The FTSE is on the rebound, trading over 1% higher for the third straight session. The Index is on track to gain 3.6% across the week, its second straight week of gains over 3%. The FTSE has risen for 4 of the past five weeks. The numbers tell us that a recovery is in progress, at least for now.

The FTSE is a relative underperformer compared to its peers however the recent easing of restrictions, vaccine optimism and break through of significant resistance this morning means that UK stocks could be in for an additional surge higher, in the short term.

The stocks which soared under lock down, such as Netflix, Amazon in the US and Utilities here is the UK are seeing their growth slow. Meanwhile the stocks that took the biggest hit on the way down have been dominating the upper reaches of the index over this week.

Given the unprecedented nature of the crisis that we are in, it is impossible to predict how deep the recession will be and for how long it will go one for. However, what we have seen over the past few sessions is that optimism is overshadowing longer term economic fears and also where the up -tick in stocks is happening, giving clues as to which sectors are set to benefit the most for easing lockdown measures.

Travel stock

It is still a long way back for travel stocks, however revived hopes of a summer holiday season has lifted the likes of BA owner International Consolidated Airlines Group, EasyJet, Carnival Group and TUI Travel to name a few. Optimism is growing that summer holiday’s might not be a complete write off after all. Traders will also be watching the government’s response as pressure builds on Boris to scrap the 14-day quarantine rule for all those entering the UK. Any sign of this being removed could give this sector an important boost

Despite recent gains it is still too early to call a recovery for travel stocks with IAG still 60% below its February price and EasyJet 58%.

It is still a long way back for travel stocks, however revived hopes of a summer holiday season has lifted the likes of BA owner International Consolidated Airlines Group, EasyJet, Carnival Group and TUI Travel to name a few. Optimism is growing that summer holiday’s might not be a complete write off after all. Traders will also be watching the government’s response as pressure builds on Boris to scrap the 14-day quarantine rule for all those entering the UK. Any sign of this being removed could give this sector an important boost

Despite recent gains it is still too early to call a recovery for travel stocks with IAG still 60% below its February price and EasyJet 58%.

