.