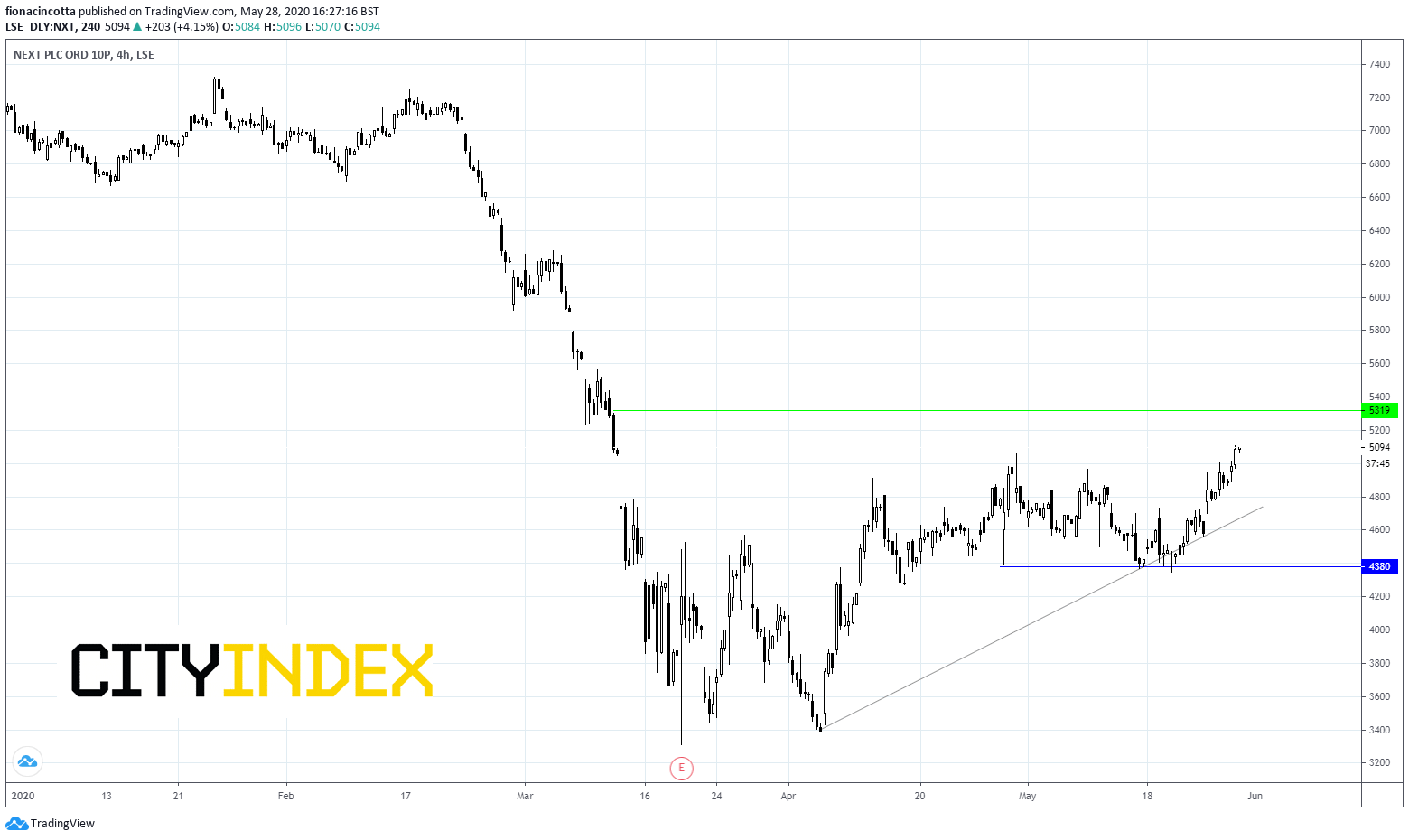

Retailers

The announcement that shops will be reopening their doors at from 15th of June, was reflected by a jump in retailers. Primark owner Associated British Foods was a notable winner, given its lack of an online presence. Bellwether has also charged higher over the coming days. Next is in a particularly good spot given its sophisticated online offering. The retailer will be able to take advantages in any longer-term changes to shopping habits which lock down produced – namely more online shopping. The government is considering reducing the social distancing limit down from 2 meters. Should this go-ahead retailers could get an additional boost.

The announcement that shops will be reopening their doors at from 15th of June, was reflected by a jump in retailers. Primark owner Associated British Foods was a notable winner, given its lack of an online presence. Bellwether has also charged higher over the coming days. Next is in a particularly good spot given its sophisticated online offering. The retailer will be able to take advantages in any longer-term changes to shopping habits which lock down produced – namely more online shopping. The government is considering reducing the social distancing limit down from 2 meters. Should this go-ahead retailers could get an additional boost.

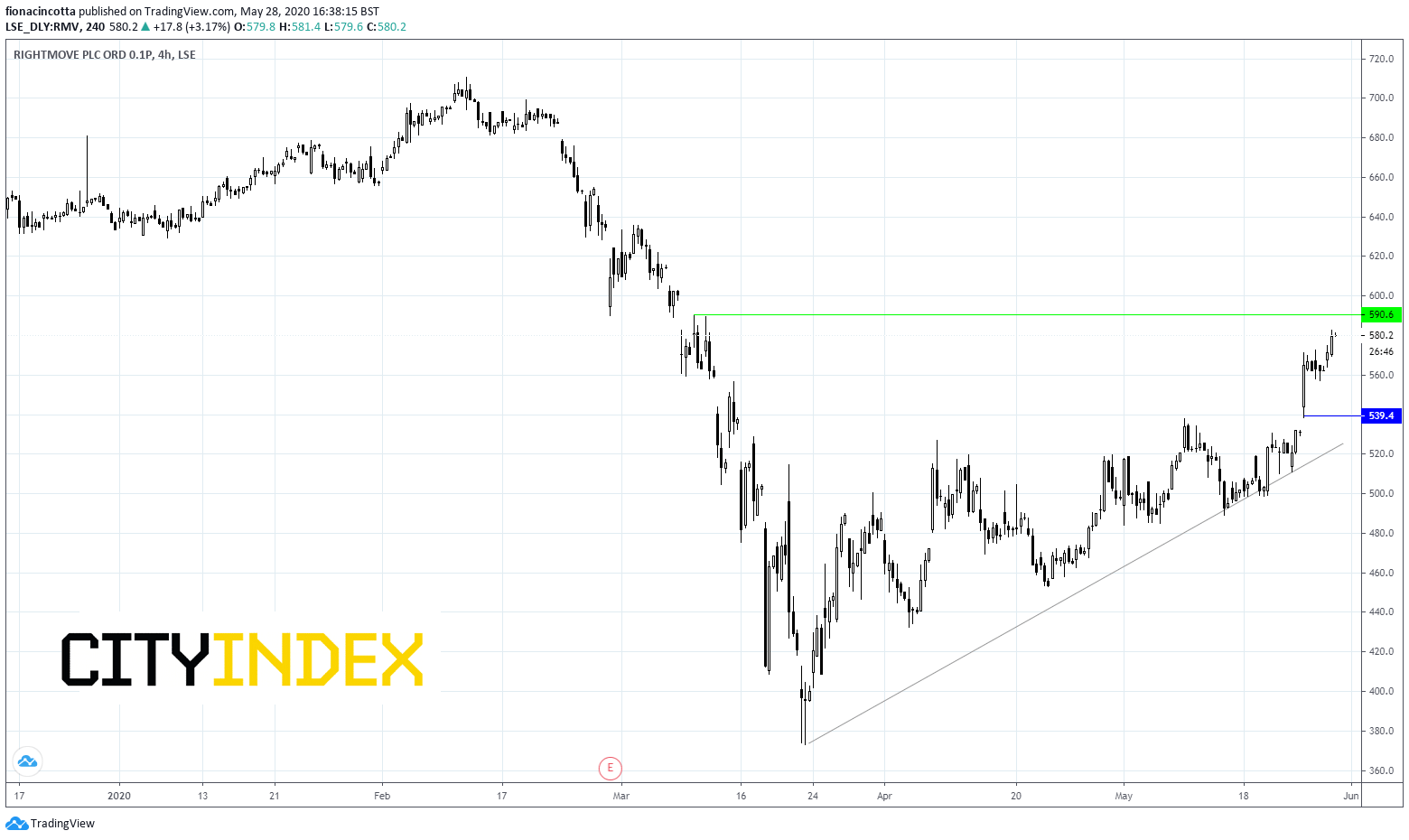

Property

Property stocks, such as Foxtons, Rightmove and Countrywide have risen this week and could continue to rise. Rightmove has surged 8.6% so far as investors grow increasingly optimistic of a housing market revival. However, it is worth keeping an eye on Brexit news over the coming months. A cliff edge Brexit could add pressure to the housing market, property prices and property shares.

Property stocks, such as Foxtons, Rightmove and Countrywide have risen this week and could continue to rise. Rightmove has surged 8.6% so far as investors grow increasingly optimistic of a housing market revival. However, it is worth keeping an eye on Brexit news over the coming months. A cliff edge Brexit could add pressure to the housing market, property prices and property shares.

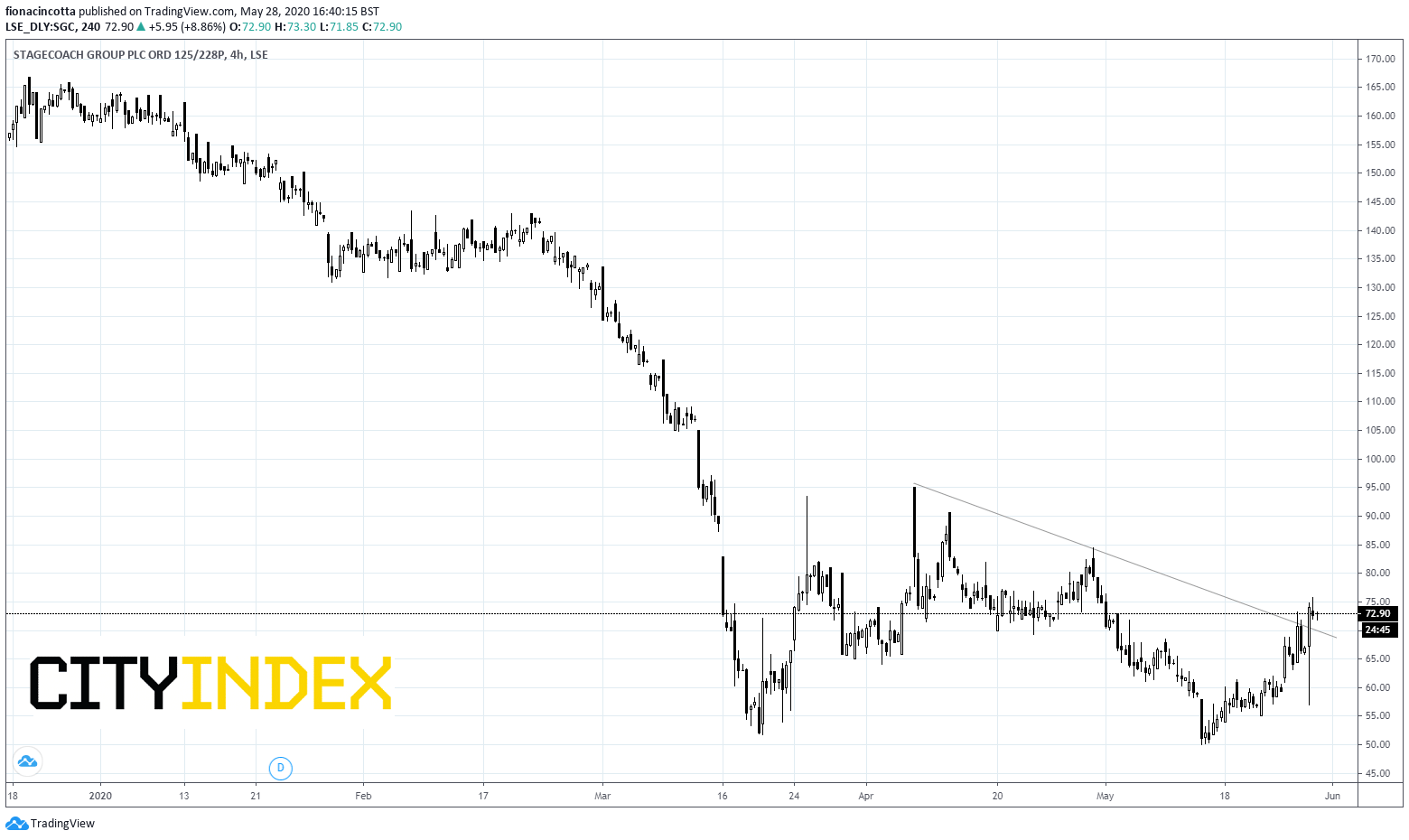

Transport

Transport will be a sector to watch after the UK government pledged £254 million for buses and £29 million for trams and light railway to improve the frequency of services. Stocks such as Stagecoach, National Express and First Group have all performed well across the past few sessions with scope for further upside as people start returning to work.

Latest market news

Yesterday 11:09 PM

Yesterday 11:01 PM

Yesterday 04:00 PM

Yesterday 01:15 PM

Yesterday 11:30 AM

Latest Indices articles

April 18, 2024 04:46 PM

April 17, 2024 11:00 AM

April 16, 2024 08:00 PM

April 16, 2024 04:54 PM